Honda 2009 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2009 Honda annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Liquidity and Capital Resources

Overview of Capital Requirements, Sources and Uses

The policy of Honda is to support its business activities by

maintaining suffi cient capital resources, a suffi cient level of

liquidity and a sound balance sheet.

Honda’s main business is the manufacturing and sale of

motorcycles, automobiles and power products. To support this

business, it also provides retail fi nancing and automobile

leasing services for customers, as well as wholesale fi nancing

services for dealers.

Honda requires operating capital mainly to purchase parts

and raw materials required for production, as well as to

maintain inventory of fi nished products and cover receivables

from dealers. Honda also requires funds for capital

expenditures, mainly to introduce new models, upgrade,

rationalize and renew production facilities, as well as to expand

and reinforce sales and R&D facilities.

Honda meets its operating capital requirements primarily

through cash generated by operations, bank loans and the

issuance of commercial paper. Year-end balance of liabilities

associated with the Company and its subsidiaries’ funding for

non-fi nancial services businesses was ¥766.6 billion as of

March 31, 2009. In addition, the Company’s fi nance

subsidiaries fund those fi nancial programs for customers and

dealers primarily from corporate bonds, medium-term notes,

commercial paper, securitization of fi nance receivables and

intercompany loans. Year-end balance of liabilities associated

with these fi nance subsidiaries’ funding for fi nancial services

business was ¥4,515.8 billion as of March 31, 2009.

Cash Flows

Consolidated cash and cash equivalents for the year ended

March 31, 2009 decreased by ¥360.5 billion from March 31,

2008, to ¥690.3 billion. The reasons for the increases or

decreases for each cash fl ow activity are as follows.

Net cash provided by operating activities amounted to

¥383.6 billion of cash infl ows. Cash infl ows from operating

activities decreased by ¥743.2 billion compared with the

previous fi scal year, due mainly to a decrease in cash received

from customers, primarily due to lower unit sales in the

automobile business in North America and an increase in

inventories, which was offset by decreased payments for parts

and raw materials primarily due to a decrease in automobile

production and decreased payments for operating expenses.

Net cash used in investing activities amounted to ¥1,133.3

billion of cash outfl ows, due mainly to capital expenditures and

the purchase of operating lease assets (which exceeds

proceeds from sales of operating lease assets), which was

offset by collections of and proceeds from sales of fi nance

subsidiaries-receivables (which exceeded acquisitions of

fi nance subsidiaries-receivables). Cash outfl ows from investing

activities decreased by ¥553.0 billion compared with the

previous fi scal year, due mainly to a decrease in acquisitions of

fi nance subsidiaries-receivables and the purchases of operating

lease assets and an increase in proceeds from sales of fi nance

subsidiaries-receivables and operating lease assets.

Net cash provided by fi nancing activities amounted to ¥530.8

billion of cash infl ows, due mainly to proceeds from long-term

debt and increase in short-term debt (which exceeded

repayment of long-term debt), which was offset by cash

dividends paid. Cash infl ows from fi nancing activities decreased

by ¥157.1 billion compared with the previous fi scal year.

Liquidity

The ¥690.3 billion in cash and cash equivalents at the end of

year corresponds to approximately 0.8 month of net sales, and

Honda believes it has suffi cient liquidity for its business

operations.

At the same time, Honda is aware of the possibility that

various factors, such as recession-induced market contraction

and fi nancial and foreign exchange market volatility, may

adversely affect liquidity. For this reason, fi nance subsidiaries

that carry total short-term borrowings of ¥1,697.4 billion have

committed lines of credit equivalent to ¥864.5 billion that serve

as alternative liquidity for the commercial paper issued regularly

to replace debt. Honda believes it currently has suffi cient credit

limits, extended by prominent international banks as of the date

of the fi ling of Honda’s form 20-F.

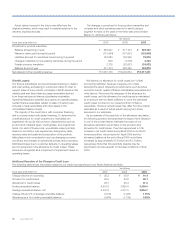

Honda’s short- and long-term debt securities are rated by

credit rating agencies, such as Moody’s Investors Service, Inc.,

Standard & Poor’s Rating Services, and Rating and Investment

Information, Inc. The following table shows the ratings of

Honda’s unsecured debt securities by Moody’s, Standard &

Poor’s and Rating and Investment Information as of March 31,

2009.

Credit Ratings for

Short-term

unsecured

debt securities

Long-term

unsecured

debt securities

Moody’s Investors Service P-1 A1

Standard & Poor’s Rating Services A-1 A+

Rating and Investment Information a-1+ AA

The above ratings are based on information provided by

Honda and other information deemed credible by the rating

agencies. They are also based on the agencies’ assessment of

credit risk associated with designated securities issued by

Honda. Each rating agency may use different standards for

calculating Honda’s credit rating, and also makes its own

assessment. Ratings can be revised or nullifi ed by agencies at

any time. These ratings are not meant to serve as a

recommendation for trading in or holding Honda’s unsecured

debt securities.

Off-Balance Sheet Arrangements

Special Purpose Entity

For the purpose of accelerating the receipt of cash related to

our fi nance receivables, we periodically securitize and sell pools

of these receivables. In these securitizations, we sell a portfolio

of fi nance receivables to a special purpose entity, which is

established for the limited purpose of buying and reselling

fi nance receivables. We remain as a servicer of the fi nance

receivables and are paid a servicing fee for our services. The

special purpose entity transfers the receivables to a trust or

bank conduit, which issues interest-bearing asset-backed

securities or commercial paper, respectively, to investors. We

retain certain subordinated interests in the sold receivables in

the form of subordinated certifi cates, servicing assets and

residual interests in certain cash reserves provided as credit

enhancements for investors. We apply signifi cant assumptions

regarding prepayments, credit losses and average interest

Annual Report 2009

56