HSBC 2009 Annual Report Download - page 248

Download and view the complete annual report

Please find page 248 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

Liquidity and funding > Liquidity risk management / Contingent liquidity risk

246

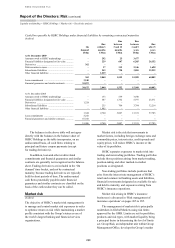

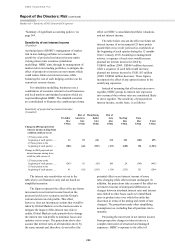

Advances to deposits ratio

HSBC emphasises the importance of core current

accounts and savings accounts as a source of funds

to finance lending to customers, and discourages

reliance on short-term professional funding. This is

achieved by placing limits on Group banking entities

which restrict their ability to increase loans and

advances to customers without corresponding

growth in current accounts and savings accounts.

This measure is referred to as the ‘advances to

deposits’ ratio.

Advances to deposits ratio limits are set by the

RMM and monitored by Group Finance. The ratio

describes loans and advances to customers as a

percentage of the total of core customer current and

savings accounts and term funding with a remaining

term to maturity in excess of one year. Loans and

advances to customers which are part of reverse

repurchase arrangements, and where HSBC receives

securities which are deemed to be liquid, are

excluded from the advances to deposits ratio. The

classification of a deposit as ‘core’ includes

consideration of the size of the customer’s total

deposit balances, the pricing and the deposit’s

behavioural characteristics.

The three principal banking entities listed in the

table below represented 70 per cent of HSBC’s total

core deposits at 31 December 2009 (2008: 70 per

cent). The table shows that loans and advances to

customers in HSBC’s principal banking entities are

overwhelmingly financed by reliable and stable

sources of funding. HSBC would meet any

unexpected net cash outflows by selling securities

and accessing additional funding sources such as

interbank or collateralised lending markets. The

distinction between core and non-core deposits

generally means that the Group’s measure of

advances to deposits is more restrictive than that

which could be inferred from the published financial

statements. For example, HSBC’s consolidated

advances to deposits measure at 31 December 2009

based only on published balance sheet information

was 77.3 per cent (2008: 83.6 per cent).

Ratio of net liquid assets to customer

liabilities

Net liquid assets are the aggregated liquid assets

less all funds maturing in the next 30 days from

wholesale market sources and from customers who

are deemed to be professional. For this purpose,

HSBC defines liquid assets as cash balances, short-

term interbank deposits and highly-rated debt

securities available for immediate sale and for which

a deep and liquid market exists. Contingent liquidity

risk associated with committed loan facilities is not

reflected in the ratios. The Group’s framework for

monitoring this risk is described in ‘Contingent

liquidity risk’ below.

Limits for the ratio of net liquid assets to

customer liabilities are set for each bank operating

entity, but not for HSBC Finance. As HSBC Finance

does not accept customer deposits, it is not

appropriate to manage its liquidity using standard

liquidity ratios. See ‘HSBC Finance’ below.

Ratios of net liquid assets to customer liabilities

are provided in the following table, along with the

US dollar equivalents of net liquid assets.

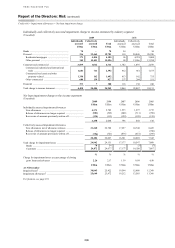

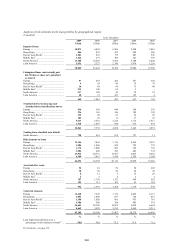

HSBC’s principal banking entities – the management of liquidity risk

(Audited)

Advances to deposits ratios

Ratio of net liquid assets

to customer liabilities Net liquid assets

2009

2008 2009

2008 2009

2008

%

% %

% US$bn

US$bn

HSBC Bank (UK operations)

Year-end ............................ 102.3

106.0 8.8

7.1 29.2

21.3

Maximum ......................... 107.7

106.7 13.6

14.1 46.2

52.5

Minimum .......................... 101.7

97.5 6.5

6.9 19.5

21.3

Average ............................. 105.1

101.5 10.2

10.0 32.6

35.8

The Hongkong and Shanghai

Banking Corporation

Year-end ............................ 70.9

77.4 30.0

25.0 84.9

64.6

Maximum ......................... 77.4

82.9 35.0

25.0 97.8

64.6

Minimum .......................... 68.6

76.7 25.0

19.9 64.6

51.1

Average ............................. 71.5

80.6 30.7

21.9 85.1

56.5

HSBC Bank USA

Year-end ............................ 98.1

103.7 17.8

31.5 14.1

27.4

Maximum ......................... 110.6

117.3 31.5

31.5 27.4

27.4

Minimum .......................... 98.1

103.7 16.7

15.8 13.2

17.1

Average ............................. 105.4

111.8 22.2

22.6 18.9

21.5