HSBC 2009 Annual Report Download - page 241

Download and view the complete annual report

Please find page 241 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

239

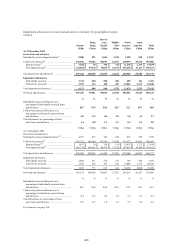

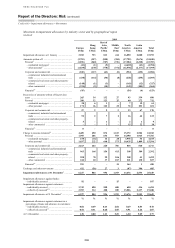

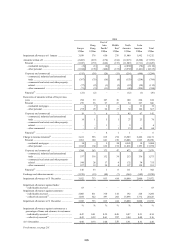

in unemployment and bankruptcy filings. Impaired

loans were broadly stable at US$846 million.

In Rest of Asia-Pacific, new loan impairment

allowances rose by 18 per cent to US$1.1 billion,

mainly due to increased delinquencies on unsecured

lending, particularly in the credit card and personal

lending portfolios in India and, to a lesser extent,

in Indonesia. In the corporate and commercial

portfolios, new loan impairment allowances

increased, reflecting a deterioration in India’s

economic conditions. Impaired loans increased

by 44 per cent to US$1.2 billion.

Releases and recoveries in the Rest of

Asia-Pacific region rose by 42 per cent to

US$214 million at 31 December 2009.

New loan impairment allowances in the Middle

East increased significantly from a low base, to

US$1.4 billion. The increase reflected higher charges

in the UAE, largely in Dubai, due to a marked

deterioration in credit quality which particularly

affected the real estate and construction industries.

Infrastructure projects were delayed or cancelled and

unemployment levels increased. Delinquency rates

rose as a result, particularly in the credit card and

personal loan portfolios. Impaired loans increased by

US$1.4 billion to US$1.7 billion.

New loan impairment allowances rose by

7 per cent to US$26.4 billion despite falls of

12 per cent in Hong Kong and 7 per cent in

North America.

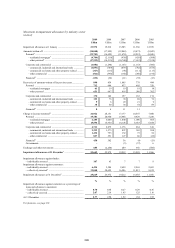

In North America, new loan impairment

allowances declined by 7 per cent to US$15.6 billion

against the backdrop of a widespread rise in

unemployment, continued weakness in the US

economy and housing markets, higher levels of

personal bankruptcy filings and portfolio seasoning.

This decline was the result of lower loan impairment

charges in the Mortgage Services real estate secured,

credit card and vehicle finance portfolios, partially

offset by higher loan impairment charges in the

branch-based Consumer Lending business. Apart

from the changes made to the write-off period, the

main contributing factors were as follows:

• new loan impairment allowances in the

Mortgage Services business decreased in 2009

as the portfolio continued to run off. While loss

severities increased compared with 2008, a

higher percentage of impairment was in respect

of first lien loans which have less severity than

second lien loans;

• new loan impairment allowances in the vehicle

finance loan portfolio decreased as a result of

lower loan levels reflecting the discontinuance

of vehicle finance originations in July 2008. In

addition, loss severities decreased as prices on

repossessed vehicles improved; and

• new loan impairment allowances in the branch-

based Consumer Lending business increased in

2009, primarily in the unsecured portfolio due to

the deterioration in the 2006 and 2007 vintages

which were more pronounced in certain

geographic regions and, to a lesser extent, first

lien real estate secured loans. These increases

were partially offset by lower new loan

impairment allowances for second lien real

estate secured loans.

New loan impairment allowances in the Cards

and Retail Services portfolios declined due to lower

outstanding balances and management action taken

in the past two years to constrain origination

activities in riskier segments. In addition,

impairment provisioning reflects an improved

outlook on future loss estimates as the impact of

higher unemployment rates on losses has not been as

severe as initially expected due, in part, to lower fuel

prices and the boost to cash flow provided by

government stimulus programmes that meaningfully

benefit non-prime customers. In HSBC Bank USA

personal lending portfolios, new loan impairment

allowances increased, mainly in prime residential

mortgage lending.

New loan impairment allowances in the

corporate and commercial lending portfolios

increased as the weaker economy affected firms in

the commercial real estate and construction sectors

in the US. In Canada, higher new loan impairment

allowances were primarily against exposures in the

commercial real estate, manufacturing and trade

sectors.

In North America, releases and recoveries

increased by 14 per cent to US$205 million at

31 December 2009 due to an increase in the

repayment of loans previously impaired in the

corporate, commercial and financial portfolios.

Impaired loans decreased by 7 per cent to

US$13.3 billion at 31 December 2009.

New loan impairment allowances in Latin

America increased by 18 per cent to US$2.9 billion,

while impaired loans rose by 27 per cent to

US$3.0 billion. The increase in new loan impairment

allowances in Brazil was driven by higher

delinquencies, mainly in credit cards, overdrafts and

payroll loans, due to higher unemployment. In the

commercial portfolio, higher new loan impairment

allowances reflected the challenging economic