HSBC 2009 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

215

Dubai and the UAE

In November 2009, Dubai World, a Dubai

government-owned firm, requested a creditor

standstill on its debt repayments and those of some

of its subsidiaries. The announcement prompted

a significant sell-off in markets across the world.

Abu Dhabi announced that it would offer additional

assistance to Dubai, providing liquidity and a

platform for the debt restructuring process to

continue.

HSBC, as the longest-established bank in the

region, has a longstanding relationship with the

government of Dubai and its related entities. HSBC

has contributed from the earliest days to the

development of Dubai as an emerging economy and

continues to maintain supportive relationships with

all parts of the UAE. HSBC will continue to offer its

support to the government of Dubai in achieving a

workable resolution of its current liquidity problems.

HSBC’s exposure within Dubai is acceptably

spread and is primarily to operating companies

within the emirate. HSBC is playing a prominent

role in restructuring indebtedness in order to help

restore confidence in the region.

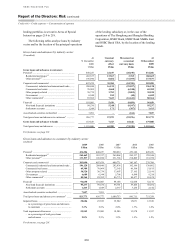

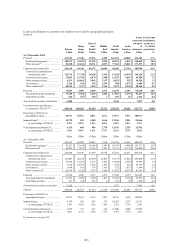

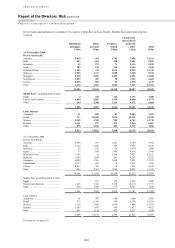

In the UAE, gross customer loans and advances

fell from US$18 billion at 31 December 2008 to

US$15 billion at 31 December 2009. Although the

Middle East represents 2 per cent of the Group’s

balance sheet, it remains a region to which HSBC

is strongly committed.

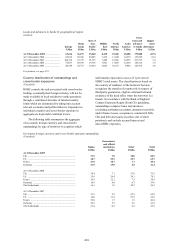

Sovereign counterparties

The overall quality of the Group’s sovereign risk

exposure remained satisfactory during 2009, with the

large majority of both in-country and cross-border

limits extended to countries with strong internal

credit risk ratings. There was no significant

downward shift in the quality of the exposure

although, given the higher debt and weaker fiscal

positions of many Western governments, there is

increased potential for deterioration in sovereign risk

profiles before budgetary re-balancing is achieved.

In order to manage this, the Group regularly updates

its assessments of higher-risk countries and adjusts

its risk appetite to reflect such changes.

Leveraged financing

The Group operates a controlled approach towards

leveraged finance origination with caps on

underwriting and final hold levels in place. This puts

a premium on successfully distributing risk in order

to create capacity under the caps. Group exposure to

leveraged finance transactions remained modest in

relation to overall exposure.

Personal lending

(Unaudited)

HSBC provides a broad range of secured and

unsecured personal lending products to meet

customer needs. Given the diverse nature of the

markets in which HSBC operates, the range is not

standardised across all countries but is tailored to

meet the demands of individual markets while using

appropriate distribution channels and, wherever

possible, standard global IT platforms.

Personal lending includes advances to customers

for asset purchase, such as residential property and

motor vehicles, where the loans are typically secured

on the assets being acquired. HSBC also offers loans

secured on existing assets, such as first and second

liens on residential property; unsecured lending

products such as overdrafts, credit cards and payroll

loans; and debt consolidation loans which may be

secured or unsecured.

In 2009, credit exposure in the personal lending

portfolios continued to be affected by adverse global

economic conditions, particularly increased

unemployment levels and the restricted availability

of refinancing which limited the ability of many

customers to service financial obligations in line

with contractual commitments. This led to

delinquency levels and loan impairment charges

remaining high, although management action in

recent years to run off the US consumer finance exit

portfolios and curtail originator activity helped

reduce the overall impairment charge.

The commentary that follows is on an

underlying basis.

At 31 December 2009, total personal lending

was US$434 billion, a decline of 6 per cent from

31 December 2008, driven by run-off in the US

consumer finance exit portfolios. Within Personal

Financial Services total loan impairment charges and

other credit risk provisions of US$19.9 billion were

3 per cent lower than in 2008 and were concentrated

in North America (US$14.4 billion) and, to a lesser

extent, Europe (US$2.0 billion) and Latin America

(US$2.0 billion).

In early March 2009, HSBC Finance announced

the discontinuation of new customer account

originations for all products offered by its Consumer

Lending business and closed approximately 800

Consumer Lending branch offices. In November

2009, it entered into an agreement to sell its vehicle

loan servicing operations to Santander Consumer

USA Inc. (‘SC USA’) as well as an aggregate

US$1.0 billion of vehicle finance loans, both

delinquent and non-delinquent. Under a separate

agreement, SC USA will service the remainder of