TCF Bank 2013 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2013 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

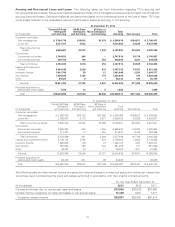

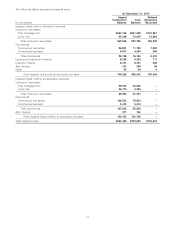

December 31, 2013, interest-only strips and contractual recourse liabilities related to sales of auto loans totaled $64.9 million and

$1.1 million, respectively. At December 31, 2012, interest-only strips and contractual recourse liabilities related to sales of auto

loans totaled $46.7 million and $3.6 million, respectively. TCF recorded impairment charges related to auto finance interest-only

strips of $5.4 million and $458 thousand during the years ended December 31, 2013 and 2012, respectively. These impairments

were related to higher prepayments than originally assumed. No servicing assets or liabilities related to consumer auto loans

were recorded within TCF’s Consolidated Statements of Financial Condition, as the contractual servicing fees are adequate to

compensate TCF for its servicing responsibilities. TCF’s auto loan managed portfolio, which includes portfolio loans, loans held

for sale, and loans sold and serviced for others, totaled $2.4 billion and $1.3 billion at December 31, 2013 and 2012, respectively.

During the years ended December 31, 2013 and 2012, TCF sold $763.1 million and $161.8 million, respectively, of consumer real

estate loans, with limited representations, indemnifications, and limited credit guarantees, received cash of $767.3 million and

$167.2 million, respectively, and recognized net gains of $21.7 million and $5.4 million, respectively. Related to these sales, TCF

retained interest-only strips of $22.2 million and $1.1 million for the years ended December 31, 2013 and 2012, respectively. At

December 31, 2013, interest-only strips and contractual recourse liabilities related to sales of consumer real estate loans totaled

$19.6 million and $563 thousand, respectively. TCF recorded impairment charges related to consumer real estate interest-only

strips of $466 thousand during the year ended December 31, 2013 and had no impairment charges recorded during the year

ended December 31, 2012. No servicing assets or liabilities related to consumer real estate loans were recorded within TCF’s

Consolidated Statements of Financial Condition, as the contractual servicing fees are adequate to compensate TCF for its

servicing responsibilities based on the amount demanded by the marketplace. TCF’s consumer real estate loan managed

portfolio, which includes portfolio loans, loans held for sale, and loans sold and serviced for others, totaled $7 billion and

$6.7 billion at December 31, 2013 and 2012, respectively.

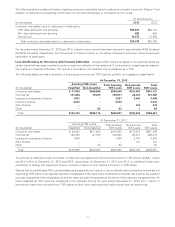

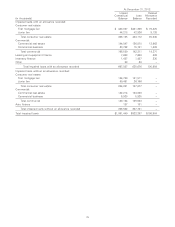

From time to time, TCF sells leasing and equipment finance loans and minimum lease payments to third-party financial

institutions at fixed rates. During the years ended December 31, 2013 and 2012, TCF sold $60.3 million and $102.4 million,

respectively, of loans and minimum lease payment receivables, received cash of $62.1 million and $105.9 million, respectively,

and recognized a net gain of $487 thousand and $2.1 million, respectively. Related to these sales, TCF had servicing liabilities of

$1.3 million for both the years December 31, 2013 and 2012. At December 31, 2013 and 2012, TCF had total servicing liabilities

related to leasing and equipment finance of $1.7 million and $1.2 million, respectively. At December 31, 2013 and 2012, TCF had

lease residuals related to sales of outstanding minimum lease payments receivable of $15.2 million included in loans and leases

and $14.8 million included in other assets, respectively. TCF’s leasing and equipment finance loan managed portfolio, which

includes portfolio loans, loans held for sale, and loans sold and serviced for others, totaled $3.6 billion and $3.4 billion at

December 31, 2013 and 2012, respectively.

During the year ended December 31, 2013, TCF sold $86.5 million of commercial loans and recognized a net gain of $1.6 million.

There were no material sales of commercial loans during the year ended 2012. There were no servicing liabilities related to these

sales.

TCF’s agreements to sell consumer real estate and auto loans typically contain certain representations and warranties regarding

the loans sold. These representations and warranties generally relate to, among other things, the ownership of the loan, the

validity, priority and perfection of the lien securing the loan, accuracy of information supplied to the buyer, the loan’s compliance

with the criteria set forth in the agreement, payment delinquency, and compliance with applicable laws and regulations. TCF may

be required to repurchase loans in the event of an unremedied breach of these representations or warranties. During the years

ended December 31, 2013 and 2012, losses related to repurchases pursuant to such representations and warranties were

immaterial as the majority of such repurchases were of consumer auto loans where TCF typically has contractual agreements

with the automobile dealership that originated the loan requiring the dealer to repurchase such contracts from TCF.

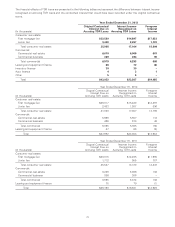

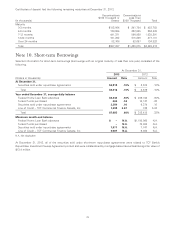

Future minimum lease payments receivable for direct financing, sales-type leases and operating leases as of December 31, 2013

are as follows:

(In thousands)

2014 $ 711,400

2015 509,988

2016 351,558

2017 205,442

2018 90,178

Thereafter 28,759

Total $1,897,325

68