HSBC 2009 Annual Report Download - page 277

Download and view the complete annual report

Please find page 277 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

275

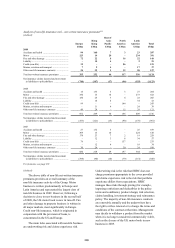

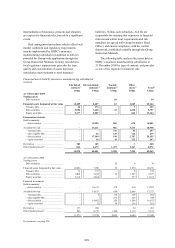

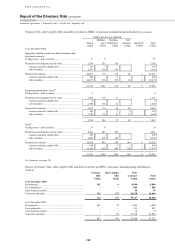

A certain number of these products have been

discontinued, including the US$553 million

immediate annuity portfolio in HSBC Finance

where, as highlighted in the above table, the current

portfolio yield is less than the guarantee. On

acquisition of this block of business by HSBC

Finance, a provision was established to mitigate the

shortfall in yields. There has been no further

deterioration in the shortfall since acquisition. There

are a limited number of additional contracts where

the current portfolio yield is less than the guarantee

implied by the contract.

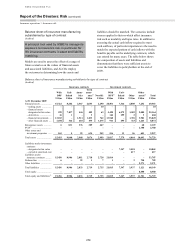

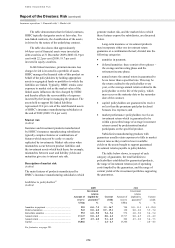

The proceeds from insurance and investment

products with DPF are primarily invested in bonds

with a proportion allocated to equity securities in

order to provide customers with the potential for

enhanced returns. Subsidiaries with portfolios of

such products are exposed to the risk of falls in the

market price of equity securities when they cannot

be fully reflected in the discretionary bonuses. An

increase in market volatility could also result in

an increase in the value of the guarantee to the

policyholder.

Long-term insurance and investment products

typically permit the policyholder to surrender the

policy or let it lapse at any time. When the surrender

value is not linked to the value realised from the sale

of the associated supporting assets, the subsidiary

is exposed to market risk. In particular, when

customers seek to surrender their policies when asset

values are falling, assets may have to be sold at a

loss to fund redemptions.

A subsidiary holding a portfolio of long-term

insurance and investment products, especially with

DPF, may attempt to reduce exposure to its local

market by investing in assets in countries other

than that in which it is based. These assets may

be denominated in currencies other than the

subsidiary’s local currency. It is often not cost

effective for the subsidiary to hedge the foreign

exchange exposure associated with these assets, and

this exposes it to the risk that its local currency will

strengthen against the currency of the related assets.

For unit-linked contracts, market risk is

substantially borne by the policyholder, but HSBC

typically remains exposed to market risk as the

market value of the linked assets influences the fees

HSBC earns for managing them.

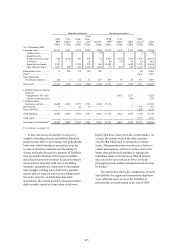

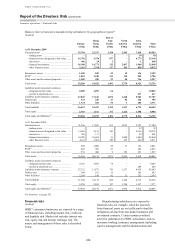

How the risks are managed

(Audited)

HSBC’s insurance manufacturing subsidiaries

manage market risk by using some or all of the

following techniques, depending on the nature of the

contracts they write:

• for products with DPF, adjusting bonus rates to

manage the liabilities to policyholders. Bonus

rates are managed by regularly evaluating their

sustainability. The effect is that a significant

portion of the market risk is borne by the

policyholder;

• as far as possible, matching assets to liabilities.

For example, for products with annual return or

capital guarantees, HSBC seeks to invest in

bonds which produce returns at least equal to

the investment returns implied by the guarantees

while remaining attentive to the overall portfolio

credit quality;

• using derivatives in a limited number of

instances;

• when designing new products with investment

guarantees, evaluating the cost of the guarantee

and considering this cost when determining the

level of premiums or the price structure;

• periodically reviewing products identified as

higher risk, which contain guarantees and

embedded optionality features linked to savings

and investment products. The scope of the

review would include pricing, risk management

and profitability (a control introduced during

2008). Guaranteed products which expose the

Group to risk beyond the levels deemed

acceptable in any of these categories are either

altered or are no longer offered to customers;

• including features designed to mitigate market

risk in new products, such as charging surrender

penalties to recoup losses incurred when

policyholders surrender their policies; and

• exiting, to the extent possible, investment

portfolios whose risk is considered unacceptable

– for example, by implementing asset

reallocation strategies in order to manage risk

exposures.

The product approval process includes the

identification and assessment of the risk

embedded in new products.

Group Insurance Head Office includes a Chief

Market and Liquidity Risk Officer reporting to the

Chief Risk Officer. Each regional insurance unit