Haier 2010 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2010 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

|

|

31 December 2010

二零一零年十二月三十一日

NOTES TO FINANCIAL STATEMENTS

財務報表附註

HAIER ELECTRONICS GROUP CO., LTD 海爾電器集團有限公司

Annual Report 2010 二零一零年年報 121

3. SIGNIFICANT ACCOUNTING JUDGEMENTS

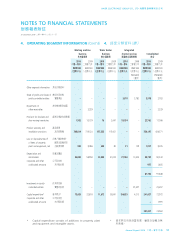

AND ESTIMATES (Cont’d)

Estimation uncertainty (Cont’d)

Impairment of receivables

The Group maintains an allowance for the estimated loss arising from

the inability of its debtors to make the required payments. The Group

makes its estimates based on the ageing of its receivable balances,

debtors’ creditworthiness, and historical write-off experience. If the

financial condition of its debtors was to deteriorate so that the

actual impairment loss might be higher than expected, the Group

would be required to revise the basis of making the allowance. At 31

December 2010, the carrying amounts of trade receivables and other

receivables were RMB3,908,094,000 (2009: RMB3,335,201,000 (as

restated); 1 January 2009: RMB2,613,909,000 (as restated)) and

RMB223,087,000 (2009: RMB50,706,000 (as restated); 1 January

2009: RMB71,500,000 (as restated)), respectively.

Write-down of inventories to net realisable value

Write-down of inventories to net realisable value is made based

on the ageing and estimated net realisable value of inventories.

The assessment of the write-down amount involves management’s

judgements and estimates. Where the actual outcome or expectation

in future is different from the original estimate, such differences will

impact the carrying value of the inventories and the write-down

charge/reversal in the period in which such estimate has been

changed. At 31 December 2010, the carrying amount of inventories

was RMB1,306,343,000 (2009: RMB389,461,000 (as restated); 1

January 2009: RMB270,711,000 (as restated)).

Product warranty and installation provisions

Product warranty and installation provisions are made based on

sales volume and past experience of the level of installation services

rendered, repairs or returns. The assessment of the provision

amount involves management’s judgements and estimates. Where

the actual outcome or expectation in future is different from

the original estimate, such differences will impact the carrying

amount of the product warranty and installation provisions and

the provision amount charged/reversed in the period in which such

estimate has been changed. At 31 December 2010, the product

warranty and installation provisions were RMB443,518,000 (2009:

RMB307,000,000; 1 January 2009: RMB239,933,000).

3. 重大會計判斷及估計

(續)

估計之不明朗因素

(續)

應收賬款減值

本集團維持其債務人未能作出所須付款而產生

之估計虧損之撥備。本集團根據應收賬款結餘

之賬齡、債務人之信譽及過往撇銷之經驗作出

估計。倘其債務人之財務狀況惡化,使實際減

值虧損可能高於預期,本集團將須修訂其作出

撥備之基準。於二零一零年十二月三十一日,

應收貿易賬款及其他應收賬款之賬面值分別為

人民幣3,908,094,000元(二零零九年:人民幣

3,335,201,000元(經 重 列);二零零九年一月

一 日: 人 民 幣2,613,909,000元( 經 重 列 ))及

人民幣223,087,000元( 二 零 零 九 年: 人 民 幣

50,706,000元(經重列);二零零九年一月一日:

人民幣71,500,000元)。

撇減存貨至可變現淨值

撇減存貨至可變現淨值乃按存貨賬齡及估計可

變現淨值而作出。評估撇減額涉及管理層之判

斷及估計。倘實際結果或未來期望與原先估計

不同,則上述差額將會對在有關估計改變期間

之存貨賬面值及撇減支出╱撥回構成影響。於

二零一零年十二月三十一日,存貨之賬面值為

人民幣1,306,343,000元(二零零九年:人民幣

389,461,000元(經重列);二零零九年一月一

日:人民幣270,711,000元(經重列))。

產品保養及安裝撥備

產品保養及安裝撥備乃按銷量及過往所提供安

裝服務、維修或退貨紀錄而作出。評估撥備額

涉及管理層之判斷及估計。倘實際結果或未來

期望與原先估計不同,則上述差額將會對在有

關估計改變期間之產品保養及安裝撥備賬面值

及撥備額支出╱撥回構成影響。於二零一零

年十二月三十一日,產品保養及安裝撥備為

人民幣443,518,000元( 二 零 零 九 年: 人 民 幣

307,000,000元;二零零九年一月一日:人民幣

239,933,000元)。