HSBC 2009 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

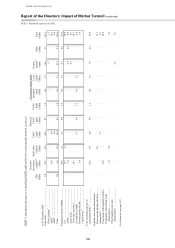

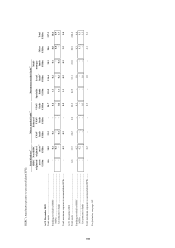

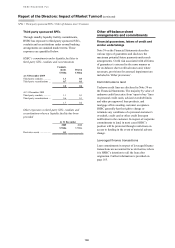

Report of the Directors: Risk (continued)

Credit risk > Management

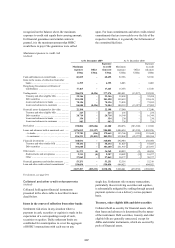

202

manuals their detailed credit policies and

procedures, consistent with Group policy;

• guiding HSBC’s operating companies on the

Group’s appetite for credit risk exposure to

specified market sectors, activities and banking

products. GMO Risk controls exposures to

certain higher-risk sectors and closely monitors

exposure to others, including real estate, the

automotive sector, certain non-bank financial

institutions, structured products and leveraged

finance transactions. When necessary,

restrictions are imposed on new business or

exposures, which may be capped at Group

and/or entity level;

• undertaking independent review and objective

assessment of risk. GMO Risk assesses all

commercial non-bank credit facilities and

exposures – including those embedded in

derivatives – that are originated or renewed by

HSBC’s operating companies over designated

limits, prior to the facilities being committed to

customers or transactions being undertaken.

Operating companies may not confirm credit

approval without this concurrence;

• monitoring the performance and management of

portfolios across the Group. GMO Risk tracks

emerging trends and conducts in-depth portfolio

reviews, overseeing the effective management

of any adverse characteristics;

• controlling centrally exposures to sovereign

entities, banks and other financial institutions.

HSBC’s credit and settlement risk limits to

counterparties in these sectors are approved and

managed by GMO Risk to optimise the use of

credit availability and avoid excessive risk

concentration;

• controlling exposure for all debt securities held;

where a security is not held solely for the

purpose of trading, a formal issuer risk limit is

established;

• establishing and maintaining HSBC’s policy

on large credit exposures, ensuring that

concentrations of exposure by counterparty,

sector or geography do not become excessive in

relation to the Group’s capital base and remain

within internal and regulatory limits. GMO Risk

also monitors HSBC’s intra-Group exposures to

ensure they are maintained within regulatory

limits and ensures that policy and practice are

fully aligned to evolving regulatory

requirements;

• controlling cross-border exposures, through the

imposition of country limits with sub-limits by

maturity and type of business. Country limits

are determined by taking into account economic

and political factors, and applying local business

knowledge. Transactions with countries deemed

to be higher risk are considered on a case by

case basis;

• maintaining and developing HSBC’s risk rating

framework and systems, to classify exposures

meaningfully and enable focused management

of the risks involved. The GCRO chairs the

Credit Risk Analytics Oversight Committee,

which reports to the RMM and oversees risk

rating model governance for both wholesale and

retail business. Rating methodologies, based

upon a wide range of analytics and market data-

based tools, are core inputs to the assessment of

customer risk. For larger facilities, while full use

is made of automated risk-rating processes, the

ultimate responsibility for setting risk ratings

rests with the final approving executive;

• assisting the Risk Strategy unit in the

development of stress-testing scenarios,

economic capital measurement and the

refinement of key risk indicators and their

reporting, embedded within the Group’s

business planning processes;

• reporting on aspects of the HSBC credit risk

portfolio to the RMM, the Group Audit

Committee and the Board of Directors of HSBC

Holdings by way of a variety of regular and ad

hoc reports covering:

– risk concentrations;

– retail portfolio performance at Group entity,

regional and overall Group levels;

– specific higher-risk portfolio segments;

– a risk map of the status of key risk topics,

with associated preventive and mitigating

actions;

– individual large impaired accounts, and

impairment allowances/charges for all

customer segments;

– country limits, cross-border exposures and

related impairment allowances;

– portfolio and analytical model performance

data; and

– stress-testing results and recommendations;

• managing and directing credit risk management

systems initiatives. A centralised database

covers substantially all the Group’s direct

lending exposures, to deliver an increasingly