Holiday Inn 2003 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2003 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

32 InterContinental Hotels Group 200332 InterContinental Hotels Group 2003

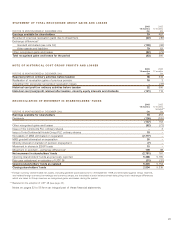

ACCOUNTING POLICIES

BASIS OF PREPARATION

Separation transaction On 15 April 2003, following

shareholder and regulatory approval, Six Continents PLC

separated into two new listed groups, InterContinental Hotels

Group PLC (IHG) comprising the Hotels and Soft Drinks

businesses and Mitchells & Butlers plc (MAB) comprising the

Retail and Standard Commerical Property Developments

(SCPD) businesses. The mechanics of the Separation are

detailed below.

The legal structure of the transaction was such that Mitchells &

Butlers plc acquired 100% of the issued share capital of Six

Continents PLC following implementation of a Court approved

Scheme of Arrangement under Section 425 of the Companies

Act 1985. Shareholders of Six Continents PLC were allotted

one Mitchells & Butlers plc share and an entitlement to a cash

payment of 81p per share for each Six Continents PLC share

held. This resulted in the issue of 866,665,032 Mitchells &

Butlers plc ordinary shares of £4.20 each plus an undertaking

to pay £702m in cash.

On 12 April 2003, Six Continents PLC transferred the Retail and

SCPD businesses to Mitchells & Butlers plc for £1,744m and also

paid a dividend to Mitchells & Butlers plc of the same amount.

On 13 April 2003, the ordinary share capital of Mitchells &

Butlers plc was sub-divided and consolidated on a 50 to 59

basis which resulted in a reduction of the number of ordinary

shares in issue to 734,461,900 with each share having a

nominal value of £4.956.

On 15 April 2003, Mitchells & Butlers plc investment in Six

Continents PLC was revalued to its market value. On the same

day, the Court approved a reduction in the capital of Mitchells

& Butlers plc. An amount equivalent to the market value of Six

Continents PLC was returned to shareholders by the transfer of

Six Continents PLC to InterContinental Hotels Group PLC and

the issue by InterContinental Hotels Group PLC of ordinary

shares to the shareholders.

The Company issued 734,461,900 ordinary £1 shares, which

were recorded at nominal value. In accordance with Sections

131 and 133 of the Companies Act 1985, no premium was

recognised on the shares issued. On consolidation, the

difference between the nominal value of the Company’s shares

issued and the amount of the share capital, share premium

and capital redemption reserve of £1,164m at the date of

Separation has been credited to the merger reserve.

Merger accounting The consolidated financial statements have

been prepared in accordance with the principles of merger

accounting as applicable to group reorganisations as set out in

Financial Reporting Standard (FRS) 6 ‘Acquisitions and

Mergers’ as if the Group had been in existence throughout the

periods presented. The financial statements have been

prepared under merger accounting principles in order to

present a true and fair view of the Group’s results and financial

position, which has required the Group to utilise the overriding

requirement of Section 227(6) of the Companies Act 1985.

The true and fair override requirement has been utilised as the

Separation transaction has been accounted for using merger

accounting principles as applicable to group reorganisations,

although it does not satisfy all the conditions required under

Schedule 4A of the Companies Act 1985 and FRS 6. Mitchells

& Butlers plc acquired Six Continents PLC for consideration

that included a non-share element equivalent to more than 10%

of the nominal value of the share element of the consideration.

Schedule 4A and FRS 6 require such transfers to be accounted

for using acquisition accounting principles which would have

resulted in the restatement at fair value of the assets and

liabilities acquired, the recognition of goodwill and the

consolidation of post acquisition results only. In the opinion of

the directors, as the rights of shareholders were not affected

by these internal company transfers, the financial statements

would fail to give a true and fair view of the Group’s results

and financial position if acquisition accounting had been used.

The effects of this departure cannot reasonably be quantified.

The consolidated financial statements are therefore presented

as if the Company had been the parent company of the Group

throughout the periods presented. The results of Mitchells &

Butlers plc have been included in discontinued operations for

all years up until the date of Separation.

BASIS OF ACCOUNTING

The financial statements are prepared under the historical cost

convention as modified by the revaluation of certain tangible

fixed assets. They have been drawn up to comply with applicable

accounting standards, including Urgent Issues Task Force

(UITF) Abstract 38 ‘Accounting for ESOP Trusts’.

Pension provisions previously included in debtors and

creditors: amounts falling due after one year have been

reclassified within other provisions for liabilities and charges.

Prior year comparatives have been restated. There has been

no overall impact on the Group’s net assets or profit and

loss account.

NEW ACCOUNTING POLICIES

UITF 38 ‘Accounting for ESOP Trusts’ was adopted for the first

time this period. UITF 38 requires that ESOP shares should be

deducted from shareholders’ funds rather than being shown

as an asset. This change in accounting policy has been

accounted for as a prior year adjustment and previously

reported figures have been restated accordingly. The effect

has been to decrease the Group’s net assets by £31m in

2002 with no impact on the profit and loss account.