Kraft 2003 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2003 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

|

|

Kraft Foods Inc. Management’s Discussion and Analysis of Financial Condition and Results of Operations

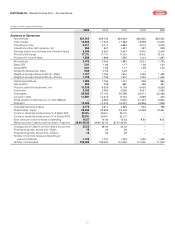

Net revenues increased $422 million (2.0%), due primarily to higher

volume/mix ($170 million), higher pricing, net of increased promo-

tional spending ($151 million), and favorable currency ($120 million),

partially offset by the divestiture of a small confectionery business in

2002 ($21 million).

Operating companies income decreased $33 million (0.7%), due

primarily to unfavorable costs, net of higher pricing ($161 million,

including higher commodity costs and increased promotional

spending), higher fixed manufacturing costs ($79 million, including

higher benefit costs) and unfavorable volume/mix ($37 million),

partially offset by 2002 pre-tax charges for asset impairment and exit

costs ($135 million) and the impact of lower integration costs and a

loss on sale of a food factory ($107 million).

The following discusses operating results within each of KFNA’s

reportable segments.

Cheese, Meals and Enhancers: Volume increased 1.7%, due

primarily to higher shipments in cheese, food service, Canada

and Mexico. Cheese volume increased due primarily to improved

consumption and share trends resulting from the investment

program that began in the third quarter of 2003. Volume for the

food service business in the United States also increased, due to

higher shipments to national accounts. Volume in Canada and

Mexico increased, driven by new beverage product introductions.

Net revenues increased $267 million (2.9%), due to favorable

currency ($120 million), higher volume/mix ($82 million) and

higher pricing ($65 million, including the impact of increased

promotional spending).

Operating companies income increased $20 million (0.9%), due

primarily to the 2002 pre-tax charges for asset impairment and

exit costs ($60 million), the impact of lower integration costs and

aloss on the sale of a food factory ($40 million) and favorable

currency ($22 million), partially offset by unfavorable costs, net

of higher pricing ($72 million, including higher commodity costs

and increased promotional spending), higher fixed manufacturing

costs ($23 million, including higher benefit costs) and unfavorable

volume/mix.

Biscuits, Snacks and Confectionery: Volume decreased 4.7%,

due primarily to lower shipments in biscuits and the divestiture of a

small confectionery business in 2002. In biscuits, volume declined,

due primarily to reduced consumption in cookies, reflecting higher

pricing, lower impact of new products, and consumer health and

wellness concerns. Snacks volume increased, benefiting from

category and consumption gains in snack nuts.

Net revenues decreased $86 million (1.8%), due to lower volume/mix

($56 million), the divestiture of a small confectionery business in

2002 ($21 million) and higher promotional spending, net of higher

pricing ($9 million).

Operating companies income decreased $164 million (15.6%),

due primarily to lower volume/mix ($84 million), higher fixed

manufacturing costs ($77 million) and unfavorable costs, net

of higher pricing ($71 million, including higher commodity costs

and increased promotional spending), partially offset by lower

marketing, administration and research costs ($77 million).

Beverages, Desserts and Cereals: Volume increased 5.3%, due

primarily to higher shipments of ready-to-drink beverages, which

were aided by new product introductions. Desserts volume also

increased, due primarily to higher shipments of sugar-free items

and increased merchandising programs. In coffee, volume declined,

impacted by competitive activity and a category decline due to

higher prices.

Net revenues increased $155 million (3.5%), due to higher

volume/mix ($100 million) and higher pricing ($55 million).

Operating companies income increased $111 million (9.8%), due

primarily to the impact of lower integration costs ($59 million),

the 2002 asset impairment and exit costs ($47 million) and higher

volume/mix ($43 million), partially offset by higher marketing,

administration and research costs ($31 million), unfavorable

costs, net of higher pricing ($13 million, including higher commodity

costs) and higher benefit costs.

Oscar Mayer and Pizza: Volume increased 1.0%, due primarily to

gains in cold cuts, hot dogs, bacon, soy-based meat alternatives

and frozen pizza.

Net revenues increased $86 million (2.9%), due primarily to higher

volume/mix ($44 million) and higher pricing ($40 million, including the

impact of increased promotional spending).

Operating companies income was equal to the prior year’s, as the

impact of 2002 pre-tax charges for asset impairment and exit

costs ($25 million) and integration costs ($7 million), lower fixed

manufacturing costs ($14 million) and higher volume/mix ($10 million)

was offset by higher marketing, administration and research costs

($51 million), unfavorable costs, net of higher pricing ($5 million,

including higher commodity costs and increased promotional

spending) and higher benefit costs.

2002 compared with 2001

The following discussion compares KFNA’s operating results for

2002 with 2001.

KFNA’s volume increased 8.2%, due primarily to the inclusion

in 2002 of a business that was previously held for sale and

contributions from new products.

Net revenues increased $515 million (2.5%), due primarily to

higher volume/mix ($437 million) and the inclusion in 2002 of a

business that was previously held for sale ($252 million), partially

offset by lower selling prices in response to lower commodity

costs ($154 million).

30