HSBC 2009 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

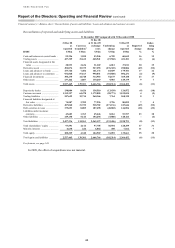

37

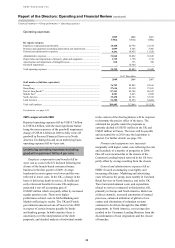

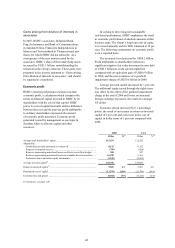

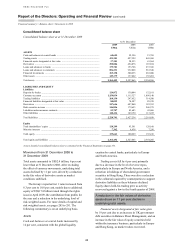

8 per cent increase in lending to customers

(excluding the financial sector and settlement

accounts).

Loan impairment charges rose significantly in

the US by 38 per cent to US$16.3 billion, due to

credit quality deterioration across all US portfolios

in Personal Financial Services.

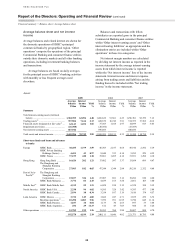

In the US consumer lending portfolio, loan

impairment charges rose as delinquency rates

deteriorated sharply and the economy declined

markedly in the second half of 2008, most notably in

the first lien portfolio. This was particularly apparent

in the geographical regions most affected by house

price depreciation and rising unemployment rates. In

mortgage services, loan impairment charges rose as

2005 and 2006 vintages matured and moved into the

later stages of delinquency. This was partly offset by

the benefit of lower balances as run-off continued,

albeit at a slowing pace as house price depreciation

restricted refinancing options for customers. In

HSBC USA, loan impairment charges rose as credit

quality worsened across the real estate secured

portfolio and private label cards. Delinquencies rose

in the prime first lien residential mortgage portfolio,

Home Equity Line of Credit and Home Equity Loan

second lien portfolios. The higher delinquency rate

for prime first lien mortgages was in part due to

lower balances following US$7.0 billion of portfolio

sales during the year.

Loan impairment charges in the US card and

retail services portfolios rose, again driven by

increasing unemployment, portfolio seasoning,

higher levels of personal bankruptcy filings and

continued weakness in the US economy which was

most apparent in regions with the most significant

declines in house prices and rising unemployment.

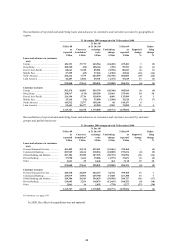

Loan impairment charges in Commercial

Banking in North America more than doubled from

a low base in 2007, due to deterioration across the

commercial real estate, middle market and corporate

banking portfolios in the US and, to a lesser extent,

higher loan impairment charges against firms in the

manufacturing, export and commercial real estate

sectors in Canada.

In the UK, a modest decline in loan impairment

charges in Personal Financial Services reflected the

non-recurrence of a methodology change at HFC in

2007 which resulted in higher impairment charges.

Credit quality in the Personal Financial Services

portfolio remained broadly stable, reflecting early

risk mitigation through the tightening of lending

controls and the sale of non-core credit card

portfolios during the year. Credit quality in the

unsecured portfolios deteriorated slightly in 2008,

particularly in the second half of the year, due to the

weakening UK economy. Loan impairment charges

in the commercial portfolio rose in 2008 as the

weakening property market led to higher impairment

charges against construction companies and

businesses dependent upon the real estate sector,

particularly in the final quarter of the year.

Impairment charges against banks rose due to some

exposure to the Icelandic banks in 2008. In addition,

rising levels of personal indebtedness resulted in

lower releases and recoveries of charges than in

2007.

Higher loan impairment and other credit risk

provisions within Global Banking and Markets in

Europe reflected increased charges against certain

corporate accounts and impairment recorded on

available-for-sale debt securities.

In Mexico, loan impairment charges rose by

US$513 million or 69 per cent, primarily in the

credit card portfolio. This was due to a combination

of higher lending volumes from organic expansion

and higher delinquency rates which were driven by

a deterioration in credit quality as the portfolio

continued to season and move into the later stages of

delinquency. Management took action to enhance

collection activity and improve the quality of new

business. Impairment charges in the commercial

portfolio also rose due to credit quality deterioration

among small and medium-sized enterprises as the

economy weakened.

In Hong Kong, the rise in loan impairment

charges was driven by weakness in parts of the

export sector within the commercial portfolio in the

second half of 2008. In Global Banking and Markets,

credit impairment charges within Balance Sheet

Management principally reflected losses on debt

securities and paper issued by financial institutions

previously rated at investment grade which failed in

the year.

In Rest of Asia-Pacific, the growth in loan

impairment charges reflected a combination of the

expansion of consumer lending and credit quality

deterioration in India and the Middle East. In

addition, higher impairment charges in Commercial

Banking were driven by a deterioration in credit

quality in the second half of the year.

For the Group as a whole, the aggregate

outstanding customer loan impairment allowances

at 31 December 2008 of US$23.9 billion represented

2.6 per cent of gross customer advances (net of

reverse repos and settlement accounts), compared

with 2 per cent at 31 December 2007.