Cincinnati Bell 2012 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2012 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

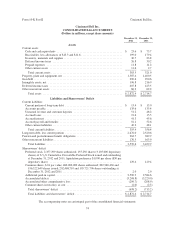

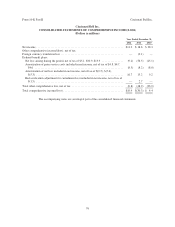

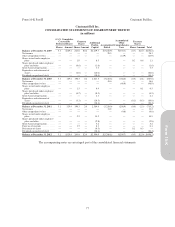

allowance for uncollectible accounts in the Consolidated Balance Sheets. The Company establishes the

allowances for uncollectible accounts using percentages of aged accounts receivable balances to reflect the

historical average of credit losses as well as specific provisions for certain identifiable, potentially uncollectible

balances. When internal collection efforts on accounts have been exhausted, the accounts are written off and the

associated allowance for uncollectible accounts is reduced.

Inventory, Materials and Supplies — Inventory, materials and supplies consists of wireless handsets,

wireline network components, various telephony and IT equipment to be sold to customers, maintenance

inventories, and other materials and supplies, which are carried at the lower of average cost or market.

Property, Plant and Equipment — Property, plant and equipment is stated at original cost and presented

net of accumulated depreciation and impairment losses. Maintenance and repairs are charged to expense as

incurred while improvements which extend an asset’s useful life or increase its functionality are capitalized and

depreciated over the asset’s remaining life. The majority of the Wireline network property, plant and equipment

used to generate its voice and data revenue is depreciated using the group method, which develops a depreciation

rate annually based on the average useful life of a specific group of assets rather than for each individual asset as

would be utilized under the unit method. The estimated life of the group changes as the composition of the group

of assets and their related lives change. Provision for depreciation of other property, plant and equipment, except

for leasehold improvements, is based on the straight-line method over the estimated economic useful life.

Depreciation of leasehold improvements is based on a straight-line method over the lesser of the economic useful

life of the asset or the term of the lease, including optional renewal periods if renewal of the lease is reasonably

assured.

Additions and improvements, including interest and certain labor costs incurred during the construction

period, are capitalized. The Company records the fair value of a legal liability for an asset retirement obligation

in the period it is incurred. The estimated removal cost is initially capitalized and depreciated over the remaining

life of the underlying asset. The associated liability is accreted to its present value each period. Once the

obligation is ultimately settled, any difference between the final cost and the recorded liability is recognized as

income or loss on disposition.

Goodwill and Indefinite-Lived Intangible Assets

Goodwill — Goodwill represents the excess of the purchase price consideration over the fair value of net

assets acquired and recorded in connection with business acquisitions. Goodwill is generally allocated to

reporting units one level below business segments. Goodwill is tested for impairment on an annual basis or when

events or changes in circumstances indicate that such assets may be impaired. If the net book value of the

reporting unit exceeds its fair value, an impairment loss may be recognized. An impairment loss is measured as

the excess of the carrying value of goodwill of a reporting unit over its implied fair value. The implied fair value

of goodwill represents the difference between the fair value of the reporting unit and the fair value of all the

assets and liabilities of that unit, including any unrecognized intangible assets.

Intangible assets not subject to amortization — Intangible assets represent purchased assets that lack

physical substance but can be separately distinguished from goodwill because of contractual or legal rights, or

because the asset is capable of being separately sold or exchanged. Federal Communications Commission

(“FCC”) licenses for wireless spectrum represent indefinite-lived intangible assets. The Company may renew the

wireless licenses in a routine manner every ten years for a nominal fee, provided the Company continues to meet

the service and geographic coverage provisions required by the FCC. Intangible assets not subject to amortization

are tested for impairment annually, or when events or changes in circumstances indicate that the asset might be

impaired.

Long-Lived Assets — Management reviews the carrying value of property, plant and equipment and other

long-lived assets, including intangible assets with definite lives, when events or changes in circumstances

indicate that the carrying amount of the assets may not be recoverable. An impairment loss is recognized when

the estimated future undiscounted cash flows expected to result from the use of an asset (or group of assets) and

80

Form 10-K Part II Cincinnati Bell Inc.