AT&T Wireless 2014 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2014 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

AT&T INC.

|

35

principal payments. Likewise, periodically we enter into

interest rate locks to partially hedge the risk of increases

in the benchmark interest rate during the period leading

up to the probable issuance of fixed-rate debt. We expect

gains or losses in our cross-currency swaps and interest

rate locks to offset the losses and gains in the financial

instruments they hedge.

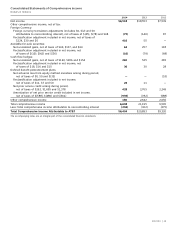

Following are our interest rate derivatives subject to

material interest rate risk as of December 31, 2014.

The interest rates illustrated below refer to the average

rates we expect to pay based on current and implied

forward rates and the average rates we expect to receive

based on derivative contracts. The notional amount is the

principal amount of the debt subject to the interest rate

swap contracts. The fair value asset (liability) represents

the amount we would receive (pay) if we had exited the

contracts as of December 31, 2014.

Interest Rate Risk

The majority of our financial instruments are medium- and

long-term fixed-rate notes and debentures. Changes in

interest rates can lead to significant fluctuations in the

fair value of these instruments. The principal amounts

by expected maturity, average interest rate and fair value

of our liabilities that are exposed to interest rate risk

are described in Notes 9 and 10. In managing interest

expense, we control our mix of fixed and floating rate debt,

principally through the use of interest rate swaps. We have

established interest rate risk limits that we closely monitor

by measuring interest rate sensitivities in our debt and

interest rate derivatives portfolios.

All our foreign-denominated long-term debt has been

swapped from fixed-rate or floating-rate foreign currencies

to fixed-rate U.S. dollars at issuance through cross-currency

swaps, removing interest rate risk and foreign currency

exchange risk associated with the underlying interest and

Maturity

Fair Value

2015 2016 2017 2018 2019 Thereafter Total 12/31/14

Interest Rate Derivatives

Interest Rate Swaps:

Receive Fixed/Pay Variable Notional

Amount Maturing $1,000 $ — $ 700 $1,500 $3,350 $ — $6,550 $157

Weighted-Average Variable Rate Payable1 2.4% 3.4% 4.2% 4.9% 4.2% —

Weighted-Average Fixed Rate Receivable 4.1% 4.2% 4.2% 4.5% 3.5% —

1 Interest payable based on current and implied forward rates for One, Three, or Six Month LIBOR plus a spread ranging between approximately 4 and 425 basis points.

In anticipation of other foreign currency-denominated

transactions, we often enter into foreign exchange forward

contracts to provide currency at a fixed rate. Our policy

is to measure the risk of adverse currency fluctuations

by calculating the potential dollar losses resulting from

changes in exchange rates that have a reasonable

probability of occurring. We cover the exposure that

results from changes that exceed acceptable amounts.

For the purpose of assessing specific risks, we use a

sensitivity analysis to determine the effects that market

risk exposures may have on the fair value of our financial

instruments and results of operations. To perform the

sensitivity analysis, we assess the risk of loss in fair values

from the effect of a hypothetical 10% depreciation of the

U.S. dollar against foreign currencies from the prevailing

foreign currency exchange rates, assuming no change in

interest rates. We had no foreign exchange forward

contracts outstanding at December 31, 2014.

Foreign Exchange Risk

We are exposed to foreign currency exchange risk through

our foreign affiliates and equity investments in foreign

companies. We do not hedge foreign currency translation

risk in the net assets and income we report from these

sources. However, we do hedge a portion of the exchange

risk involved in anticipation of highly probable foreign

currency-denominated transactions and cash flow streams,

such as those related to issuing foreign-denominated debt,

receiving dividends from foreign investments, and other

receipts and disbursements.

Through cross-currency swaps, all our foreign-denominated

debt has been swapped from fixed-rate or floating-rate

foreign currencies to fixed-rate U.S. dollars at issuance,

removing interest rate risk and foreign currency exchange

risk associated with the underlying interest and principal

payments. We expect gains or losses in our cross-currency

swaps to offset the losses and gains in the financial

instruments they hedge.