HSBC 2009 Annual Report Download - page 288

Download and view the complete annual report

Please find page 288 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

Capital management and allocation > Capital measurement and allocation

286

financial system during the past two years have been

used to inform the capital planning process and

further develop the stress scenarios employed by the

Group.

The responsibility for global capital allocation

principles and decisions rests with GMB. Through

its structured internal governance processes, HSBC

maintains discipline over its investment and capital

allocation decisions and seeking to ensure that

returns on investment are adequate after taking

account of capital costs. HSBC’s strategy is to

allocate capital to businesses on the basis of their

economic profit generation, regulatory and economic

capital requirements and cost of capital.

HSBC’s capital management process is

articulated in an annual Group capital plan which is

approved by the Board. The plan is drawn up with

the objective of maintaining both the appropriate

amount of capital and the optimal mix between the

different components of capital. When HSBC

Holdings and its major subsidiaries raise non-equity

tier 1 capital and subordinated debt, this is done in

accordance with the Group’s guidelines on market

and investor concentration, cost, market conditions,

timing, effect on composition and maturity profile.

Each subsidiary manages its own capital to support

its planned business growth and meet its local

regulatory requirements within the context of the

approved annual Group capital plan. In accordance

with HSBC’s Capital Management Framework,

capital generated by subsidiaries in excess of

planned requirements is returned to HSBC Holdings,

normally by way of dividends.

HSBC Holdings is primarily the provider of

equity capital to its subsidiaries and these

investments are substantially funded by HSBC

Holdings’ own capital issuance and profit retention.

As part of its capital management process, HSBC

Holdings seeks to maintain a prudent balance

between the composition of its capital and that of its

investment in subsidiaries.

During 2009, the Group targeted a tier 1 ratio

within the range 7.5 to 10.0 per cent for the purposes

of its long-term capital planning. This was an

increase on the 2008 range of 7.5 to 9.0 per cent, and

reflected revised market expectations on capital

strength and the higher volatility of capital

requirements which resulted from pro-cyclicality

embedded within the Basel II rules. The tier 1 ratio

increased to 10.8 per cent at 31 December 2009

(2008: 8.3 per cent) and notwithstanding that this

lies outside the target range noted above, HSBC is

satisfied that, in light of the current evolution of the

regulatory framework, this is appropriate.

Capital measurement and allocation

The FSA supervises HSBC on a consolidated basis

and therefore receives information on the capital

adequacy of, and sets capital requirements for, the

Group as a whole. Individual banking subsidiaries

are directly regulated by their local banking

supervisors, who set and monitor their capital

adequacy requirements.

HSBC calculates capital at a Group level using

the Basel II framework of the Basel Committee on

Banking Supervision; local regulators are at different

stages of implementation and local rules may still

be on a Basel I basis, notably in the US. In most

jurisdictions, non-banking financial subsidiaries

are also subject to the supervision and capital

requirements of local regulatory authorities.

Basel II is structured around three ‘pillars’:

minimum capital requirements, supervisory review

process and market discipline. The Capital

Requirements Directive (‘CRD’) implemented

Basel II in the EU and the FSA then gave effect

to the CRD by including the requirements of the

CRD in its own rulebooks.

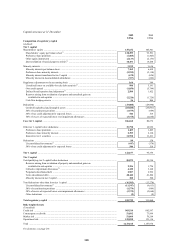

Capital

HSBC’s capital is divided into two tiers:

• tier 1 capital is divided into core tier 1 and other

tier 1 capital. Core tier 1 capital comprises

shareholders’ equity and related minority

interests. The book values of goodwill and

intangible assets are deducted from core tier 1

capital and other regulatory adjustments are

made for items reflected in shareholders’ equity

which are treated differently for the purposes of

capital adequacy. Qualifying hybrid capital

instruments such as non-cumulative perpetual

preference shares and innovative tier 1 securities

are included in other tier 1 capital;

• tier 2 capital comprises qualifying subordinated

loan capital, related minority interests, allowable

collective impairment allowances and unrealised

gains arising on the fair valuation of equity

instruments held as available-for-sale. Tier 2

capital also includes reserves arising from the

revaluation of properties.

To ensure the overall quality of the capital base,

the FSA’s rules set limits on the amount of hybrid

capital instruments that can be included in tier 1

capital relative to core tier 1 capital, and also limits

overall tier 2 capital to no more than tier 1 capital.

The basis of consolidation for financial

accounting purposes is described on page 367 and