AT&T Wireless 2014 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2014 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

Notes to Consolidated Financial Statements (continued)

Dollars in millions except per share amounts

58

|

AT&T INC.

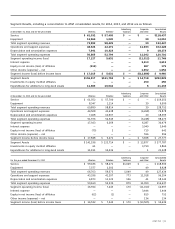

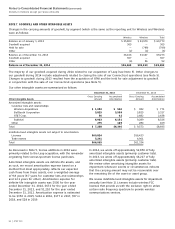

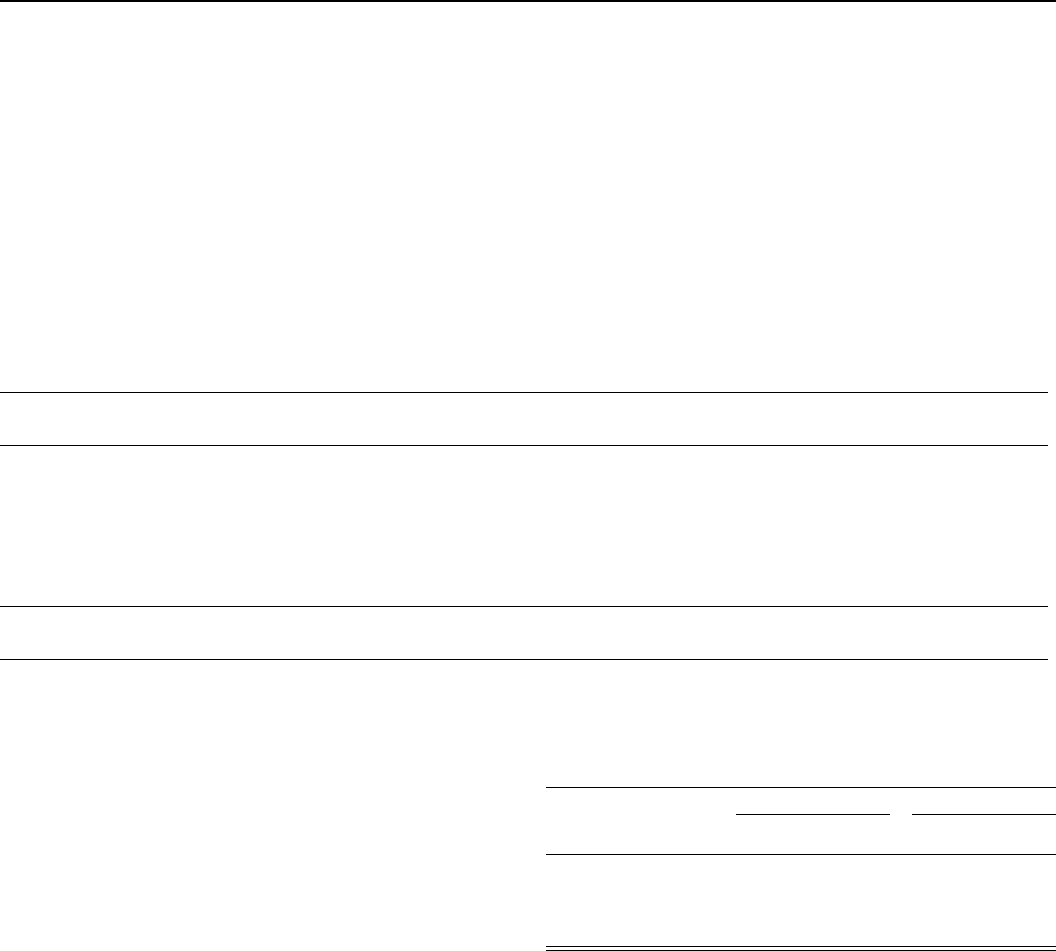

Long-Term Debt and Other Financial Instruments

The carrying amounts and estimated fair values of our

long-term debt, including current maturities and other

financial instruments, are summarized as follows:

December 31, 2014 December 31, 2013

Carrying Fair Carrying Fair

Amount Value Amount Value

Notes and debentures $81,632 $90,367 $74,484 $79,309

Commercial paper — — 20 20

Bank borrowings 5 5 1 1

Investment securities 2,735 2,735 2,450 2,450

The carrying value of debt with an original maturity of

less than one year approximates fair value. The fair value

measurements used for notes and debentures are

considered Level 2 and are determined using various

methods, including quoted prices for identical or similar

securities in both active and inactive markets.

The fair value measurements level of an asset or liability

within the fair value hierarchy is based on the lowest

level of any input that is significant to the fair value

measurement. Valuation techniques used should maximize

the use of observable inputs and minimize the use of

unobservable inputs.

The valuation methodologies described above may produce

a fair value calculation that may not be indicative of future

net realizable value or reflective of future fair values.

We believe our valuation methods are appropriate and

consistent with other market participants. The use of

different methodologies or assumptions to determine the

fair value of certain financial instruments could result in

a different fair value measurement at the reporting date.

There have been no changes in the methodologies used

since December 31, 2013.

unless the lowest of such ratings is more than one level

below the highest of such ratings, in which case the

pricing will be the rating that is one level above the

lowest of such ratings.

The 18-Month Credit Agreement contains affirmative and

negative covenants and events of default equivalent to

those contained in the Syndicated Credit Agreement.

The Applicable Margin for a Eurodollar Rate Advance under

the 18-Month Credit Agreement will equal 0.800%, 0.900%

or 1.000% per annum, depending on AT&T’s credit rating.

The Applicable Margin for a Base Rate Advance under the

18-Month Credit Agreement will be 0%.

In the event that AT&T’s unsecured senior long-term

debt ratings are split by S&P, Moody’s and Fitch, then the

Applicable Margin will be determined by the highest rating,

NOTE 10. FAIR VALUE MEASUREMENTS AND DISCLOSURE

The Fair Value Measurement and Disclosure framework provides a three-tiered fair value hierarchy that gives highest priority

to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest

priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy are described below:

LEVEL 1 Inputs to the valuation methodology are unadjusted quoted prices for identical assets or liabilities in active

markets that we have the ability to access.

LEVEL 2 Inputs to the valuation methodology include:

• Quoted prices for similar assets and liabilities in active markets.

• Quoted prices for identical or similar assets or liabilities in inactive markets.

• Inputs other than quoted market prices that are observable for the asset or liability.

• Inputs that are derived principally from or corroborated by observable market data by correlation or other

means.

LEVEL 3 Inputs to the valuation methodology are unobservable and significant to the fair value measurement.

• Fair value is often based on developed models in which there are few, if any, external observations.