TCF Bank 2013 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2013 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

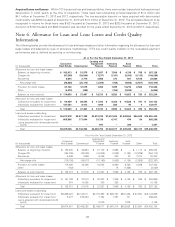

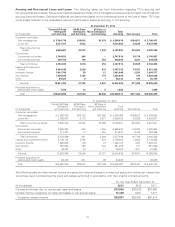

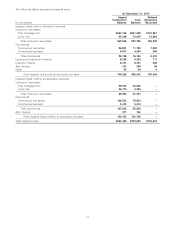

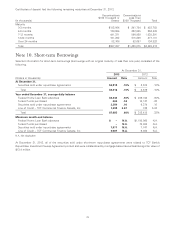

The table below summarizes TDR loans that defaulted during the years ended December 31, 2013 and 2012, which were

modified within one year of the beginning of the respective reporting period. TCF considers a loan to have defaulted when it

becomes 90 or more days delinquent under the modified terms, has been transferred to non-accrual status subsequent to the

modification or has been transferred to other real estate owned.

Year Ended December 31,

2013 2012

Number Number

(Dollars in thousands) of Loans Loan Balance(1) of Loans Loan Balance(1)

Consumer real estate:

First mortgage lien 85 $ 12,511 62 $ 10,007

Junior lien 50 2,479 25 1,221

Total consumer real estate 135 14,990 87 11,228

Commercial real estate 7 5,561 21 41,027

Leasing and equipment finance 2 268 ––

Auto finance 659––

Other 11––

Total defaulted modified loans 151 $ 20,878 108 $ 52,255

Total loans modified in the applicable period 1,865 $374,761 2,383 $575,014

Defaulted modified loans as a percent of total loans modified

in the applicable period 8.1% 5.6% 4.5% 9.1%

(1) The loan balances presented are not materially different than the pre-modification loan balances as TCF’s loan modifications generally do not

forgive principal amounts.

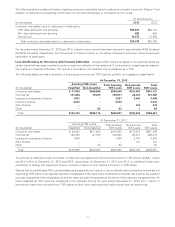

Consumer real estate TDR loans are evaluated separately in TCF’s allowance methodology. Impairment is generally based upon

the present value of the expected future cash flows or the fair value of the collateral less selling expenses for collateral

dependent loans. The allowance on accruing consumer real estate TDR loans was $103.3 million, or 20.4% of the outstanding

balance, at December 31, 2013 and $82.3 million, or 17.2% of the outstanding balance, at December 31, 2012. For consumer

real estate TDR loans, TCF utilized average remaining re-default rates ranging from 6% to 25% in 2013, and 10% to 25% in 2012,

depending on modification type, in determining impairment, which is consistent with actual experience.

Generally consumer real estate loans remain on accruing status upon modification if they are less than 90 days past due and

payment in full under the modified loan terms is expected based on a current credit evaluation and historical payment

performance. In addition, consumer real estate junior lien loans are placed on non-accrual status and charged-off to the estimated

fair value when the junior lien loan is 30 days or more past due and when TCF has evidence that the related third-party first

mortgage lien is 90 days or more past due or foreclosure action has been initiated. Loans are placed on non-accrual status and

reported as non-accrual until there is sustained repayment performance for six consecutive payments, except for loans

discharged in Chapter 7 bankruptcy that are not reaffirmed, which remain on non-accrual status for the remainder of the term of

the loan. All eligible loans are re-aged to current delinquency status upon modification.

Commercial TDR loans are individually evaluated for impairment based upon the present value of the expected future cash flows

or for collateral dependent loans at the fair value of collateral, less selling expense if repayment or satisfaction of the loans is

expected to be dependent on the sale of the collateral. Non-accrual commercial loans are charged-off to the estimated fair value

of underlying collateral, less estimated selling costs; however, if payment or satisfaction of the loan is dependent on the

operation, rather than the sale, of the collateral, the impairment does not include selling costs. The allowance on accruing

commercial TDR loans was $6.3 million, or 5.2% of the outstanding balance, at December 31, 2013 and $1.5 million, or 1% of the

outstanding balance, at December 31, 2012.

Impaired Loans TCF considers impaired loans to include non-accrual commercial loans, non-accrual equipment finance loans

and non-accrual inventory finance loans, as well as all TDR loans. Non-accrual impaired loans, including non-accrual TDR loans,

are included in non-accrual loans and leases within the previous tables. Accruing TDR loans have been disclosed by delinquency

status within the previous tables of accruing and non-accrual loans and leases. In the following tables, the loan balance of

impaired loans represents the amount recorded within loans and leases on the Consolidated Statements of Financial Condition,

whereas the unpaid contractual balance represents the balances legally owed by the borrowers.

73