Cincinnati Bell 2012 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2012 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

obligations to fund our qualified pension plans. Based on current legislation and current actuarial assumptions,

we estimate these contributions to approximate $190 million over the period from 2013 to 2020. It is also

possible that we will use a portion of our cash flows generated from operations for de-leveraging in the future,

including discretionary, opportunistic repurchases of debt prior to the scheduled maturities. On January 24, 2013,

we completed the IPO of CyrusOne, our former data center colocation business. It is management’s intent to sell

down the Company’s interests in CyrusOne over time and use such proceeds to further de-leverage the Company.

During the fourth quarter of 2012, the Company’s $210 million revolving credit facility, previously expiring

in June 2014, was replaced with a new $200 million Corporate Credit Agreement that expires in July 2017.

Proceeds from this new facility may be used for ongoing working capital and for other general corporate

purposes. The amount available under this facility will be reduced to $150 million by December 31, 2014 and

further reduced to $125 million on December 31, 2015, subject to the amount of cash proceeds received by the

Company from any sales of its ownership in CyrusOne’s common stock. This new Corporate Credit Agreement

contains financial covenants that require us to maintain certain leverage and interest coverage ratios, and limits

our capital expenditures on an annual basis. Capital expenditures are permitted subject to predetermined annual

thresholds which are not to exceed $955 million in the aggregate over the next five years. The facility also has

certain covenants, which, among other things, limit our ability to incur additional debt or liens, pay dividends,

sell, transfer, lease, or dispose of assets, and make certain investments or merge with another company. If the

Company were to violate any of its covenants and were unable to obtain a waiver, it would be considered in

default. If the Company were in default under its credit facility, no additional borrowings under the credit facility

would be available until the default was waived or cured.

In addition, the CyrusOne Credit Agreement required CyrusOne to maintain a certain secured net leverage

ratio, ratio of EBITDA to fixed charges and ratio of total indebtedness to gross asset value, in each case on a

consolidated basis. Notwithstanding these limitations, CyrusOne will be permitted, subject to the terms and

conditions of the CyrusOne Credit Agreement, to distribute to its shareholders cash dividends in an amount not to

exceed 95% of its adjusted funds from operations for any period. Similarly, CyrusOne’s indenture permits

dividends and distributions necessary for CyrusOne to maintain its status as a real estate investment trust.

As of December 31, 2012, the Company was in compliance with both the Corporate and CyrusOne Credit

Agreement covenants.

Various issuances of the Company’s public debt, which include the 8

1

⁄

4

% Senior Notes due 2017, the 8

3

⁄

4

%

Senior Subordinated Notes due 2018, the 8

3

⁄

8

% Senior Notes due 2020, and the CyrusOne 6

3

⁄

8

% Senior Notes

contain covenants that, among other things, limit the Company’s ability to incur additional debt or liens, pay

dividends or make other restricted payments, sell, transfer, lease, or dispose of assets and make investments or

merge with another company. As of December 31, 2012, the Company was in compliance with these covenants.

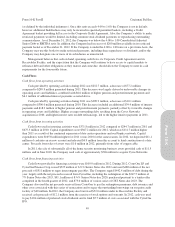

The Company’s most restrictive covenants are generally included in its Corporate Credit Agreement. In

order to continue to have access to the amounts available to it under the Corporate Credit Agreement, the

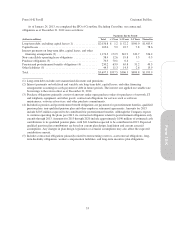

Company must remain in compliance with all covenants. The following table presents the calculation of the most

restrictive debt covenant, the Consolidated Total Leverage Ratio, as of and for the year ended December 31,

2012:

(dollars in millions)

Consolidated Total Leverage Ratio as of December 31, 2012 ......... 5.12

Maximum ratio permitted for compliance ........................ 7.25

Consolidated Funded Indebtedness additional availability ........... $ 894.1

Consolidated EBITDA clearance over compliance threshold ......... $ 123.3

Definitions and components of this calculation are detailed in our credit agreement and can be found in the

Company’s Form 8-K filed on November 20, 2012.

In various issuances of the Company’s public debt indentures, a financial covenant exists that permits the

incurrence of additional Indebtedness up to a 4:00 to 1:00 Consolidated Adjusted Senior Debt to EBITDA ratio

48

Form 10-K Part II Cincinnati Bell Inc.