HSBC 2009 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

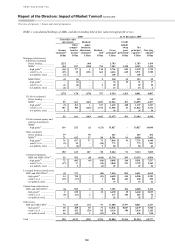

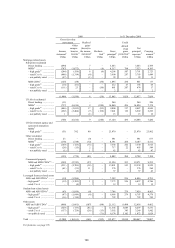

Report of the Directors: Impact of Market Turmoil (continued)

Fair values of financial instruments > Carried at fair value

166

US$3.6 billion) and US$1.9 billion to

communications and infrastructure (2008:

US$1.7 billion). During the year, 99 per cent

of the total fair value movement not recognised was

against exposures in these two sectors (2008: 99 per

cent). Subsequent to the end of the year, as part of

portfolio management, US$0.6 billion of the data

processing exposure was sold.

Fair values of financial instruments

(Audited)

The classification of financial instruments is

determined in accordance with the accounting

policies set out in Note 2 on the Financial

Statements. The use of assumptions and estimation

in valuing financial instruments is described on

page 63. The following is a description of HSBC’s

methods of determining fair value and its related

control framework, and a quantification of its

exposure to financial instruments measured at fair

value.

Fair value is the amount for which an asset

could be exchanged, or a liability settled, between

knowledgeable, willing parties in an arm’s length

transaction.

Financial instruments measured at fair value

on an ongoing basis include trading assets and

liabilities, instruments designated at fair value,

derivatives and financial investments classified

as available for sale (including treasury and other

eligible bills, debt securities, and equity securities).

Fair values of financial instruments carried

at fair value

Control framework

Fair values are subject to a control framework

designed to ensure that they are either determined

or validated by a function independent of the

risk-taker. To this end, ultimate responsibility for

the determination of fair values lies with Finance,

which reports functionally to the Chief Financial

Officer, Executive Director, Risk and Regulation.

Finance establishes the accounting policies and

procedures governing valuation and is responsible

for ensuring that they comply with all relevant

accounting standards.

For all financial instruments where fair values

are determined by reference to externally quoted

prices or observable pricing inputs to models,

independent price determination or validation is

utilised. In inactive markets, direct observation

of a traded price may not be possible. In these

circumstances, HSBC will source alternative market

information to validate the financial instrument’s fair

value, with greater weight given to information that

is considered to be more relevant and reliable. The

factors that are considered in this regard are, inter

alia:

• the extent to which prices may be expected to

represent genuine traded or tradeable prices;

• the degree of similarity between financial

instruments;

• the degree of consistency between different

sources;

• the process followed by the pricing provider to

derive the data;

• the elapsed time between the date to which the

market data relates and the balance sheet date;

and

• the manner in which the data was sourced.

Models provide a logical framework for the

capture and processing of necessary valuation inputs.

For fair values determined using a valuation model,

the control framework may include, as applicable,

independent development or validation of (i) the

logic within valuation models; (ii) the inputs to those

models; (iii) any adjustments required outside the

valuation models; and (iv) where possible, model

outputs. Valuation models are subject to a process

of due diligence and calibration before becoming

operational and are calibrated against external

market data on an ongoing basis.

The results of the independent validation

process are reported to, and considered by, Valuation

Committees. Valuation Committees are composed of

valuation experts from several independent support

functions (Product Control, Market Risk

Management, Quantitative Risk and Valuation

Group and Finance) in addition to senior

management. The members of each Valuation

Committee consider the appropriateness and

adequacy of the fair value adjustments and the

effectiveness of valuation models. If necessary,

they may require changes to model calibration or

calibration procedures. The Valuation Committees

are overseen by the Valuation Committee Review

Group, which consists of Heads of Global Banking

and Markets’ Finance and Risk Functions. All

subjective valuation items with a potential impact in

excess of US$5 million are reported to the Valuation

Committee Review Group.