Air New Zealand 2014 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2014 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

AIR NEW ZEALAND ANNUAL FINANCIAL RESULTS 201412

Where the hedge relationship continues throughout its designated term, the amount recognised in the cash flow hedge reserve is

transferred to the Statement of Financial Performance in the same period that the hedged item is recorded in the Statement of Financial

Performance, or, when the hedged item is a non-financial asset, the amount recognised in the cash flow hedge reserve is transferred to

the carrying amount of the asset when it is recognised.

Net investment hedge

Hedges of net investments in foreign operations are accounted for similarly to cash flow hedges. Any gain or loss on the hedging

instrument relating to the effective portion of the hedge is recognised in other comprehensive income and accumulated in the foreign

currency translation reserve within equity. The gain or loss relating to the ineffective portion of the hedge is recognised immediately in

the Statement of Financial Performance.

Fair value hedges

Changes in the fair value of hedging instruments designated as fair value hedges are recognised in the Statement of Financial

Performance. The hedged item is adjusted to reflect changes in its fair value in respect of the risk being hedged. The gain or loss

attributable to the hedged risk is recognised in the Statement of Financial Performance with an adjustment to the carrying amount of the

hedged item.

FAIR VALUE ESTIMATION

The fair value of the investment in quoted equity instruments is determined by reference to quoted market prices in an active market.

This equates to “Level 1” of the fair value hierarchy defined within NZ IFRS - 13 Fair Value Measurement. The fair value of derivative

financial instruments is based on published market prices for similar assets or liabilities or market observable inputs to valuation at

balance date (“Level 2” of the fair value hierarchy). The fair value of interest-bearing liabilities for disclosure purposes is calculated based

on the present value of future principal and interest cash flows, discounted at the market rate of interest for similar liabilities at reporting

date. The fair value of all other financial instruments approximates the carrying value.

OFFSETTING FINANCIAL ASSETS AND FINANCIAL LIABILITIES

Financial assets and financial liabilities are offset and the net amount reported in the Statement of Financial Position when there is a

legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis or realise the asset and settle

the liability simultaneously.

PROPERTY, PLANT AND EQUIPMENT

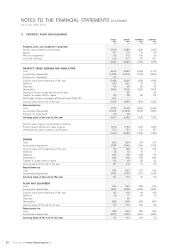

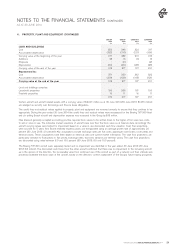

Owned assets

Items of property, plant and equipment are stated at cost or deemed cost less accumulated depreciation and accumulated impairment

losses. Cost includes expenditure that is directly attributable to the acquisition of the item and in bringing the asset to the location and

working condition for its intended use. Cost may also include transfers from equity of any gains or losses on qualifying cash flow hedges

of foreign currency purchases of property, plant and equipment.

Where significant parts of an item of property, plant and equipment have different useful lives, they are accounted for separately.

A portion of the cost of an acquired aircraft is attributed to its service potential (reflecting the maintenance condition of its engines) and

is depreciated over the shorter of the period to the next major inspection event, overhaul, or the remaining life of the asset.

Leased assets

Leases under which the Group assumes substantially all the risks and rewards of ownership are classified as finance leases. All other

leases are classified as operating leases.

Upon initial recognition, assets held under finance leases are measured at amounts equal to the lower of their fair value and the present

value of the minimum lease payments at inception of the lease. A corresponding liability is also established.

Subsequent to initial recognition, the asset is accounted for in accordance with the accounting policy applicable to that asset.

Manufacturers’ credits

The Group receives credits and other contributions from manufacturers in connection with the acquisition of certain aircraft and engines.

Depending on the reason for which the amounts are received, the credits and other contributions are either recorded as a reduction

to the cost of the related aircraft and engines, or offset against the associated operating expense. When the aircraft are held under

operating leases, the amounts are deferred and deducted from the operating lease rentals on a straight-line basis over the period of the

related lease as deferred credits.

STATEMENT OF ACCOUNTING POLICIES (CONTINUED)

FOR THE YEAR TO 30 JUNE 2014