HSBC 2009 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

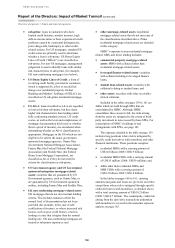

Report of the Directors: Impact of Market Turmoil (continued)

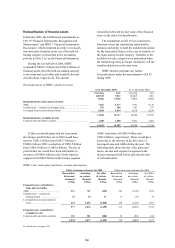

Overview of exposure > Nature and extent of exposures

158

• sub-prime: loans to customers who have

limited credit histories, modest incomes, high

debt-to-income ratios or have experienced credit

problems caused by occasional delinquencies,

prior charge-offs, bankruptcy or other credit-

related actions. For US mortgages, standard US

credit scores are primarily used to determine

whether a loan is sub-prime. US Home Equity

Lines of Credit (‘HELoC’s) are classified as

sub-prime. For non-US mortgages, management

judgement is used to identify loans with similar

risk characteristics to sub-prime, for example,

UK non-conforming mortgages (see below);

• US Home Equity Lines of Credit: a form of

revolving credit facility provided to customers,

which is supported by a first or second lien

charge over residential property. Global

Banking and Markets’ holdings of HELoCs are

classified as US sub-prime residential mortgage

assets;

• US Alt-A: loans classified as Alt-A are regarded

as lower risk than sub-prime, but they share

higher risk characteristics than lending under

fully conforming standard criteria. US credit

scores, as well as the level and completeness of

mortgage documentation held (such as whether

there is proof of income), are considered when

determining whether an Alt-A classification is

appropriate. Mortgages in the US which are not

eligible to be sold to the major government

sponsored mortgage agencies, Ginnie Mae

(Government National Mortgage Association),

Fannie Mae (the Federal National Mortgage

Association) and Freddie Mac (the Federal

Home Loan Mortgage Corporation), are

classified as Alt-A if they do not meet the

criteria for classification as sub-prime;

• US Government agency and US Government

sponsored enterprises mortgage-related

assets: securities that are guaranteed by US

Government agencies, such as Ginnie Mae, or

are guaranteed by US Government sponsored

entities, including Fannie Mae and Freddie Mac;

• UK non-conforming mortgage-related assets:

UK mortgages that do not meet normal lending

criteria. This includes instances where the

normal level of documentation has not been

provided (for example, in the case of self-

certification of income), or where increased risk

factors, such as poor credit history, result in

lending at a rate that is higher than the normal

lending rate. UK non-conforming mortgages are

treated as sub-prime exposures; and

• other mortgage-related assets: residential

mortgage-related assets that do not meet any of

the classifications described above. Prime

residential mortgage-related assets are included

in this category.

HSBC’s exposure to non-residential mortgage-

related ABSs and direct lending includes:

• commercial property mortgage-related

assets: MBSs with collateral other than

residential mortgage-related assets;

• leveraged finance-related assets: securities

with collateral relating to leveraged finance

loans;

• student loan-related assets: securities with

collateral relating to student loans; and

• other assets: securities with other receivable-

related collateral.

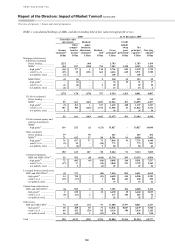

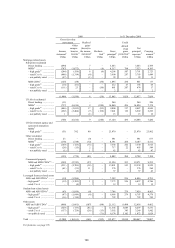

Included in the tables on pages 159 to 161 are

ABSs which are held through SPEs that are

consolidated by HSBC. Although HSBC

consolidates these assets in full, the risks arising

from the assets are mitigated to the extent of third-

party investment in notes issued by those SPEs. For

a description of HSBC’s holdings of and

arrangements with SPEs, see page 181.

The exposure detailed in the table on page 159

includes long positions where risk is mitigated by

specific credit derivatives with monolines and other

financial institutions. These positions comprise:

• residential MBSs with a carrying amount of

US$1.0 billion (2008: US$0.9 billion);

• residential MBS CDOs with a carrying amount

of US$15 million (2008: US$39 million); and

• ABSs other than residential MBSs and

MBS CDOs with a carrying amount of

US$9.2 billion (2008: US$9.8 billion).

In the tables on pages 160 to 161, carrying

amounts and gains and losses are given for securities

except those where risk is mitigated through specific

credit derivatives with monolines, as detailed above,

with a total carrying amount of US$10.2 billion

(2008: US$10.7 billion). The counterparty credit risk

arising from the derivative transactions undertaken

with monolines is covered in the monoline exposure

analysis on page 163.