Panera Bread 2011 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2011 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

47

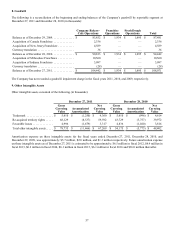

Other Intangible Assets, net

Other intangible assets, net consist primarily of favorable lease agreements, re-acquired territory rights, and trademarks. The

Company amortizes the fair value of favorable lease agreements over the remaining related lease terms at the time of the acquisition,

which ranged from approximately 2 years to 17 years. The fair value of re-acquired territory rights was based on the present value

of the acquired bakery-cafe cash flows. The Company amortizes the fair value of re-acquired territory rights over the remaining

contractual terms of the re-acquired territory rights at the time of the acquisition, which ranged from approximately 13 years to

20 years. The fair value of trademarks is amortized over their estimated useful life of 22 years.

The Company reviews intangible assets with finite lives for impairment when events or circumstances indicate these assets might

be impaired. When warranted, the Company tests intangible assets with finite lives for impairment using historical cash flows and

other relevant facts and circumstances as the primary basis for an estimate of future cash flows. As of December 27, 2011,

December 28, 2010, and December 29, 2009, no impairment of intangible assets with finite lives had been recognized. There can

be no assurance that future intangible asset impairment tests will not result in a charge to earnings.

Impairment of Long-Lived Assets

The Company evaluates whether events and circumstances have occurred that indicate the remaining estimated useful life of long-

lived assets may warrant revision or that the remaining balance of an asset may not be recoverable. When appropriate, the Company

determines if there is impairment by comparing anticipated undiscounted cash flows from the related long-lived assets of a bakery-

cafe or fresh dough facility with their respective carrying values. If impairment exists, the amount of impairment is determined

by comparing anticipated discounted cash flows from the related long-lived assets of a bakery-cafe or a fresh dough facility, which

approximates fair value, with their respective carrying values. In performing this analysis, management considers such factors as

current results, trends, future prospects, and other economic factors. No impairment loss was recognized during the fiscal year

ended December 27, 2011. The Company recognized an impairment loss of $0.1 million and $0.6 million during the fiscal years

ended December 28, 2010 and December 29, 2009, respectively, related to a distinct underperforming Company-owned bakery-

cafe within each fiscal year. The loss was recorded in other operating expenses in the Consolidated Statements of Operations.

Self-Insurance Reserves

The Company is self-insured for a significant portion of its workers’ compensation, group health, and general, auto, and property

liability insurance with varying deductibles of as much as $0.5 million for individual claims, depending on the type of claim. The

Company also purchases aggregate stop-loss and/or layers of loss insurance in many categories of loss. The Company utilizes

third party actuarial experts’ estimates of expected losses based on statistical analyses of historical industry data, as well as its

own estimates based on the Company’s actual historical data to determine required self-insurance reserves. The assumptions are

closely reviewed, monitored, and adjusted when warranted by changing circumstances. The estimated accruals for these liabilities

could be affected if actual experience related to the number of claims and cost per claim differs from these assumptions and

historical trends. Based on information known at December 27, 2011, the Company believes it has provided adequate reserves for

its self-insurance exposure. As of December 27, 2011 and December 28, 2010, self-insurance reserves were $23.6 million and

$20.2 million, respectively, and were included in accrued expenses in the Consolidated Balance Sheets. The total amounts expensed

for self-insurance were $35.9 million, $35.6 million, and $37.1 million, for the fiscal years ended December 27, 2011, December 28,

2010, and December 29, 2009, respectively.

Income Taxes

The Company completes the provision for income taxes in accordance with the accounting standard for income taxes in the

Company’s consolidated financial statements and accompanying notes. Under this method, deferred tax assets and liabilities are

recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing

assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income tax rates

expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled.

Any effect on deferred tax assets and liabilities from a change in tax rates is recognized in income in the period that includes the

enactment date.

In accordance with the authoritative guidance on income taxes, the Company establishes additional provisions for income taxes

when, despite the belief that tax positions are fully supportable, there remain certain positions that do not meet the minimum

probability threshold, which is a tax position that is more likely than not to be sustained upon ultimate settlement with tax authorities

assuming full knowledge of the position and all relevant facts. In the normal course of business, the Company and its subsidiaries

are examined by various Federal, State, foreign, and other tax authorities. The Company regularly assesses the potential outcomes

of these examinations and any future examinations for the current or prior years in determining the adequacy of its provision for

income taxes. The Company continually assesses the likelihood and amount of potential adjustments and adjusts the income tax