Haier 2010 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2010 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

|

|

31 December 2010

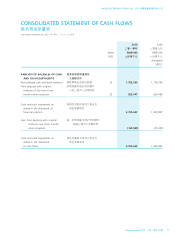

二零一零年十二月三十一日

NOTES TO FINANCIAL STATEMENTS

財務報表附註

HAIER ELECTRONICS GROUP CO., LTD 海爾電器集團有限公司

Annual Report 2010 二零一零年年報 87

2.3 ISSUED BUT NOT YET EFFECTIVE INTERNATIONAL

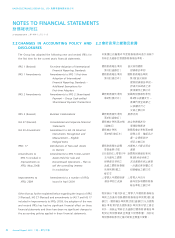

FINANCIAL REPORTING STANDARDS (Cont’d)

IFRS 9 Financial Instruments

6

IAS 12 Amendments Amendments to IAS 12 Income Tax

– Deferred Tax: Recovery of

Underlying Assets

5

IAS 24 (Revised) Related Party Disclosures

3

IAS 32 Amendment Amendment to IAS 32 Financial

Instruments: Presentation –

Classification of Rights Issues

1

IFRIC 14 Amendments to IFRIC 14 Prepayments

Amendments of a Minimum Funding Requirement

3

IFRIC 19 Extinguishing Financial Liabilities with

Equity Instruments

2

Apart from the above, the IASB has issued Improvements to IFRSs

2010 sets out amendments to a number of IFRSs primarily with

a view to removing inconsistencies and clarifying wording. The

amendments to IFRS 3 and IAS 27 are effective for annual periods

beginning on or after 1 July 2010, whereas the amendments to

IFRS 1, IFRS 7, IAS 1, IAS 34 and IFRIC 13 are effective for annual

periods beginning on or after 1 January 2011 although there are

separate transitional provisions for each standard.

1 Effective for annual periods beginning on or after 1 February 2010

2 Effective for annual periods beginning on or after 1 July 2010

3 Effective for annual periods beginning on or after 1 January 2011

4 Effective for annual periods beginning on or after 1 July 2011

5 Effective for annual periods beginning on or after 1 January 2012

6 Effective for annual periods beginning on or after 1 January 2013

Further information about those changes that are expected to

significantly affect the Group is as follows:

IFRS 9 issued in November 2009 is the first part of phase 1 of

a comprehensive project to entirely replace IAS 39 Financial

Instruments: Recognition and Measurement. This phase focuses

on the classification and measurement of financial assets. Instead of

classifying financial assets into four categories, an entity shall classify

financial assets as subsequently measured at either amortised cost

or fair value, on the basis of both the entity’s business model

for managing the financial assets and the contractual cash flow

characteristics of the financial assets. This aims to improve and

simplify the approach for the classification and measurement of

financial assets compared with the requirements of IAS 39.

2.3 已頒佈但尚未生效之國際財務報

告準則

(續)

國際財務報告準則

財務工具

6

第9號

國際會計準則第12號 國際會計準則第12號

(修訂本)

所得稅—遞延稅項:

收回相關資產

之

修訂本

5

國際會計準則第24號

關連人士披露

3

(經修訂)

國際會計準則第32號 國際會計準則第32號

(修訂本)

財務工具,呈列-

供股之分類

之修訂本

1

國際財務報告詮釋 國際財務報告詮譯委員

委員會第14號 會第14號

最低資金要

(修訂本)

求之預付款項

之修訂本

3

國際財務報告詮釋

以權益工具清償財務

委員會第19號

負債

2

除上述之外,國際會計準則委員會已發出

二零

一零年國際財務報告準則之改進

,載列對多項

國際財務報告準則之修訂,主要是為去除不一

致性和澄清用字。國際財務報告準則第3號及

國際會計準則第27號之修訂於二零一零年七月

一日或以後開始之年度期間生效,而對國際財

務報告準則第1號、國際財務報告準則第7號、

國際會計準則第1號、國際會計準則第34號及

國際財務報告詮釋委員會第13號之修訂則會於

二零一一年一月一日或以後開始之年度期間生

效,即使各項準則有獨立之過渡性條文。

1 於二零一零年二月一日或以後開始之年度

期間生效

2 於二零一零年七月一日或以後開始之年度

期間生效

3 於二零一一年一月一日或以後開始之年度

期間生效

4 於二零一一年七月一日或以後開始之年度

期間生效

5 於二零一二年一月一日或以後開始之年度

期間生效

6 於二零一三年一月一日或以後開始之年度

期間生效

以下為預期會重大影響本集團之相關改動之進

一步資料:

於二零零九年十一月頒佈之國際財務報告準則第

9號是完全取代國際會計準則第39號

財務工具:

確認及計量

全面計劃第一階段之第一部分。本階

段專注於財務資產之分類及計量。以代替將財務

資產分類為四類,實體須根據實體管理財務資產

之業務模式及財務資產之合約現金流量特點將財

務資產分類為其後以攤銷成本或公平值計量。這

旨在比較國際會計準則第39號之規定改善及簡化

財務資產之分類和計量方法。