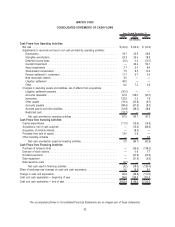

Memorex 2009 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2009 Memorex annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

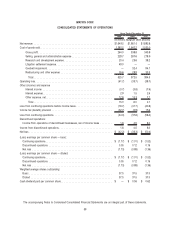

|

|

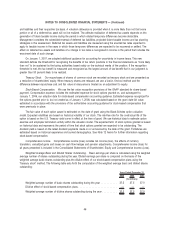

Inventories. Inventories are valued at the lower of cost or market, with cost generally determined on a first-in, first-

out basis. We provide estimated inventory write-downs for excess, slow-moving and obsolete inventory as well as inventory

with a carrying value in excess of net realizable value.

Derivative Financial Instruments. We follow GAAP guidance for accounting for derivative instruments and hedging

activities, which requires that all derivatives, including foreign currency exchange contracts, be recognized on the balance

sheet at fair value. Derivatives that are not hedges must be recorded at fair value through operations. If a derivative is a

hedge, depending on the nature of the hedge, changes in the fair value of the derivative are either offset against the

change in fair value of the underlying assets or liabilities through operations or recognized in accumulated other

comprehensive loss in shareholders’ equity until the underlying hedged item is recognized in operations. These gains and

losses are generally recognized as an adjustment to cost of goods sold for inventory-related hedge transactions, or as

adjustments to foreign currency transaction gains or losses included in non-operating expenses for foreign denominated

payables and receivables-related hedge transactions. Cash flows attributable to these financial instruments are included

with cash flows of the associated hedged items. The ineffective portion of a derivative’s change in fair value is immediately

recognized in operations.

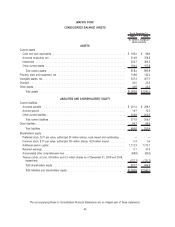

Property, Plant and Equipment. Property, plant and equipment, including leasehold and other improvements that

extend an asset’s useful life or productive capabilities, are recorded at cost. Maintenance and repairs are expensed as

incurred. The cost and related accumulated depreciation of assets sold or otherwise disposed are removed from the

related accounts and the gains or losses are reflected in the results of operations.

Property, plant and equipment are generally depreciated on a straight-line basis over their estimated useful lives. The

estimated depreciable lives range from 10 to 20 years for buildings and 5 to 10 years for machinery and equipment.

Leasehold and other improvements are amortized over the lesser of the remaining life of the lease or the estimated useful

life of the improvement.

Intangible Assets. Intangible assets include trade names, customer relationships and other intangible assets

acquired in business combinations. Intangible assets are amortized using methods that approximate the benefit provided

by utilization of the assets.

We capitalize costs of software developed or obtained for internal use, once the preliminary project stage has been

completed, management commits to funding the project and it is probable that the project will be completed and the

software will be used to perform the function intended. Capitalized costs include only (1) external direct costs of materials

and services consumed in developing or obtaining internal-use software, (2) payroll and payroll-related costs for employees

who are directly associated with and who devote time to the internal-use software project and (3) interest costs incurred,

when material, while developing internal-use software. Capitalization of costs ceases when the project is substantially

complete and ready for its intended use.

Goodwill. Goodwill is the excess of the cost of an acquired entity over the amounts assigned to assets acquired

and liabilities assumed in a business combination. Goodwill is not amortized. In accordance with GAAP guidance for

goodwill and other intangible assets, we evaluate the carrying value of goodwill during the fourth quarter of each year and

between annual evaluations if events occur or circumstances change that would indicate a possible impairment.

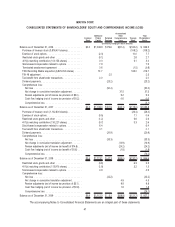

In evaluating whether goodwill was impaired, we compared the fair value of the reporting units to which goodwill is

assigned to their carrying value (Step 1 of the impairment test). In calculating fair value, we used a weighting of the

valuations calculated using a market approach and the income approach. The basis of this weighting is due to the fact

that the income approach is tailored to the circumstances of the business, and the market approach is completed as a

secondary test to ensure that the results of the income approach are reasonable and in line with comparable companies in

the industry. The income approach is a valuation technique under which we estimate future cash flows using the reporting

units’ financial forecasts. Future estimated cash flows are discounted to their present value to calculate fair value. The

market approach establishes fair value by comparing our company to other publicly traded guideline companies or by

analysis of actual transactions of similar businesses or assets sold. In determining the fair value of reporting units, we

weighted values under the income approach 75 percent and values determined from market comparables 25 percent. The

summation of our reporting units’ fair values is compared and reconciled to our market capitalization as of the date of our

44

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)