BMW 2007 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2007 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

|

|

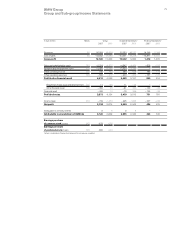

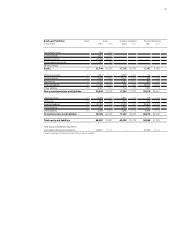

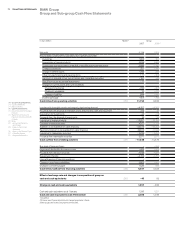

68 Group Management Report

10 Group Management Report

10 A Review of the Financial Year

13 General Economic Environment

17 Review of Operations

41 BMW Stock and Bonds

44 Disclosures relating to Takeover

Regulations and Explanatory Report

47 Financial Analysis

47 – Internal Management System

49 – Earnings Performance

51 – Financial Position

52 – Net Assets Position

55 – Subsequent Events Report

55 – Value Added Statement

57 – Key Performance Figures

58 – Comments on BMW AG

62 Risk Management

68 Outlook

The economic environment in 2008

The BMW Group forecasts that the global economy

will again lose some of its momentum in 2008, but

will nevertheless continue to grow. The pace will again

be set by the emerging markets in Asia, Latin America

and Eastern Europe, whereas growth in North America

and the rest of Europe is likely to be robust, but no-

where near as high. From today’s perspective, the

US credit crisis is not expected to result in massive

global economic upheaval. It could, however, hold

down domestic demand somewhat, particularly in

the USA itself, without causing a recession there.

The US growth rate in 2008 will again remain

below the average registered in recent years. The

impact of the property and credit crisis is not likely

to tail off until the second half of the year at the earli-

est. The US Federal Reserve will no doubt endeavour

to stimulate the economy with further interest rate

cuts. It is nevertheless likely that consumers will be

much more reluctant to spend than they were a

year ago. Overall, the growth rate should remain at

roughly the same level as in the previous year.

By contrast, a slowdown in growth is forecasted

for Europe in 2008. Firstly, higher interest rates will

take their toll and hold down investment volumes.

Secondly, export growth is likely to weaken once

again. The sharp increase in the inflation rate at the

turn of the year will probably deter the European

Central Bank from lowering interest rates significantly.

The growth rate for Germany will also weaken.

Whereas private consumption is forecasted to re-

main buoyant, exports and particularly investments

are likely to grow at a much slower pace.

The Japanese economy should grow in 2008

at a somewhat lower pace to that of 2007, with

momentum still coming from both the domestic

market and abroad. The recent sharp rise in con-

sumer prices – mostly due to higher energy prices

– should make it easier for the Japanese central

bank to increase interest rates in small steps.

The emerging economies of Asia, Latin America

and Eastern Europe will continue to expand rapidly

with growth rates only marginally down on the pre-

vious year.

A generally strong euro expected

The euro again appreciated sharply against the US

dollar in the course of 2007. Lower interest rates,

weaker growth and the USA’s high current account

deficit all suggest that the US dollar is likely to remain

weak in the near future.

Although the British pound fell steeply during

the second half of 2007, it is not expected to suffer

any further significant loss in value.

The Japanese yen also depreciated sharply in

2007. The fact that interest rates are still on the low

side in Japan means that the yen is likely to remain

undervalued for the time being.

Risks affecting economic growth

Energy and commodity prices will remain high in

2008, reflecting the fact that demand – in particular

from the emerging economies – will continue to

grow strongly. With the global economy still enjoying

robust growth and the US dollar weakening, com-

modities are likely to remain in demand as an invest-

ment in the near future. As a result of the extremely

tense situation on the markets, the risk of specula-

tive price rises remains present for the foreseeable

future. The most significant risk emanates from the

credit crisis in the USA. Should the crisis become

more serious in the USA or spill over into other

markets, this could result in a significantly lower

global growth rate. All in all, the credit crisis causes

forecasts for 2008 to be subject to a high degree of

uncertainty.

Economic outlook for the automobile industry

in 2008

The global automotive economy will again be driven

by the emerging economies of Asia, Eastern Europe

and Latin America, whereas sales on the three main

traditional markets (Japan, the USA and Western

Europe) are likely to stagnate.

Double-digit growth is again forecasted for China

and India in 2008. The forecast for Russia and some

of the Latin American markets is on a similar scale.

Growth will also remain strong overall in Eastern

Europe.

Outlook