Blackberry 2004 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2004 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

|

|

35

For the years ended February 28, 2004, March 1, 2003 and March 2, 2002

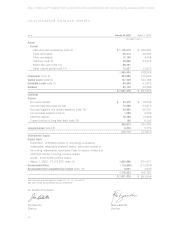

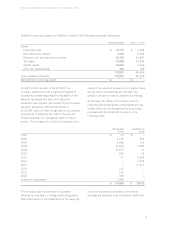

(e) Cash and cash equivalents

Cash and cash equivalents consist of balances

with banks and liquid short-term investments with

maturities of three months or less at the date of

acquisition and are carried on the balance sheet

at fair value.

(f) Short-term investments

Short-term investments consist of liquid investments

with maturities of between three months and one

year at the date of acquisition. Such short-term

investments are available for sale investments and

are carried on the balance sheet at fair value.

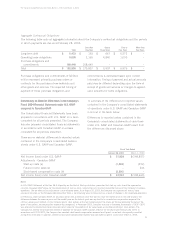

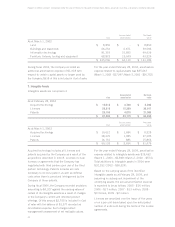

(g) Trade receivables

Trade receivables are presented net of allowance for

doubtful accounts. The allowance was $2,379 at

February 28, 2004 (March 1, 2003 - $2,331). Bad

debt expense (recovery) was $(548) for the year

ended February 28, 2004 (March 1, 2003 - $696;

March 2, 2002 - $6,236).

The allowance for doubtful accounts reflects

estimates of probable losses in trade receivables.

The allowance is determined based on specifically

identified accounts, historical experience and all

other current information.

(h) Investments

All investments with maturities in excess of one year

are classified as long-term investments. In the event

of a decline in value which is other than temporary,

the investments are written down to estimated

realizable value.

Investments designated as held-to-maturity

investments are carried at cost. The Company

does not exercise significant influence with respect

to any of these investments.

Investments designated as available-for-sale

investments are carried at fair value. Unrealized

gains or losses are included in other comprehensive

income.

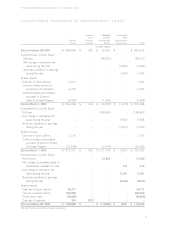

(i) Derivative financial instruments

The Company utilizes forward foreign exchange rate

contracts and foreign exchange rate swaps to reduce

exposure to fluctuations in foreign currency exchange

rates. The Company does not purchase or hold

derivative financial instruments for speculative

purposes.

The Company formally documents relationships

between hedging instruments and associated

hedged items. This documentation includes:

identification of the specific foreign currency asset,

liability or forecasted transaction being hedged; the

nature of the risk being hedged; the hedge

objective; and the method of assessing hedge

effectiveness. Hedge effectiveness is formally

assessed, both at hedge inception and on an

ongoing basis, to determine whether the derivatives

used in hedging transactions are highly effective in

offsetting changes in foreign currency denominated

assets, liabilities and anticipated cash flows of

hedged items.

Statement of Financial Accounting Standards

(“SFAS”) 133, Accounting for Derivative

Instruments, as amended by SFAS 137, 138 and 149,

requires all derivative instruments to be recognized

at fair value on the consolidated balance sheet, and

outlines the criteria to be met in order to designate

a derivative instrument as a hedge and the methods

for evaluating hedge effectiveness. For instruments

designated as fair value hedges, changes in fair

value are recognized in current earnings, and will

generally be offset by changes in the fair value of

the associated hedged transaction. For instruments

designated as cash flow hedges, the effective

portion of changes in fair value are recorded in other

comprehensive income, and subsequently

reclassified to earnings in the period in which the

cash flows from the associated hedged transaction

affect earnings. When an anticipated transaction is

no longer likely to occur, the corresponding

derivative instrument is de-designated as a hedge,

and changes in the fair value of the instrument are

recognized in net income.