Kraft 2003 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2003 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66

|

|

55

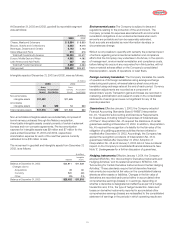

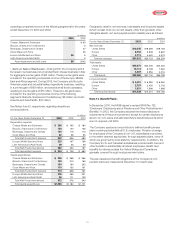

Components of Net Periodic Benefit Cost

Net periodic pension (income) cost consisted of the following for the

years ended December 31, 2003, 2002 and 2001:

(in millions) U.S. Plans Non-U.S. Plans

2003 2002 2001 2003 2002 2001

Service cost $135 $120 $ 107 $58 $49 $45

Interest cost 338 339 339 136 120 112

Expected return

on plan assets (587) (631) (648) (146) (134) (126)

Amortization:

Unrecognized net

loss (gain)

from experience

differences 15 8(21) 18 5(1)

Prior service cost 218875

Other expense (income) 51 130 (12)

Net pension

(income) cost $(46) $(33) $(227) $74 $47 $35

Retiring employees elected lump-sum payments, resulting in

settlement losses of $51 million and $21 million in 2003 and 2002,

respectively, and settlement gains of $12 million in 2001. In addition,

during 2002, certain salaried employees in the United States left the

Company under a voluntary early retirement program instituted in

2001. This resulted in special termination benefits and curtailment

and settlement losses of $109 million in 2002.

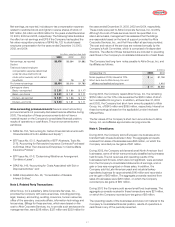

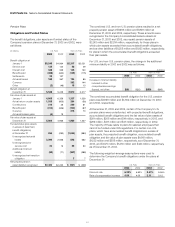

The following weighted-average assumptions were used to

determine the Company’s net pension cost for the year ended

December 31:

U.S. Plans Non-U.S. Plans

2003 2002 2001 2003 2002 2001

Discount rate 6.50% 7.00% 7.75% 5.56% 5.80% 5.88%

Expected rate of

return on plan assets 9.00 9.00 9.00 8.41 8.49 8.51

Rate of compensation

increase 4.00 4.50 4.50 3.12 3.36 3.55

The Company’s expected rate of return on plan assets is determined

by the plan assets’ historical long-term investment performance,

current asset allocation and estimates of future long-term returns

by asset class.

Kraft and certain of its subsidiaries sponsor employee savings plans,

to which the Company contributes. These plans cover certain

salaried, non-union and union employees. The Company’s

contributions and costs are determined by the matching of

employee contributions, as defined by the plans. Amounts charged

to expense for defined contribution plans totaled $84 million,

$64 million and $63 million in 2003, 2002 and 2001, respectively.

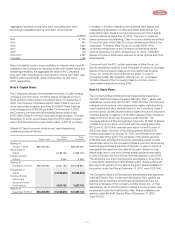

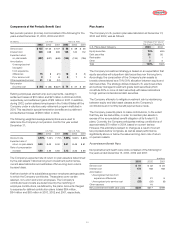

Plan Assets

The Company’s U.S. pension plan asset allocation at December 31,

2003 and 2002, was as follows:

Percentage of Fair Value of

Plan Assets at December 31

U.S. Plans Asset Category 2003 2002

Equity securities 70% 63%

Debt securities 26 32

Real estate 11

Other 34

Total 100% 100%

The Company’s investment strategy is based on an expectation that

equity securities will outperform debt securities over the long term.

Accordingly, the composition of the Company’s plan assets is

broadly characterized as a 70%/30% allocation between equity and

debt securities. The strategy utilizes indexed U.S. equity securities

and actively managed investment grade debt securities (which

constitute 80% or more of debt securities) with lesser allocations

to high yield and international debt securities.

The Company attempts to mitigate investment risk by rebalancing

between equity and debt asset classes as the Company’s

contributions and monthly benefit payments are made.

The Company presently plans to make contributions, to the extent

that they are tax deductible, in order to maintain plan assets in

excess of the accumulated benefit obligation of its funded U.S.

plans. Currently, the Company anticipates making contributions of

approximately $70 million in 2004, based on current tax law.

However, this estimate is subject to change as a result of current

tax proposals before Congress, as well as asset performance

significantly above or below the assumed long-term rate of return

on pension assets.

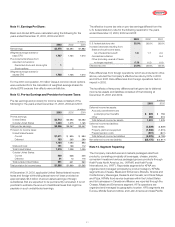

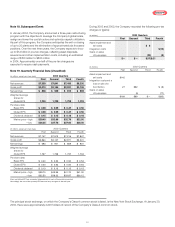

Postretirement Benefit Plans

Net postretirement health care costs consisted of the following for

the years ended December 31, 2003, 2002 and 2001:

(in millions)

2003 2002 2001

Service cost $41 $32 $34

Interest cost 173 168 168

Amortization:

Unrecognized net loss from

experience differences 40 21 5

Unrecognized prior service cost (25) (20) (8)

Other expense 16

Net postretirement health care costs $229 $217 $199