HSBC 2009 Annual Report Download - page 267

Download and view the complete annual report

Please find page 267 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

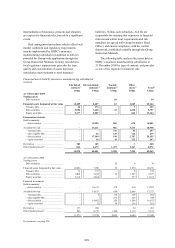

265

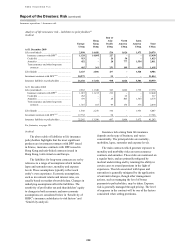

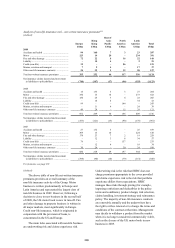

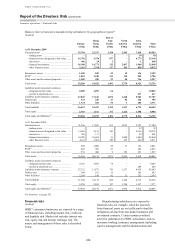

Risk management of insurance

operations

(Audited)

HSBC operates a bancassurance model which

provides insurance products for customers with

whom the Group has a banking relationship.

Insurance products are sold to all customer groups,

mainly utilising retail branches, the internet and

phone centres. Personal Financial Services

customers attract the majority of sales and comprise

the majority of policyholders.

HSBC offers its customers a wide range of

insurance and investment products, many of

which complement other bank and

consumer finance products.

Many of these insurance products are

manufactured by HSBC subsidiaries. The Group

underwrites the insurance risk and retains the risks

and rewards associated with writing insurance

contracts, retaining both the underwriting profit and

the commission paid by the manufacturer to the bank

distribution channel within the Group. When the

Group chooses to manage its exposure to insurance

risk through the use of third-party reinsurers, the

associated revenue and manufacturing profit is ceded

to them. HSBC’s exposure to risks associated with

manufacturing insurance contracts in its subsidiaries

and its management of these risks are discussed

below.

Where the Group considers it operationally

more effective, third parties are engaged to

manufacture insurance products for sale through

HSBC’s banking network. The Group works with a

limited number of market-leading partners to provide

the products. These arrangements earn HSBC a

commission.

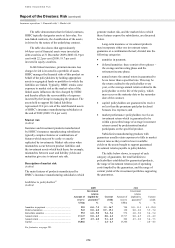

HSBC’s bancassurance business operates in

all six of the Group’s geographical regions with

over 30 legal entities, the majority of which are

subsidiaries of banking legal entities, manufacturing

insurance products. Management of these insurance

manufacturers set their own control procedures in

addition to complying with guidelines issued by the

Group Insurance Head Office. This is headed by

HSBC’s Managing Director of Insurance, supported

by a Chief Operating Officer, Chief Financial

Officer and Chief Risk Officer. The role of Group

Insurance Head Office includes forming and

communicating the strategy for insurance, setting the

control framework for monitoring and measuring

insurance risk in line with Group practices, and

drawing up insurance-specific policies and

guidelines for inclusion in the Group Instruction

Manuals. The control framework for monitoring risk

includes the Group Insurance Risk Committee,

which oversees the status of the significant risk

categories in the insurance operations. Five sub-

committees report to the Committee, focusing on

products and pricing, market and liquidity risk,

credit risk, operational and insurance risk.

All insurance products, whether manufactured

internally or by a third party, are subjected to a

detailed product approval process. Approval is

provided by the Regional Insurance Head Office or

Group Insurance Head Office depending on the type

of product and its risk profile. The process consists

of an analysis of the inherent risks of a product,

including but not limited to market risk, credit risk,

insurance and pricing risk and regulatory risk.

Certain products, for example those of a particularly

complex nature or those providing a guarantee, are

reviewed by the Product and Pricing Committee as

part of the approval process. The committee

comprises the heads of the relevant risk functions

within insurance and sits at both regional and Group

Insurance levels.

The processes and controls employed to monitor

each risk are described under their respective

headings below.

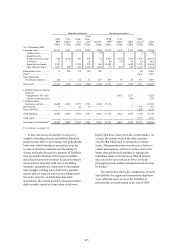

The main contracts manufactured by HSBC are

as follows:

Life insurance business

(Audited)

• Life insurance contracts with discretionary

participation features (‘DPF’) allow

policyholders to participate in the profits

generated from such business, which may take

the form of annual bonuses and a final bonus, in

addition to providing cover on death. Certain

minimum return levels are also guaranteed. The

largest portfolio is in Hong Kong.

• Credit life insurance business is written to

underpin banking and finance products. The

policy pays a claim if the holder of the loan is

unable to make repayments due to early death

or unemployment.

• Annuities are contracts providing regular

payments of income from capital investment for

either a fixed period or during the annuitant’s

lifetime. Payments to the annuitant either begin

on inception of the policy (immediate annuities)

or at a designated future date (deferred

annuities).