TCF Bank 2013 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2013 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

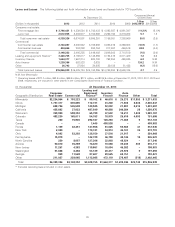

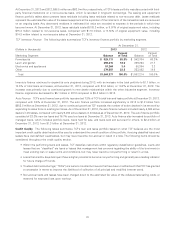

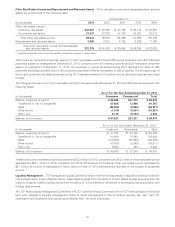

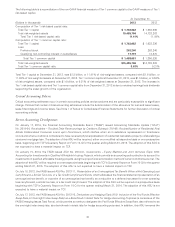

Changes in the amount of non-accrual loans and leases for the years ended December 31, 2013 and 2012 are summarized in the

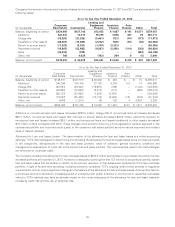

following tables.

At or for the Year Ended December 31, 2013

Leasing and

Consumer Equipment Inventory Auto

(In thousands) Real Estate Commercial Finance Finance Finance Other Total

Balance, beginning of period $234,900 $127,746 $13,652 $ 1,487 $ 101 $1,571 $379,457

Additions 222,443 13,315 19,219 7,608 497 29 263,111

Charge-offs (38,283) (27,325) (5,461) (721) (10) (173) (71,973)

Transfers to other assets (66,267) (13,885) (2,252) (526) (10) (56) (82,996)

Return to accrual status (71,229) (9,057) (1,748) (3,321) – – (85,355)

Payments received (19,865) (53,985) (9,267) (2,292) (114) (503) (86,026)

Sales (43,434) (309) – – – (453) (44,196)

Other, net 768 4,039 (102) 294 6 (5) 5,000

Balance, end of period $219,033 $ 40,539 $14,041 $ 2,529 $ 470 $ 410 $277,022

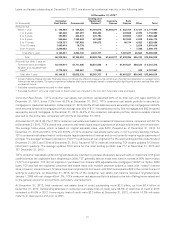

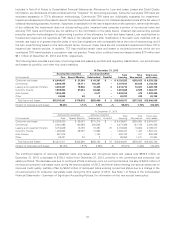

At or for the Year Ended December 31, 2012

Leasing and

Consumer Equipment Inventory Auto

(In thousands) Real Estate Commercial Finance Finance Finance Other Total

Balance, beginning of period $149,371 $127,519 $ 20,583 $ 823 $ – $ 15 $ 298,311

Additions 340,359 120,155 27,138 8,784 110 14 496,560

Charge-offs (62,591) (40,502) (19,667) (736) – (1,188) (124,684)

Transfers to other assets (82,632) (15,044) (2,915) (817) – (605) (102,013)

Return to accrual status (96,137) (27,692) (1,308) (3,867) – – (129,004)

Payments received (12,827) (35,480) (10,170) (2,885) (13) (572) (61,947)

Other, net (643) (1,210) (9) 185 4 3,907 2,234

Balance, end of period $234,900 $127,746 $ 13,652 $ 1,487 $101 $ 1,571 $ 379,457

Additions to non-accrual loans and leases decreased $233.4 million, charge-offs of non-accrual loans and leases decreased

$52.7 million, non-accrual loans and leases that returned to accrual status decreased $43.6 million, payments received on

non-accrual loan and leases increased $24.1 million and non-accrual loans and leases transferred to other assets decreased

$19 million in 2013 compared with 2012. These changes were primarily driven by a more aggressive workout approach in the

commercial portfolio and improved credit quality in the consumer real estate portfolio as home values improved and incident

rates of default declined.

Allowance for Loan and Lease Losses The determination of the allowance for loan and lease losses is a critical accounting

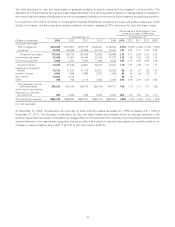

estimate. TCF’s methodologies for determining and allocating the allowance for loan and lease losses focus on historical trends

in net charge-offs, delinquencies in the loan and lease portfolio, value of collateral, general economic conditions and

management’s assessment of credit risk in the current loan and lease portfolio. The various factors used in the methodologies

are reviewed on a periodic basis.

The Company considers the allowance for loan and lease losses of $252.2 million appropriate to cover losses incurred in the loan

and lease portfolios at December 31, 2013. However, no assurance can be given that TCF will not, in any particular period, sustain

loan and lease losses that are sizable in relation to the amount reserved, or that subsequent evaluations of the loan and lease

portfolio, in light of factors then prevailing, including economic conditions, TCF’s ongoing credit review process or regulatory

requirements, will not require significant changes in the balance of the allowance for loan and lease losses. Among other factors,

a continued economic slowdown, increasing levels of unemployment and/or a decline in commercial or residential real estate

values in TCF’s markets may have an adverse impact on the current adequacy of the allowance for loan and lease losses by

increasing credit risk and the risk of potential loss.

39