HSBC 2009 Annual Report Download - page 268

Download and view the complete annual report

Please find page 268 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

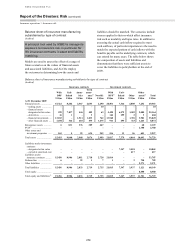

Report of the Directors: Risk (continued)

Insurance operations > Non-life business / Insurance risk

266

• Term assurance and critical illness policies

provide cover in the event of death (term

assurance) and serious illness.

• Linked life insurance contracts pay benefits to

policyholders which are typically determined

by reference to the value of the investments

supporting the policies.

• Investment contracts with DPF allow

policyholders to participate in the profits

generated by such business. The largest

portfolio is written in France. Policyholders

are guaranteed to receive a return on their

investment plus any discretionary bonuses.

In addition, certain minimum return levels are

guaranteed.

• Unit-linked investment contracts are those

where the principal benefit payable is the value

of assigned assets. Any benefits payable to

policyholders related to insurance risk are not

significant on these contracts.

• Other investment contracts include pension

contracts written in Hong Kong.

Non-life insurance business

(Audited)

Non-life insurance contracts include motor, fire and

other damage to property, accident and health,

repayment protection and commercial insurances.

Motor insurance business covers vehicle

damage and liability for personal injury. For fire and

other damage to property, the main focus in most

markets is providing individuals with home and

contents insurance. Cover is also provided for

selected commercial customers, largely written in

Asia and Latin America.

A very limited portfolio of liability business is

written, other than that included in the motor book.

Credit non-life insurance is concentrated in

North America, and is originated in conjunction with

the provision of loans. Following a decision taken to

close the Consumer Lending business in the US,

insurance products written in conjunction with this

business will now be run off. In December 2007, the

group decided to cease selling payment protection

insurance (‘PPI’) products in the UK and a phased

withdrawal was completed across the HSBC, first

direct and M&S Money brands during 2008. HFC

ceased selling single premium PPI in 2008 and sales

of regular PPI will reduce as HFC exits its remaining

retail relationships. HSBC continues to distribute its

UK short-term income protection (‘STIP’) product.

In January 2009, the Competition Commission

(‘CC’) published its report into the PPI market in

which it stipulated that STIP products will also be

subject to their remedies when sold in conjunction

with or as a result of a referral following the sale of a

loan or similar credit product. HSBC has undertaken

an analysis of the required changes to the STIP

product and its sales processes resulting from the

CC’s remedies. Following an appeal to the

Competition Appeal Tribunal, the CC continues to

consult on whether a ban on firms selling PPI at the

point of sale of the credit product is an appropriate

and justified remedy for the deficiencies it identified

in the PPI market.

Given the nature of the contracts written by the

Group, the risks to which HSBC’s insurance

operations are exposed fall into two principal

categories: insurance risk and financial risk. The

following section describes the nature and extent of

these risks and HSBC’s approach to managing them.

The majority of the risk in the insurance business

derives from manufacturing activities, and

consequently the following sections focus on how

the Group manages risk arising in the manufacturing

subsidiaries.

Insurance risk

(Audited)

Insurance risk is a risk, other than financial risk,

transferred from the holder of a contract to the

issuer, in this case HSBC.

The principal insurance risk faced by HSBC

is that, over time, the combined cost of

claims, benefits, administration and

acquisition of the contract may exceed the

aggregate amount of premiums received

and investment income.

The cost of claims and benefits can be

influenced by many factors, including mortality and

morbidity experience, lapse and surrender rates and,

if the policy has a savings element, the performance

of the assets held to support the liabilities.

Performance of the underlying assets is affected by

changes in both interest rates and equity prices (see

page 274).

During 2009, Group Insurance agreed to a

global risk appetite statement in relation to insurance

risks, encompassing limits on the largest exposures

the business will write in normal circumstances. In

addition to the global statement, local businesses

continue to propose their own risk appetites that are

authorised centrally.

Life and non-life business insurance risks are

controlled by high-level policies and procedures set

centrally, supplemented as appropriate with