Haier 2010 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2010 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

|

|

31 December 2010

二零一零年十二月三十一日

NOTES TO FINANCIAL STATEMENTS

財務報表附註

Annual Report 2010 二零一零年年報

HAIER ELECTRONICS GROUP CO., LTD 海爾電器集團有限公司

86

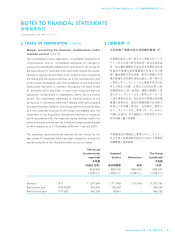

2.2 CHANGES IN ACCOUNTING POLICY AND

DISCLOSURES (Cont’d)

(b) Improvements to IFRSs 2009 issued in April 2009 sets out

amendments to a number of IFRSs. There are separate

transitional provisions for each standard. While the adoption

of some of the amendments results in changes in accounting

policies, none of these amendments has had a significant

financial impact on the Group. Details of the key amendments

most applicable to the Group are as follows:

• IAS 7 Statement of Cash Flows: Requires that only

expenditures that result in a recognised asset in the

statement of financial position can be classified as a

cash flow from investing activities.

• IAS 17 Leases: Removes the specific guidance on

classifying land as a lease. As a result, leases of land

should be classified as either operating or finance leases

in accordance with the general guidance in IAS 17.

2.3 ISSUED BUT NOT YET EFFECTIVE INTERNATIONAL

FINANCIAL REPORTING STANDARDS

The Group has not applied the following new and revised IFRSs,

that have been issued but are not yet effective, in these financial

statements.

IFRS 1 Amendment Amendment to IFRS 1 First-time

Adoption of International Financial

Reporting Standards– Limited

Exemption from Comparative

IFRS 7 Disclosures for First-time

Adopters2

IFRS 1 Amendments Amendments to IFRS 1 First-time

Adoption of International Financial

Reporting Standards – Severe

Hyperinflation and Removal of

Fixed Dates for First-time Adopters 4

IFRS 7 Amendments Amendments to IFRS 7 Financial

Instruments: Disclosures –

Transfers of Financial Assets4

2.2 會計政策之變動及披露

(續)

(b) 於二零零九年四月頒佈

二零零九年國際財

務報告準則之改進

載列對多項國際財務報

告準則之修訂。各項準則均單獨附有過渡

性規定。採納其中若干修訂將導致會計政

策變更,但該等修訂並未對本集團造成重

大財務影響。其中最適用於本集團之主要

修訂詳情如下:

• 國際會計準則第7號

現金流量表

:要

求只有會於財務狀況報表中被確認為

資產之開支方才可以分類為投資活動

引起之現金流量。

• 國際會計準則第17號

租賃

:刪除了將

土地劃分為租賃之分類指引。據此,

將土地租賃分類為經營租約或融資租

約都與國際會計準則第17號之總體

指引相一致。

2.3 已頒佈但尚未生效之國際財務報

告準則

本集團於此等財務報表內並無採納以下已頒佈

惟未生效之新訂及經修訂之國際財務報告準

則。

國際財務報告準則 國際財務報告準則

第1號(修訂本) 第1號

首次採納國際

財務報告準則-首次

採用者毋須按照國際

財務報告準則第7號

披露比較資料之有限

豁免

之修訂本2

國際財務報告準則 國際財務報告準則

第1號(修訂本) 第1號

首次採納國際

財務報告準則-嚴重

惡性通脹及就首次採

用者剔除固定日期

之

修訂本4

國際財務報告準則 國際財務報告準則

第7號(修訂本) 第7號

財務工具:

披露-財務資產轉讓

之修訂本4