HSBC 2009 Annual Report Download - page 249

Download and view the complete annual report

Please find page 249 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

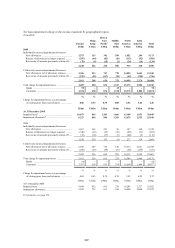

247

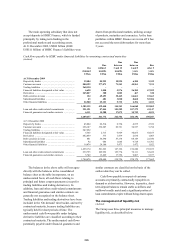

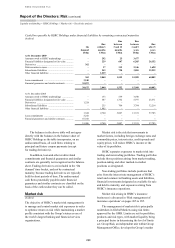

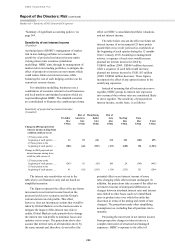

Advances to deposits ratios

Ratio of net liquid assets

to customer liabilities Net liquid assets

2009

2008 2009

2008 2009

2008

%

% %

% US$bn

US$bn

Total of HSBC’s other

principal banking entities37

Year-end ............................ 80.8

85.2 29.4

26.5 94.7

83.5

Maximum ......................... 85.2

92.3 29.4

26.5 94.7

83.5

Minimum .......................... 80.8

82.7 24.7

19.4 73.2

66.1

Average ............................. 82.2

88.1 27.3

22.5 84.8

73.9

For footnote, see page 291.

The reduction in the quantum of net liquid

assets in HSBC Bank USA between 2008 and 2009

reflects the temporary high level of net liquid assets

maintained at the end of 2008 in anticipation of

funding requirements for the credit card portfolios

transferred to HSBC Bank USA from HSBC Finance

in early 2009.

Projected cash flow scenario analysis

The Group uses a number of standard projected cash

flow scenarios designed to model both Group-

specific and market-wide liquidity crises, in which

the rate and timing of deposit withdrawals and

drawdowns on committed lending facilities are

varied, and the ability to access interbank funding

and term debt markets and to generate funds from

asset portfolios is restricted. The scenarios are

modelled by all Group banking entities and by

HSBC Finance. The appropriateness of the

assumptions under each scenario is regularly

reviewed. In addition to the Group’s standard

projected cash flow scenarios, individual entities

are required to design their own scenarios to reflect

specific local market conditions, products and

funding bases.

Limits for cumulative net cash flows under

stress scenarios are set for each banking entity and

for HSBC Finance. Both ratio and cash flow limits

reflect the local market place, the diversity of

funding sources available and the concentration risk

from large depositors. Compliance with entity level

limits is monitored centrally by Group Finance and

reported regularly to the RMM.

HSBC Finance

As HSBC Finance is unable to accept standard

retail customer deposits, it takes funding from the

professional markets. HSBC Finance uses a range

of measures to monitor funding risk, including

projected cash flow scenario analysis and caps

placed on the amount of unsecured term funding

that can mature in any rolling three-month and

rolling 12-month periods. HSBC Finance also

maintains access to committed sources of secured

funding and has in place committed backstop lines

for short-term refinancing CP programmes.

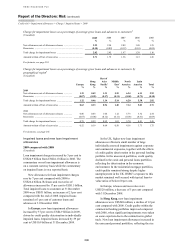

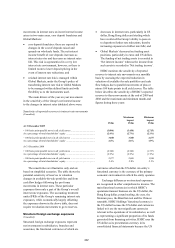

HSBC Finance – funding

(Audited)

At 31 December

2009 2008

US$bn US$bn

Maximum amounts of unsecured term

funding maturing in any rolling:

3 month period ................................. 5.2 6.0

12 month period ............................... 12.3 17.4

Unused committed sources of secured

funding38 ........................................... 0.4 2.4

Committed backstop lines from

non-Group entities in support of

CP programmes ................................ 5.3 7.3

For footnote, see page 291.

The need for HSBC Finance to refinance

maturing term funding is mitigated by the continued

run-down of its balance sheet.

Contingent liquidity risk

(Audited)

In the normal course of business, Group entities

provide customers with committed facilities,

including committed backstop lines to conduit

vehicles sponsored by the Group and standby

facilities to corporate customers. These facilities

increase the funding requirements of the Group

when customers choose to raise drawdown levels

over and above their normal utilisation rates. The

liquidity risk consequences of increased levels of

drawdown are analysed in the form of projected cash

flows under different stress scenarios. The RMM

also sets limits for non-cancellable contingent

funding commitments by Group entity after due

consideration of each entity’s ability to fund them.

The limits are split according to the borrower, the

liquidity of the underlying assets and the size of the

committed line.