TCF Bank 2013 Annual Report Download - page 23

Download and view the complete annual report

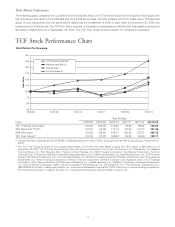

Please find page 23 of the 2013 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

abusive in connection with any consumer financial product or service. The CFPB has examination and enforcement authority

over all banks and savings institutions with more than $10 billion in assets, including TCF Bank.

Additionally, the Dodd-Frank Act:

• Directed the Federal Reserve to issue rules limiting debit-card interchange fees for larger banks;

• Removed, after a three-year phase-in period which began January 1, 2013, trust preferred securities as a permitted

component of a bank holding company’s Tier 1 Capital;

• Eliminated federal preemption for subsidiaries of national banks and federal savings associations;

• Provided for new disclosure and other requirements relating to executive compensation and corporate governance,

including requiring an advisory vote on executive compensation (‘‘Say on Pay’’);

• Provided for mortgage reform addressing a customer’s ability to repay, restricted variable-rate lending by requiring the

ability to repay to be determined for variable-rate loans by using the maximum rate that will apply during the first five years

of a variable rate loan, and made more loans subject to requirements for higher cost loans, new disclosures and certain

other restrictions;

• Permanently increased the maximum amount of deposit insurance for banks, savings institutions and credit unions to

$250,000 per depositor, retroactive to January 1, 2008; and allowed depository institutions to pay interest on business

checking accounts, and;

• Required publicly-traded bank holding companies with assets of $10 billion or more to establish a risk committee of the

Board of Directors responsible for enterprise-wide risk management practices.

Taxation

Federal Taxation TCF’s federal income tax returns are open and subject to examination for 2012 and later tax return years.

State Taxation TCF and/or its subsidiaries currently file tax returns in all states which impose corporate income and franchise

taxes and local tax returns in certain cities and other taxing jurisdictions. The methods of filing, and the methods for calculating

taxable and apportionable income, vary depending upon the laws of the taxing jurisdiction. See ‘‘Item 1A. Risk Factors’’.

See ‘‘Item 7. Management’s Discussion and Analysis – Consolidated Income Statement Analysis – Income Taxes’’ and Notes 1

and 12 of Notes to Consolidated Financial Statements for additional information regarding TCF’s income taxes.

Available Information

TCF’s website, http://ir.tcfbank.com, includes free access to Company news releases, investor presentations, conference calls

to discuss published financial results, TCF’s Annual Report and periodic filings required by the United States Securities and

Exchange Commission (‘‘SEC’’), including annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on

Form 8-K and amendments to those reports, as soon as reasonably practicable after electronic filing of such material with, or

furnishing it to, the SEC. TCF’s Compensation, Nominating, and Corporate Governance Committee and Audit Committee

charters, Corporate Governance Guidelines, Codes of Ethics and changes to Codes of Ethics and information on all of TCF’s

securities are also available on this website. Stockholders may request these documents in print free of charge by contacting the

Corporate Secretary at TCF Financial Corporation, 200 Lake Street East, Mail Code EX0-01-G, Wayzata, MN 55391-1693.

Item 1A. Risk Factors

Various risks and uncertainties may affect TCF’s business. Any of the risks described below or elsewhere in this Annual Report

on Form 10-K or TCF’s other SEC filings may have a material impact on TCF’s financial condition or results of operations.

TCF’s earnings are significantly affected by general economic and political conditions.

TCF’s operations and profitability are impacted by general business and economic conditions in the local markets in which TCF

operates, the U.S. generally and abroad. Economic conditions have a significant impact on the demand for TCF’s products and

services, as well as the ability of its customers to repay loans, the value of the collateral securing loans, the ability of TCF to sell

loans, the stability of its deposit funding sources and sales revenue at the end of contractual lease terms. A significant decline in

general economic conditions caused by inflation, recession, unemployment, changes in securities markets, changes in housing

market prices or other factors could impact economic conditions and, in turn, could have a material adverse effect on TCF’s

financial condition and results of operations.

7