Radio Shack 2003 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2003 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

RADIOSHACK 2003 Annual Report

28

2003, and made no material adjustments to our consolidated

financial statements as a result of this adoption.

In November 2002, the FASB issued Interpretation No.45,

“Guarantor’s Accounting and Disclosure Requirements for

Guarantees, Including Guarantees of Indebtedness of

Others.” FIN 45 is effective for guarantees issued or modified

after December 31, 2002.The disclosure requirements were

effective for certain guarantees existing at December 31,

2002, and expand the disclosures required by a guarantor

about its obligations under a guarantee. FIN 45 also

requires that we recognize guarantees entered into or

modified after December 31, 2002, as a liability for the fair

value of the obligation undertaken in the issuance of the

guarantee.We adopted FIN 45 on January 1, 2003, its

effective date, and, aside from the required disclosure pro-

visions, made no material adjustments to our consolidated

financial statements as a result of this adoption.

In January 2003, the FASB issued Interpretation 46,

“Consolidation of Variable Interest Entities – An Interpretation

of ARB No.51.” FIN 46 is intended to clarify the application

of ARB No.51,“Consolidated Financial Statements,”to cer-

tain entities in which equity investors do not have the

characteristics of a controlling financial interest or do not

have sufficient equity at risk for the entity to finance its

activities without additional subordinated financial sup-

port. For those entities, a controlling financial interest

cannot be identified based on an evaluation of voting inter-

ests and may be achieved through arrangements that do

not involve voting interests.The consolidation requirement

of FIN 46 is effective immediately to variable interests in

variable interest entities (“VIEs”) created or obtained after

January 31, 2003. FIN 46 also sets forth certain disclosures

regarding interests in VIEs that are deemed significant, even

if consolidation is not required. In December 2003, the FASB

issued FIN 46 (revised December 2003),“Consolidation of

Variable Interest Entities” (FIN 46R), which delayed the effec-

tive date of the application to us of FIN 46 to non-special

purpose VIEs acquired or created before February 1, 2003,

to the interim period ending on March 31, 2004, and pro-

vided additional technical clarifications to implementation

issues.We have determined that FIN 46 does not apply to

our dealer/franchise outlets and we do not expect to make

material adjustments to our consolidated financial state-

ments as a result of the adoption of this Interpretation.

In November 2002, the EITF reached a consensus on Issue

No.02-16,“Accounting for Consideration Received from a

Vendor by a Customer (Including a Reseller of the Vendor’s

Products).” EITF 02-16 provides guidance on how cash

consideration received by a customer from a vendor should

be classified in the customer’s statement of income. EITF

02-16 is effective prospectively for new arrangements,includ-

ing modifications of existing arrangements, entered into

after December 31, 2002.We adopted EITF 02-16 effective

January 1, 2003, and made no material adjustments to our

consolidated financial statements as a result of this adoption.

In November 2003, the EITF reached a consensus on Issue

No. 03-10,“Application of EITF Issue No. 02-16,‘Accounting

by a Customer (Including a Reseller) for Certain Consideration

Received from a Vendor,’ by Resellers to Sales Incentives

Offered to Consumers by Manufacturers.”EITF 03-10 provides

guidance on how cash consideration received by a cus-

tomer from a vendor should be classified in the customer’s

statement of income. EITF 03-10 is effective prospectively

for new arrangements, including modification of existing

arrangements, entered into after December 31, 2003.We

adopted EITF 03-10 effective January 1, 2004, and made no

material adjustments to our consolidated financial state-

ments as a result of this adoption.

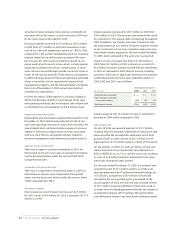

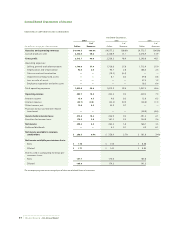

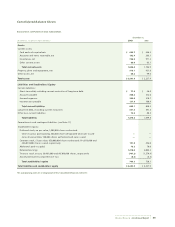

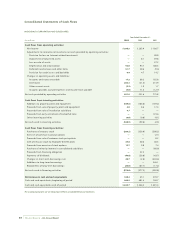

Cash Flow and Liquidity

A summary of cash flows from operating, investing and

financing activities is outlined in the table below.

Year Ended December 31,

(In millions)2003 2002 2001

Operating activities $ 651.9 $ 521.6 $ 775.8

Investing activities (188.9) (99.0) (2.3)

Financing activities (274.8) (377.5) (502.8)

In 2003, cash flows provided by operating activities was

$651.9 million, compared to $521.6 million and $775.8 mil-

lion in 2002 and 2001, respectively.

During the year ended December 31, 2003, changes in

accounts receivable, consisting primarily of amounts due

from our various vendors and third-party service providers,

provided $17.2 million in cash, compared to $68.2 million in

the prior year. Cash provided by accounts receivable in

2003 and 2002 was the result of reductions of vendor

and service provider receivables and dealer/franchise

receivables, due to increased collections and lower sales of

satellite television hardware.

During the year ended December 31, 2003, changes in

inventory provided $202.3 million in cash, compared to a

$21.4 million cash usage during 2002.The decrease in

inventory since December 31, 2002, was primarily the result

of supply chain initiatives, including a greater focus on

reducing weeks-of-supply.