Holiday Inn 2003 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2003 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68

|

|

57

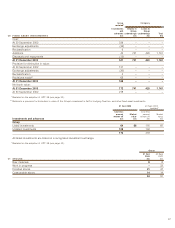

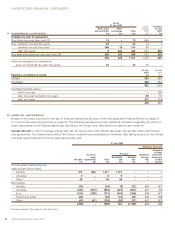

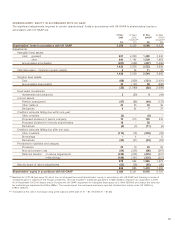

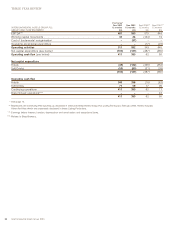

Fixed asset investments

Fixed asset investments are stated at cost less any provision

for diminution in value. Under US GAAP, these investments are

recorded at market value and unrealised gains and losses are

reported in other comprehensive income except for other than

temporary which are recognised in the profit and loss account.

Derivative instruments and hedging

The Group enters into derivative instruments to limit its exposure

to interest rate and foreign exchange risk. Under UK GAAP,

these instruments are measured at cost and accounted for

as hedges, whereby gains and losses are deferred until the

underlying transaction occurs. Under US GAAP, all derivative

instruments (including those embedded in other contracts) are

recognised on the balance sheet at their fair values. Changes

in fair value are recognised in net income unless specific hedge

criteria are met. If a derivative qualifies for hedge accounting as

defined under US GAAP, changes in fair value are recognised

periodically in net income or in shareholders’ equity as a

component of other comprehensive income depending on

whether the derivative qualifies as a fair value or cash flow

hedge. Substantially all derivatives held by the Group during

the year did not qualify for hedge accounting under US GAAP.

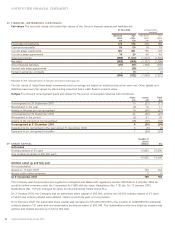

Guarantees

The Group gives guarantees in connection with obtaining long-

term management contracts. Under UK GAAP, a contingent

liability under such guarantees is not recognised unless it is

probable that it will result in a future loss to the Group. For

the purposes of US GAAP, under FASB interpretation (FIN) 45

‘Guarantors Accounting and Disclosure Requirements for

Guarantees, Including Direct Guarantees of Indebtedness of

Others in the Year’, at the inception of guarantees issued after

31 December 2002, the Group would record the fair value of

the guarantee as an asset and a liability, which are amortised

over the life of the contract.

Proposed dividends

Final ordinary dividends are provided for in the year in

respect of which they are proposed by the Board for approval

by the shareholders. Under US GAAP, dividends would not

be provided for until the year in which they are declared.

Exceptional items

Certain exceptional items are shown on the face of the profit

and loss account after operating profit. Under US GAAP these

items would be classified as operating profit or expenses.

Discontinued operations

For the purposes of the reconciliation on page 58 the

discontinued operations are the same for both UK and US GAAP.

DIFFERENCES BETWEEN UNITED KINGDOM AND

UNITED STATES GENERALLY ACCEPTED ACCOUNTING

PRINCIPLES (CONTINUED)

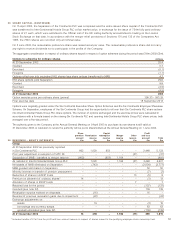

would account for sales of real estate in accordance with

FAS 66 ‘Accounting for Sales of Real Estate’. Gains on sales

of real estate are deferred if there is a continuing involvement

with the property. Consequently the Group has reduced gains

on sales where this criteria exists.

Staff costs

The Group charges against earnings the cost of shares

acquired to settle awards under certain incentive schemes.

The charge is based on an apportionment of the cost of

shares over the period of the scheme. Prior to Separation the

Group accounted for those plans under the recognition and

measurement provisions of Accounting Principles Board (APB)

Opinion 25 ‘Accounting for Stock Issue to Employees’ and

related interpretations. Under APB 25 these awards would be

accounted for as variable plans and the charge would be based

on the intrinsic value of the shares using the share price at the

balance sheet date. Effective from the date of Separation, the

Group adopted the preferable fair value recognition provisions

of FAS 123 ‘Accounting for Stock-Based Compensation’.

The Group selected the modified prospective method of

adoption described in FAS 148 ‘Accounting for Stock-Based

Compensation – Transition and Disclosure’. Compensation cost

recognised since Separation is the same as that which would

have been recognised had the fair value method of FAS 123

been applied from its original effective date. In accordance

with the modified prospective method of adoption, results

for years prior to 2002 have not been restated.

Severance and restructuring costs

Under UK GAAP, severance costs are provided for in the

financial statements if it is determined that a constructive or

legal obligation has arisen from a restructuring programme

where it is probable that it will result in the outflow of economic

benefits and the costs involved can be estimated with

reasonable accuracy. Under US GAAP, severance costs are

recognised over the remaining service period to termination.

Accordingly, timing differences between UK and US GAAP

arise on the recognition of such costs.

Deferred taxation

The Group provides for deferred taxation in respect of timing

differences, subject to certain exceptions, between the

recognition of gains and losses in the financial statements

and for tax purposes. Timing differences recognised, include

accelerated capital allowances, unrelieved tax losses and

short-term timing differences. Under US GAAP, deferred

taxation would be computed on all differences between the

tax bases and book values of assets and liabilities which

will result in taxable or tax deductible amounts arising in

future years. Deferred taxation assets under UK GAAP and

US GAAP are recognised only to the extent that it is more

likely than not that they will be realised.