Haier 2010 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2010 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

|

|

31 December 2010

二零一零年十二月三十一日

NOTES TO FINANCIAL STATEMENTS

財務報表附註

Annual Report 2010 二零一零年年報

HAIER ELECTRONICS GROUP CO., LTD 海爾電器集團有限公司

88

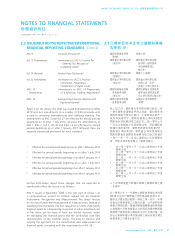

2.3 ISSUED BUT NOT YET EFFECTIVE INTERNATIONAL

FINANCIAL REPORTING STANDARDS (Cont’d)

In November 2010, the IASB issued additions to IFRS 9 to address

financial liabilities (the “Additions”) and incorporated in IFRS 9 the

current derecognition principles of financial instruments of IAS 39.

Most of the Additions were carried forward unchanged from IAS 39,

while changes were made to the measurement of financial liabilities

designated at fair value through profit or loss using the fair value

option (“FVO”). For these FVO liabilities, the amount of change in

the fair value of a liability that is attributable to changes in credit

risk must be presented in other comprehensive income (“OCI”).

The remainder of the change in fair value is presented in profit or

loss, unless presentation of the fair value change in respect of the

liability’s credit risk in OCI would create or enlarge an accounting

mismatch in profit or loss. However, loan commitments and financial

guarantee contracts which have been designated under the FVO

are scoped out of the Additions.

IAS 39 is aimed to be replaced by IFRS 9 in its entirety. Before this

entire replacement, the guidance in IAS 39 on hedge accounting

and impairment of financial assets continues to apply. The Group

expects to adopt IFRS 9 from 1 January 2013.

IAS 24 (Revised) clarifies and simplifies the definition of related

parties. It also provides for a partial exemption of related party

disclosure to government-related entities for transactions with the

same government or entities that are controlled, jointly controlled

or significantly influenced by the same government. The Group

expects to adopt IAS 24 (Revised) from 1 January 2011.

Improvements to IFRSs 2010 issued in May 2010 sets out

amendments to a number of IFRSs. The Group expects to adopt the

amendments from 1 January 2011. There are separate transitional

provisions for each standard. While the adoption of some of the

amendments may result in changes in accounting policies, none

of these amendments are expected to have a significant financial

impact on the Group. Those amendments that are expected to have

a significant impact on the Group’s policies are as follows:

2.3 已頒佈但尚未生效之國際財務報

告準則

(續)

於二零一零年十一月,國際會計師公會就財務

負債頒佈國際財務報告準則第9號之新增規定

(「新增規定」),並將國際會計準則第39號財務

工具之現有取消確認原則納入國際財務報告準

則第9號內,因此指定為按公平值計入損益之

財務負債之計量將透過公平值選擇(「公平值選

擇」)計算。就該等公平值選擇負債而言,由信

貸風險變動而產生之負債公平值變動金額,必

須於其他全面收益(「其他全面收益」)中呈列。

除非於其他全面收益中就負債之信貸風險呈列

公平值變動,會於損益中產生或擴大會計差

異,否則其餘公平值變動金額於損益呈列。然

而,新增規定並不涵蓋按公平值選擇納入之貸

款承諾及財務擔保合約。

國際財務報告準則第9號旨在完全取代國際會計

準則第39號。於全面取代前,國際會計準則第

39號於對沖會計及財務資產之減值方面之指引

繼續適用。本集團預期自二零一三年一月一日

起採納國際財務報告準則第9號。

國際會計準則第24號(經修訂)闡明及簡化關連

人士之定義。該經修訂之準則亦為與政府有關

之實體提供部分豁免,豁免披露與由同一政府

控制、共同控制或受同一政府重大影響之相同

政府或實體之所有交易詳情及結餘。本集團預

期自二零一一年一月一日起採納國際會計準則

第24號(經修訂)。

於二零一零年五月頒佈對

二零一零年國際財務

報告準則之改進

,載有對多項國際財務報告準

則之修訂。本集團預期自二零一一年一月一日

起採納有關修訂。各項準則有獨立之過渡條

文。雖然採納若干修訂可能導致會計政策發生

變動,惟預期該等修訂概不會對本集團構成任

何重大財務影響。預期對本集團之政策產生重

大影響之修訂如下: