Cincinnati Bell 2012 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2012 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

calculating the expenses and liabilities related to these plans. The most significant of these numerous

assumptions, which are reviewed annually, include the discount rate, expected long-term rate of return on plan

assets and healthcare cost trend rates.

Discount rate

A discount rate is used to measure the present value of projected benefit obligations. The discount rate for each

plan is individually calculated based upon the timing of expected future benefit payments. Our discount rates are

derived based upon a yield curve developed to reflect yields available on high-quality corporate bonds as of the

measurement date. As of December 31, 2012 and 2011, the discount rate used to value the pension plans was 3.30%

and 3.90%, respectively, while the discount rate used to value the postretirement plans was 3.10% and 3.60%.

Lower rates of interest available on high-quality corporate bonds drove the decrease in the discount rates in 2012.

Expected rate of return

The expected long-term rate of return on plan assets, developed using the building block approach, is based

on the mix of investments held directly by the plans, and the current view of expected future returns, which is

influenced by historical averages. The required use of an expected versus actual long-term rate of return on plan

assets may result in recognized pension expense or income that is greater or less than the actual returns of those

plan assets in any given year. Over time, however, the expected long-term returns are designed to approximate

the actual long-term returns. As of December 31, 2012 and 2011, the estimated long-term rate of return on

pension plan assets was 7.75%. The long-term rate of return on postretirement plan assets was estimated to be

zero in both periods as these plans have minimal assets with a low rate of return. Actual asset returns for the

pension trusts, which represent over 90% of invested assets, were gains of 15% in 2012, 6% in 2011, and 14% in

2010. In our pension calculations, we utilized the market-related value of plan assets, which is a calculated asset

value that recognizes changes in asset fair values in a systematic and consistent manner. Differences between

actual and expected returns are recognized in the market-related value of plan assets over five years.

Healthcare cost trend

Our healthcare cost trend rate is developed based on historical cost data, the near-term outlook, and an

assessment of likely long-term trends. As of both December 31, 2012 and 2011, the healthcare cost trend rate

used to measure the postretirement health benefit obligation was 6.5% and 8.0%, respectively. As of

December 31, 2012, the healthcare cost trend rate is assumed to decrease gradually to 4.5% by the year 2016.

The actuarial assumptions used may differ materially from actual results due to the changing market and

economic conditions and other changes. Revisions to and variations from these estimates would impact assets,

liabilities, equity, cash flow, costs of services and products, and selling, general and administrative expenses.

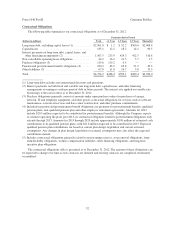

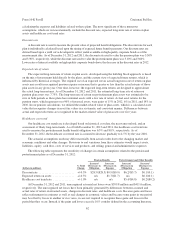

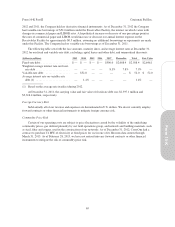

The following table represents the sensitivity of changes in certain assumptions related to the pension and

postretirement plans as of December 31, 2012:

Pension Benefits Postretirement and Other Benefits

(dollars in millions)

% Point

Change

Increase/

(Decrease) in

Obligation

Increase/

(Decrease) in

Expense

Increase/

(Decrease) in

Obligation

Increase/

(Decrease) in

Expense

Discount rate ......................... +/-0.5% $28.5/($28.5) $0.9/($0.9) $6.2/($5.7) $0.1/(0.1)

Expected return on assets ............... +/-0.5% n/a $1.7/($1.7) n/a $0.1/(0.1)

Healthcare cost trend rate ............... +/-1.0% n/a n/a $5.4/($4.8) $0.2/($0.2)

At December 31, 2012 and 2011, unrecognized actuarial net losses were $399.8 million and $411.6 million,

respectively. The unrecognized net losses have been primarily generated by differences between assumed and

actual rates of return on invested assets, changes in discount rates, and healthcare costs. Because gains and losses

reflect refinements in estimates as well as real changes in economic values and because some gains in one period

may be offset by losses in another or vice versa, we are not required to recognize these gains and losses in the

period that they occur. Instead, if the gains and losses exceed a 10% corridor defined in the accounting literature,

62

Form 10-K Part II Cincinnati Bell Inc.