Energizer 2010 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2010 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Exhibit 13

ENERGIZER HOLDINGS, INC.

(Dollars in millions, except per share and percentage data)

94

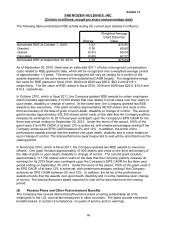

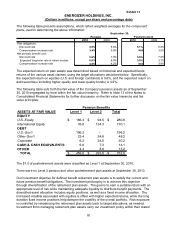

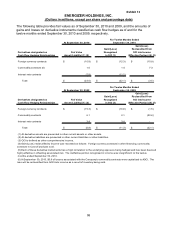

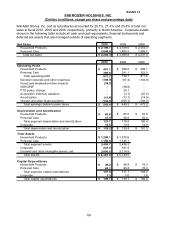

The detail of long-term debt at September 30 for the year indicated is as follows:

2010 2009

Private Placement, fixed interest rates ranging from 3.9% to 6.6%, due

2011 to 2017

1,835.0$ 1,930.0$

Term Loan, variable interest at LIBOR + 63 basis points, or 0.9%, due

2012

453.5 459.5

Total long-term debt, including current maturities 2,288.5 2,389.5

Less current portion 266.0 101.0

Total long-term debt 2,022.5$ 2,288.5$

The Company’s total borrowings were $2,313.4 at September 30, 2010, including $478.4 tied to

variable interest rates, of which $300 is hedged via the interest rate swap noted below. The

Company maintains total debt facilities of $2,588.4, exclusive of available borrowings under the

receivables securitization program, of which $259.7 remained available as of September 30,

2010.

During the second quarter of fiscal 2009, the Company entered into interest rate swap

agreements with two major financial institutions that fixed the variable benchmark component

(LIBOR) of the Company’s interest rate on $300 of the Company’s variable rate debt through

December 2012 at an interest rate of 1.9%.

In May 2011, the Company’s $275 U.S. revolving credit facility will mature. At September 30,

2010, there were no outstanding borrowings under this facility. It is our intent to renew this

facility in advance of the May maturity date. However, we can provide no assurances that this

facility will be renewed, or if renewed, that the terms will be as favorable as those contained in

the existing facility.

Under the terms of the Company’s credit agreements, the ratio of the Company’s indebtedness

to its EBITDA, as defined in the agreements and detailed below, cannot be greater than 4.00 to

1, and may not remain above 3.50 to 1 for more than four consecutive quarters. If and so long as

the ratio is above 3.50 to 1 for any period, the Company is required to pay additional interest

expense for the period in which the ratio exceeds 3.50 to 1. The interest rate margin and certain

fees vary depending on the indebtedness to EBITDA ratio. Under the Company’s private

placement note agreements, the ratio of indebtedness to EBITDA may not exceed 4.0 to 1.

However, if the ratio is above 3.50 to 1, the Company is required to pay an additional 75 basis

points in interest for the period in which the ratio exceeds 3.50 to 1. In addition, under the credit

agreements, the ratio of its current year EBIT, as defined in the agreements, to total interest

expense must exceed 3.00 to 1. The Company’s ratio of indebtedness to its EBITDA was 2.70 to

1, and the ratio of its EBIT to total interest expense was 5.72 to 1, as of September 30, 2010.

The Company anticipates that it will remain in compliance with its debt covenants for the

foreseeable future. The negative impact on EBITDA resulting primarily from the Venezuela

devaluation of $18.3, pre-tax, is included in the trailing twelve month EBITDA calculation at

September 30, 2010, and negatively impacted the ratio of indebtedness to EBITDA at

September 30, 2010. If the Company fails to comply with the financial covenants referred to

above or with other requirements of the credit agreements or private placement note

agreements, the lenders would have the right to accelerate the maturity of the debt. Acceleration

under one of these facilities would trigger cross defaults on other borrowings.