Radio Shack 2003 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2003 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

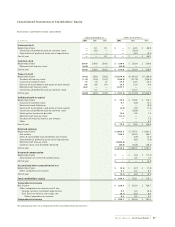

RADIOSHACK 2003 Annual Report 27

Net Interest Expense

Interest expense, net of interest income, was $34.4 million

for 2002 versus $37.8 million for 2001.

Interest expense decreased to $43.4 million in 2002 from

$50.8 million in 2001, primarily as a result of a reduction in

the average debt outstanding throughout 2002. In addi-

tion, our interest rate swap instruments also lowered overall

interest expense for the year ended December 31, 2002,

when compared to the same prior year period. Interest

income decreased almost 31% to $9.0 million in 2002 from

$13.0 million in 2001, due primarily to CompUSA’s early

payment of its note to us in June 2001, which eliminated

the associated interest income.

Other Income, Net

In the second quarter of 2002, we received payments and

recorded income of $27.7 million in partial settlement of

amounts owed to us under a tax sharing agreement that

was the subject of an arbitration which commenced in July

1999 and was styled Tandy Corporation and T.E. Electronics,

L.P. vs. O’Sullivan.The arbitration ruling requires O’Sullivan

to comply with the tax sharing agreement that was entered

into by the parties at the time of O’Sullivan’s initial public

offering.

During the second half of 2002, we received two payments

totaling $6.2 million relating to quarterly payments under

the tax sharing agreement with O’Sullivan.

Provision for Loss on Internet-Related Investment

During the second quarter of 2000, we made a $30.0 mil-

lion investment in Digital:Convergence Corporation (“DC”),

a privately-held Internet technology company. In the first

quarter of 2001, we concluded that our investment had

experienced a decline in value that, in our opinion, was

other than temporary.This conclusion was based on DC’s

inability to secure sufficient additional funding or to com-

plete an initial public offering. As such, we recorded a loss

provision equal to our initial investment. DC subsequently

filed for bankruptcy on March 22, 2002.

Provision for Income Taxes

Our provision for income taxes reflects an effective income

tax rate of 38.0% for 2002 and 42.8% for 2001.The decrease

in the effective tax rate in 2002 when compared to 2001

was the result of the 2001 impairment of RSIS goodwill,

which was not deductible for tax purposes and caused the

increased effective tax rate in 2001.

Recently Issued Accounting Pronouncements

In June 2001, the Financial Accounting Standards Board

issued SFAS No. 143,“Accounting for Asset Retirement

Obligations,”which is effective for fiscal years beginning

after June 15, 2002. SFAS No. 143 establishes financial

accounting and reporting standards for obligations associ-

ated with the retirement of tangible long-lived assets and

the associated asset retirement costs.We adopted SFAS No.

143 effective January 1, 2003, and made no material adjust-

ments to our consolidated financial statements as a result

of this adoption.

In June 2002, the FASB issued SFAS No. 146,“Accounting for

Costs Associated with Exit or Disposal Activities.” SFAS No.

146 addresses significant issues relating to the recognition,

measurement, and reporting of costs associated with exit

and disposal activities, including restructuring activities,

and nullifies the guidance in Emerging Issues Task Force

Issue No. 94-3,“Liability Recognition for Certain Employee

Termination Benefits and Other Costs to Exit an Activity

(Including Certain Costs Incurred in a Restructuring).”The

provisions of SFAS No. 146 are effective for exit or disposal

activities initiated after December 31, 2002. Retroactive

application of SFAS No. 146 is prohibited and, accordingly,

liabilities recognized prior to the initial application of SFAS

No.146 should continue to be accounted for in accordance

with EITF 94-3 or other applicable preexisting guidance.We

adopted SFAS No.146 effective January 1, 2003, and made

no material adjustments to our consolidated financial state-

ments as a result of this adoption.

In April 2003, the FASB issued SFAS No. 149,“Amendment of

Statement 133 on Derivative Instruments and Hedging

Activities.”SFAS No. 149 amends and clarifies accounting

for derivative instruments, including certain derivative

instruments embedded in other contracts, and for hedging

activities under SFAS No. 133. SFAS No. 149 is effective for

contracts entered into or modified after June 30, 2003, for

hedging relationships designated after June 30, 2003, and

to certain preexisting contracts.We adopted SFAS No. 149

effective July 1, 2003, and made no material adjustments to

our consolidated financial statements as a result of this

adoption.

In May 2003, the FASB issued SFAS No. 150,“Accounting for

Certain Financial Instruments with Characteristics of Both

Liabilities and Equity,”which is effective for financial instru-

ments entered into or modified after May 31, 2003. SFAS

No.150 establishes financial accounting and reporting

standards for how an issuer classifies and measures certain

financial instruments with characteristics of both liabilities

and equities.We adopted SFAS No. 150 effective June 1,