HSBC 2009 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

179

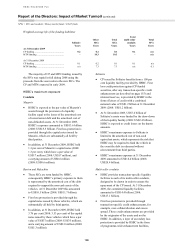

For impairment losses on available-for-sale

equity and debt securities, see pages 31 and 35,

respectively. Any impairment losses relating to

ABSs recognised in the income statement are

recorded as ‘Loan impairment charges and other

credit risk provisions’. Impairment losses incurred

on assets held by consolidated securities investment

conduits (excluding Solitaire) are offset by a credit

to the impairment line for the amount of the loss

borne by capital note holders.

Fair values of financial instruments not

carried at fair value

Financial instruments that are not carried at fair

value on the balance sheet include loans and

advances to banks and customers, deposits by banks,

customer accounts, debt securities in issue and

subordinated liabilities. Their fair values are,

however, provided for information by way of note

disclosure and are calculated as described below.

The calculation of fair value incorporates

HSBC’s estimate of the amount at which financial

assets could be exchanged, or financial liabilities

settled, between knowledgeable, willing parties in an

arm’s length transaction. It does not reflect the

economic benefits and costs that HSBC expects to

flow from the instruments’ cash flows over their

expected future lives. Other reporting entities

may use different valuation methodologies and

assumptions in determining fair values for which

no observable market prices are available, so

comparisons of fair values between entities may

not be meaningful and users are advised to exercise

caution when using this data.

As a consequence of the market turmoil there

has been a significant reduction in the secondary

market demand for US consumer lending assets.

Uncertainty over the extent and timing of future

credit losses, together with a near absence of

liquidity for non-prime ABSs and loans, continued

to be reflected in a low volume of bid prices at

31 December 2009. It is not possible from the

indicative market prices that are available to

distinguish between the relative discount to nominal

value within the fair value measurement that reflects

cash flow impairment due to expected losses to

maturity, and the discount that the market is

demanding for holding an illiquid asset. Under

impairment accounting for loans and advances, there

is no requirement to adjust the carrying value to

reflect illiquidity as HSBC’s intention is to fund

assets until the earlier of prepayment, charge-off or

repayment on maturity. The fair value, by contrast,

reflects both incurred loss and loss expected through

the life of the asset, a discount for illiquidity and a

credit spread which reflects the market’s current risk

preferences. This usually differs from the credit

spread applicable in the market at the time the loan

was underwritten and funded.

The estimated fair values at 31 December 2009

and 31 December 2008 of loans and advances to

customers in North America reflected the combined

effect of these conditions. As a result, the fair values

are substantially lower than the carrying amount of

customer loans held on-balance sheet and lower than

would otherwise be reported under more normal

market conditions. Accordingly, the fair values

reported do not reflect HSBC’s estimate of the

underlying long-term value of the assets. Fair values

at the balance sheet date of the assets and liabilities

set out below are estimated for the purpose of

disclosure as follows:

• Loans and advances to banks and customers

The fair value of loans and advances is based

on observable market transactions, where

available. In the absence of observable market

transactions, fair value is estimated using

discounted cash flow models. Performing

loans are grouped, as far as possible, into

homogeneous pools segregated by maturity and

coupon rates. In general, contractual cash flows

are discounted using HSBC’s estimate of the

discount rate that a market participant would use

in valuing instruments with similar maturity,

re-pricing and credit risk characteristics.

The fair value of a loan portfolio reflects

both loan impairments at the balance sheet

date and estimates of market participants’

expectations of credit losses over the life of

the loans. For impaired loans, fair value is

estimated by discounting the future cash flows

over the time period they are expected to be

recovered.

• Financial investments

The fair values of listed financial investments

are determined using bid market prices. The fair

values of unlisted financial investments are

determined using valuation techniques that take

into consideration the prices and future earnings

streams of equivalent quoted securities.

• Deposits by banks and customer accounts

For the purpose of estimating fair value,

deposits by banks and customer accounts are

grouped by remaining contractual maturity. Fair

values are estimated using discounted cash

flows, applying current rates offered for deposits