Kraft 2003 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2003 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66

|

|

58

Kraft Foods Inc. Notes to Consolidated Financial Statements

The Company is exposed to price risk related to forecasted

purchases of certain commodities used as raw materials by the

Company’s businesses. Accordingly, the Company uses commodity

forward contracts as cash flow hedges, primarily for coffee, cocoa,

milk and cheese. Commodity futures and options are also used to

hedge the price of certain commodities, including milk, coffee,

cocoa, wheat, corn, sugar and soybean oil. In general, commodity

forward contracts qualify for the normal purchase exception under

SFAS No. 133 and are, therefore, not subject to the provisions of

SFAS No. 133. At December 31, 2003 and 2002, the Company

had net long commodity positions of $255 million and $544 million,

respectively. Unrealized gains or losses on net commodity positions

were immaterial at December 31, 2003 and 2002. The effective

portion of unrealized gains and losses on commodity futures and

option contracts is deferred as a component of accumulated other

comprehensive earnings (losses) and is recognized as a component

of cost of sales in the Company’s consolidated statement of

earnings when the related inventory is sold.

Derivative gains or losses reported in accumulated other

comprehensive earnings (losses) are a result of qualifying hedging

activity. Transfers of these gains or losses from accumulated other

comprehensive earnings (losses) to earnings are offset by

corresponding gains or losses on the underlying hedged items.

During the year ended December 31, 2003, ineffectiveness related to

cash flow hedges was a gain of $13 million, which was recorded in

cost of sales on the consolidated statement of earnings.

Ineffectiveness related to cash flow hedges during the year ended

December 31, 2002 was not material. At December 31, 2003,

the Company was hedging forecasted transactions for periods not

exceeding twelve months and expects substantially all amounts

reported in accumulated other comprehensive earnings (losses)

to be reclassified to the consolidated statement of earnings within

the next twelve months.

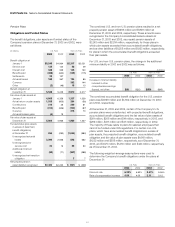

Hedging activity affected accumulated other comprehensive

earnings (losses), net of income taxes, during the years ended

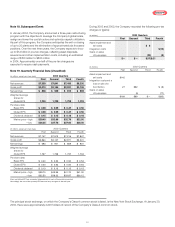

December 31, 2003, 2002 and 2001, as follows:

(in millions)

2003 2002 2001

Gain (loss) as of January 1 $13 $(18) $

—

Derivative (gains) losses transferred

to earnings (17) 21 15

Change in fair value 510 (33)

Gain (loss) at December 31 $1 $13 $(18)

Credit exposure and credit risk: The Company is exposed

to credit loss in the event of nonperformance by counterparties.

However, the Company does not anticipate nonperformance,

and such exposure was not material at December 31, 2003.

Fair value: The aggregate fair value, based on market quotes, of

the Company’s third-party debt at December 31, 2003, was $13,426

million as compared with its carrying value of $12,919 million. The

aggregate fair value of the Company’s third-party debt at December

31, 2002, was $11,764 million as compared with its carrying value of

$10,988 million. Based on interest rates available to the Company for

issuances of debt with similar terms and remaining maturities, the

aggregate fair value and carrying value of the Company’s long-term

notes payable to Altria Group, Inc. and its affiliates were $2,764

million and $2,560 million, respectively, at December 31, 2002.

See Notes 3, 7 and 8 for additional disclosures of fair value for short-

term borrowings and long-term debt.

Note 17. Contingencies:

The Company and its subsidiaries are parties to a variety of legal

proceedings arising out of the normal course of business, including

a few cases in which substantial amounts of damages are sought.

While the results of litigation cannot be predicted with certainty,

management believes that the final outcome of these proceedings

will not have a material adverse effect on the Company’s

consolidated financial position or results of operations.

Guarantees: At December 31, 2003, the Company’s third-party

guarantees, which are primarily derived from acquisition and

divestiture activities, approximated $38 million. Substantially all of

these guarantees expire through 2014, with $13 million expiring

during 2004. The Company is required to perform under these

guarantees in the event that a third party fails to make contractual

payments or achieve performance measures. The Company has a

liability of $26 million on its consolidated balance sheet at December

31, 2003, relating to these guarantees.