JetBlue Airlines 2007 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2007 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

our holding securities beyond their next scheduled auction reset dates if a secondary market does not

develop; therefore, limiting the short-term liquidity of these investments.

We are exposed to the effect of changes in the price and availability of aircraft fuel. To manage

this risk, we periodically purchase crude or heating oil option contracts or swap agreements. Prices for

these commodities are normally highly correlated to aircraft fuel, making derivatives of them effective

at offsetting aircraft fuel prices to provide some short-term protection against a sharp increase in

average fuel prices. The fair values of our derivative instruments are estimated through the use of

standard option value models and/or present value methods with underlying assumptions based on

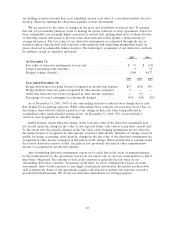

prices observed in commodity futures markets. The following is a summary of our derivative contracts

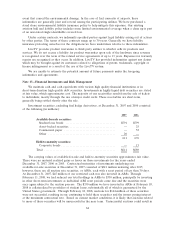

(in millions, except as otherwise indicated):

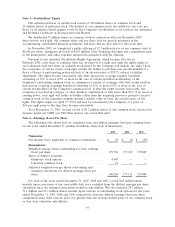

2007 2006

At December 31:

Fair value of derivative instruments at year end ......................... $ 33 $ (15)

Longest remaining term (months) ..................................... 9 12

Hedged volume (barrels) ............................................. 1,506 4,077

2007 2006 2005

Year ended December 31:

Hedge effectiveness net gains (losses) recognized in aircraft fuel expense . . $35 $(4) $43

Hedge ineffectiveness net gains recognized in other income (expense) .... 5 — —

Other fuel derivative net losses recognized in other income (expense)..... — (5) —

Percentage of actual consumption economically hedged ................. 59%64%22%

As of December 31, 2007, 100%of our outstanding derivative contracts were designated as cash

flow hedges for accounting purposes. While outstanding, these contracts are recorded at fair value on

the balance sheet with the effective portion of the change in their fair value being reflected in

accumulated other comprehensive income (loss). At December 31, 2006, 93%of our derivative

contracts were designated as cash flow hedges.

Ineffectiveness results when the change in the total fair value of the derivative instrument does

not exactly equal the change in the value of our expected future cash outlays to purchase aircraft fuel.

To the extent that the periodic changes in the fair value of the hedging instruments are not effective,

the ineffectiveness is recognized in other income (expense) immediately. Likewise, if a hedge ceases to

qualify for hedge accounting, those periodic changes in the fair value of the derivative instruments are

recognized in other income (expense) in the period of the change. When aircraft fuel is consumed and

the related derivative contract settles, any gain or loss previously deferred in other comprehensive

income is recognized in aircraft fuel expense.

Any outstanding derivative instruments expose us to credit loss in the event of nonperformance

by the counterparties to the agreements, but we do not expect any of our four counterparties to fail to

meet their obligations. The amount of such credit exposure is generally the fair value of our

outstanding derivatives contracts. To manage credit risks, we select counterparties based on credit

assessments, limit overall exposure to any single counterparty and monitor the market position with

each counterparty. Some of our agreements require cash deposits if market risk exposure exceeds a

specified threshold amount. We do not use derivative instruments for trading purposes.

65