AT&T Wireless 2010 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2010 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

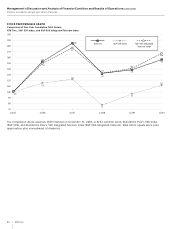

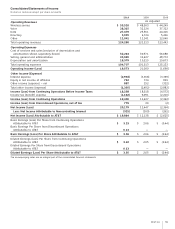

Management’s Discussion and Analysis of Financial Condition and Results of Operations (continued)

Dollars in millions except per share amounts

56 AT&T Inc.

Increasing competition in our wireline markets could

adversely affect wireline operating margins.

We expect competition in the telecommunications industry

to continue to intensify. We expect this competition will

continue to put pressure on pricing, margins and customer

retention. A number of our competitors that rely on alternative

technologies (e.g., wireless, cable and VoIP) and business

models (e.g., advertising-supported) are typically subject to

less (or no) regulation than our wireline and ATTC subsidiaries

and therefore are able to operate with lower costs.

These competitors also have cost advantages compared

to us, due in part to a nonunionized workforce, lower

employee benefits and fewer retirees (as most of the

competitors are relatively new companies). We believe such

advantages can be offset by continuing to increase the

efficiency of our operating systems and by improving

employee training and productivity; however, there can be no

guarantee that our efforts in these areas will be successful.

Continuing growth in our wireless services will depend on

continuing access to adequate spectrum, deployment of new

technology and offering attractive services to customers.

The wireless industry is undergoing rapid and significant

technological changes and a dramatic increase in usage, in

particular demand for and usage of data and other non-voice

services. We must continually invest in our wireless network

in order to continually improve our wireless service to meet

this increasing demand and remain competitive. Improvements

in our service depend on many factors, including continued

access to and deployment of adequate spectrum. We must

maintain and expand our network capacity and coverage

as well as the associated wireline network needed to

transport voice and data between cell sites. Network service

enhancements and product launches may not occur as

scheduled or at the cost expected due to many factors,

including delays in determining equipment and handset

operating standards, supplier delays, increases in network

equipment and handset component costs, regulatory permitting

delays for tower sites or enhancements or labor-related delays.

Deployment of new technology also may adversely affect the

performance of the network for existing services. If the FCC

does not allocate sufficient spectrum to allow the wireless

industry in general, and the company in particular, to increase

its capacity or if we cannot deploy the services customers

desire on a timely basis or at adequate cost while maintaining

network quality levels, then our ability to attract and retain

customers, and therefore maintain and improve our operating

margins, could be materially adversely affected.

Changes to federal, state and foreign government

regulations and decisions in regulatory proceedings could

materially adversely affect us.

Our wireline subsidiaries are subject to significant federal

and state regulation while many of our competitors are not.

In addition, our subsidiaries and affiliates operating outside

the U.S. are also subject to the jurisdiction of national and

supranational regulatory authorities in the market where

service is provided. Our wireless subsidiaries are regulated

to varying degrees by the FCC and some state and local

agencies. Adverse rulings by the FCC relating to broadband

issues could impede our ability to manage our networks and

recover costs and lessen incentives to invest in our networks.

The development of new technologies, such as IP-based

services, also has created or potentially could create

conflicting regulation between the FCC and various state

and local authorities, which may involve lengthy litigation

to resolve and may result in outcomes unfavorable to us.

In addition, increased public focus on potential global climate

changes has led to proposals at state, federal and foreign

government levels to increase regulation on various types

of emissions, including those generated by vehicles and

by facilities consuming large amounts of electricity.

Increasing competition in the wireless industry could

adversely affect our operating results.

We have multiple wireless competitors in each of our service

areas and compete for customers based principally on price,

service/device offerings, call quality, coverage area and

customer service. In addition, we are likely to experience

growing competition from providers offering services using

alternative wireless technologies and IP-based networks as

well as traditional wireline networks. We expect market

saturation to continue to cause the wireless industry’s

customer growth rate to moderate in comparison with

historical growth rates, leading to increased competition

for customers. We expect that the availability of additional

700 MHz spectrum could increase competition and the

effectiveness of existing competition. This competition will

continue to put pressure on pricing and margins as companies

compete for potential customers. Our ability to respond will

depend, among other things, on continued improvement in

network quality and customer service and effective marketing

of attractive products and services, and cost management.

These efforts will involve significant expenses and require

strategic management decisions on, and timely

implementation of, equipment choices and deployment,

and service offerings.