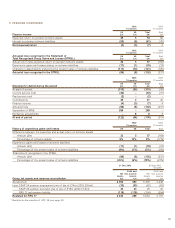

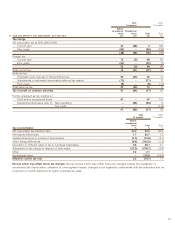

Holiday Inn 2003 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2003 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

3333

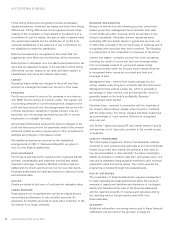

BASIS OF CONSOLIDATION

The Group financial statements comprise the financial

statements of the parent company and its subsidiary

undertakings. The results of those businesses acquired or

disposed of during the period are consolidated for the period

during which they were under the Group’s dominant influence.

FOREIGN CURRENCIES

Transactions in foreign currencies are recorded at the exchange

rates ruling on the dates of the transactions, adjusted for the

effects of any hedging arrangements. Assets and liabilities

denominated in foreign currencies are translated into sterling at

the relevant rates of exchange ruling at the balance sheet date.

The results of overseas operations are translated into sterling

at weighted average rates of exchange for the period.

Exchange differences arising from the retranslation of opening

net assets (including any goodwill previously eliminated against

reserves) denominated in foreign currencies and foreign

currency borrowings and currency swap agreements used to

hedge those assets are taken directly to reserves. All other

exchange differences are taken to the profit and loss account.

TREASURY INSTRUMENTS

Net interest arising on interest rate agreements is taken to the

profit and loss account.

Premiums payable on interest rate agreements are charged to the

profit and loss account over the term of the relevant agreements.

Currency swap agreements are retranslated at exchange rates

ruling at the balance sheet date with the net amount being

included in either current asset investments or borrowings.

Interest payable or receivable arising from currency swap

agreements is taken to the profit and loss account on a gross

basis over the term of the relevant agreements.

Gains or losses arising on forward exchange contracts are

taken to the profit and loss account in line with the transactions

they are hedging.

FIXED ASSETS AND DEPRECIATION

i Goodwill Any excess of purchase consideration for an

acquired business over the fair value attributed to its separately

identifiable assets and liabilities represents goodwill. Goodwill

is capitalised as an intangible asset. Goodwill arising on

acquisitions prior to 30 September 1998 was eliminated against

reserves. To the extent that goodwill denominated in foreign

currencies continues to have value, it is translated into sterling

at each balance sheet date and any movements are accounted

for as set out under ‘foreign currencies’ above. On disposal of a

business, any goodwill relating to the business and previously

eliminated against reserves, is taken into account in

determining the profit or loss on disposal.

ii Other intangible assets On acquisition of a business, no

value is attributed to other intangible assets which cannot be

separately identified and reliably measured. No value is

attributed to internally generated intangible assets.

iii Tangible assets Freehold and leasehold land and buildings

are stated at cost, or valuation, less depreciation. All other

fixed assets are stated at cost less depreciation. Repairs and

maintenance costs are expensed as incurred.

When implementing FRS 15 ‘Tangible Fixed Assets’ in the year

to 30 September 2000, the Group did not adopt a policy of

revaluing properties. The transitional rules of FRS 15 were

applied so that the carrying values of properties include an

element resulting from previous valuations.

iv Revaluation Surpluses or deficits arising from previous

professional valuations of properties, realised on the disposal

of an asset, are transferred from the revaluation reserve to the

profit and loss account reserve.

v Impairment Any impairment arising on an income-generating

unit, other than an impairment which represents a consumption

of economic benefits, is eliminated against any specific

revaluation reserve relating to the impaired assets in that

income-generating unit with any excess being charged to the

profit and loss account.

vi Depreciation and amortisation Goodwill and other

intangible assets are amortised over their estimated useful

lives, generally 20 years.

Freehold land is not depreciated. All other tangible fixed assets

are depreciated to a residual value over their estimated useful

lives, namely:

Freehold buildings 50 years

Leasehold buildings lesser of unexpired

term of lease and

50 years

Fixtures, fittings and equipment 3-25 years

Plant and machinery 4-20 years

All depreciation and amortisation is charged on a straight line

basis.

vii Investments Fixed asset investments are stated at cost less

any provision for diminution in value.

DEFERRED TAXATION

Deferred tax assets and liabilities are recognised, subject to

certain exceptions, in respect of all material timing differences

between the recognition of gains and losses in the financial

statements and for tax purposes.