HSBC 2009 Annual Report Download - page 224

Download and view the complete annual report

Please find page 224 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

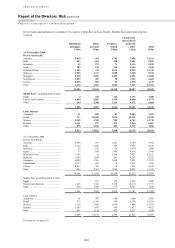

Report of the Directors: Risk (continued)

Credit risk > Areas of special interest > US personal lending – credit quality

222

Mortgage lending

In line with its exit strategy for non-prime real estate

secured mortgage lending, HSBC continued to

reduce mortgage lending exposure in the US and

balances declined from US$96 billion to

US$78 billion as the portfolios ran off.

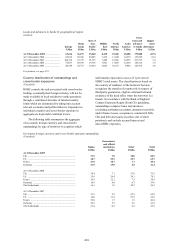

Although delinquency increased during 2009,

credit quality deteriorated at a slower rate than in

previous years as the effect of higher unemployment

was not as severe as expected due to actions

previously taken by HSBC to reduce risk in the

loan portfolio.

Following the revision of the write-off period

described on page 205, two months and over

delinquent balances in the real estate secured

portfolios of HSBC Finance decreased in dollar

terms but, excluding the effects of the change, they

rose. Delinquent balances also increased in HSBC

Bank USA. Increased delinquency reflected portfolio

seasoning in an environment of continuing weakness

in the housing market and diminished availability of

refinancing opportunities. In addition, delays to

foreclosure caused by changes in some state

government practices and backlogs in court

proceedings resulted in balances that would

otherwise have proceeded to foreclosure remaining

reported as contractually delinquent.

Excluding the effects of revising the write-off

period:

• delinquency in the Consumer Lending business

increased, primarily in the 2006, 2007 and 2008

vintages of the first lien real estate secured

portfolio. Two months or more delinquent

balances rose from US$5.6 billion in 2008 to

US$7.4 billion at 31 December 2009, and two

months or more delinquency rates grew from

12.1 per cent to 18.2 per cent;

• two months or more delinquent balances in the

Mortgage Services portfolio declined from

US$4.7 billion in 2008 to US$4.5 billion at

31 December 2009 as the portfolio continued to

season, and two months or more delinquency

rates increased from 17 per cent in 2008 to

19.6 per cent at 31 December 2009 as balances

declined at a faster pace than delinquencies.

At HSBC Bank USA, the level of dollar

delinquency increased within the first lien prime

residential mortgage and Home Equity mortgage

loan portfolios, reflecting the weakened US

economy, high unemployment and continued

deterioration of the US housing market. Delinquency

rates also rose, in part due to lower balances as

mortgage portfolios were sold to third parties. In

2009, HSBC Bank USA sold US$4.5 billion of

mortgage portfolios to third parties and it continued

to sell the majority of new mortgage loan

originations to government-sponsored enterprises

and private investors. Two months or more

delinquencies increased from 3.4 per cent to 7.5 per

cent at 31 December 2009, as delinquency balances

increased from US$0.7 billion to US$1.2 billion,

while balances declined.

In HSBC Finance, loss rates on the sale of

foreclosed properties were broadly stable throughout

2009 but were higher than those incurred in 2008

as house prices continued to fall. The number of

properties foreclosed decreased, in part due to delays

in foreclosure proceedings and the lengthening by

certain states of the foreclosure process. HSBC

continued to assist customers in restructuring their

debts to avoid foreclosure, including by modifying

their loans when it was decided that they could be

serviced on revised terms. For further details, see

‘HSBC Finance loan modifications and re-ageing’

on page 224.

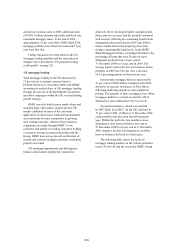

Second lien mortgage loans have a risk profile

characterised by higher loan-to-value ratios because,

in the majority of cases, the loans were taken out to

complete the refinancing or purchase of properties.

HSBC Finance has typically experienced loss on

default for second lien loans approaching 100 per

cent of the amount owing, as any equity in the

property is initially applied to the first lien loan.

Excluding the effects of the change to the write-off

period, in the HSBC Finance Mortgage Services

second lien portfolio, two months or more

delinquency rates decreased to 17.3 per cent at

31 December 2009 as the portfolio continued to run

off. In the Consumer Lending second lien portfolio,

two months or more delinquency rates increased to

18.6 per cent at 31 December 2009. In HSBC Bank

USA, second lien two months or more delinquency

rates increased from 3.5 per cent at 31 December

2008 to 4 per cent at 31 December 2009.

Stated-income mortgage balances in HSBC

Finance declined from US$5.7 billion to

US$3.9 billion as the portfolio continued to run off.

The decline included US$0.2 million as a result of

the revised write-off period referred to on page 205.

These mortgages were underwritten on the basis of

borrowers’ representations of annual income and

were not verified by supporting documents and, as a

result, represent a higher than average level of risk.

Two months or more delinquency rates decreased to

22.7 per cent at 31 December 2009. In HSBC Bank

USA, stated-income balances decreased from

US$2.2 billion to US$2.1 billion and delinquency