Foot Locker 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

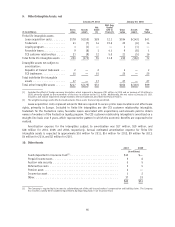

11. Accrued and Other Liabilities 2010 2009

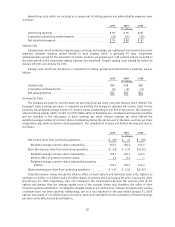

(in millions)

Incentive bonuses ........................................ $ 48 $ 9

Other payroll and payroll related costs, excluding taxes ................ 43 46

Taxes other than income taxes ................................ 37 41

Customer deposits

(1)

....................................... 29 29

Current deferred tax liabilities ................................ 20 5

Property and equipment .................................... 19 13

Income taxes payable ...................................... 8 7

Pension and postretirement benefits ............................ 4 5

Sales return reserve ....................................... 4 3

Income taxes ........................................... 1 10

Reserve for discontinued operations ............................ 1 2

Other operating costs ...................................... 52 48

$266 $218

(1) Customer deposits include unredeemed gift cards and certificates, merchandise credits, and deferred revenue related to undelivered

merchandise, including layaway sales.

12. Revolving Credit Facility

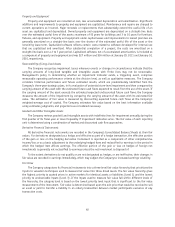

In 2009, the Company entered into a credit agreement (the ‘‘2009 Credit Agreement’’) with its banks,

providing for a $200 million asset-based revolving credit facility maturing on March 20, 2013. The 2009 Credit

Agreement also provides for an incremental facility of up to $100 million under certain circumstances. The 2009

Credit Agreement provides for a security interest in certain of the Company’s domestic assets, including certain

inventory assets. The Company is not required to comply with any financial covenants as long as there are no

outstanding borrowings. If the Company is borrowing, then it may not make Restricted Payments, such as

dividends or share repurchases, unless there is at least $50 million of Excess Availability (as defined in the 2009

Credit Agreement), and the Company’s projected fixed charge coverage ratio, which is a Non-GAAP financial ratio

determined pursuant to the 2009 Credit Agreement designed as a measure of the Company’s ability to meet

current and future obligations (Consolidated EBITDA less capital expenditures less cash taxes divided by Debt

Service Charges and Restricted Payments), is at least 1.1 to 1.0. The Company’s management does not currently

expect to borrow under the facility in 2011.

At January 29, 2011, the Company had unused domestic lines of credit of $199 million pursuant to the 2009

Credit Agreement, of which $1 million was committed to support standby letters of credit. The letters of credit are

primarily used for insurance programs.

Deferred financing fees are amortized over the life of the facility on a straight-line basis, which is

comparable to the interest method. The unamortized balance at January 29, 2011 is $4 million. Interest is based

on the LIBOR rate in effect at the time of the borrowing plus a 3.25 to 3.75 percent applicable margin, as defined

in the 2009 Credit Agreement. The quarterly facility fees paid on the unused portion were 0.75 percent for 2010,

and ranged from 0.40 percent to 0.75 percent for 2009. There were no short-term borrowings during 2010 or

2009. Interest expense, including facility fees, related to the revolving credit facility was $4 million and

$3 million in 2010 and 2009, respectively.

13. Long-Term Debt

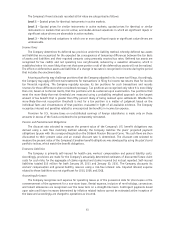

The Company’s long-term debt reflects the Company’s 8.50 percent debentures payable in 2022, and was

$137 million and $138 million for the years ended January 29, 2011 and January 30, 2010, respectively. The

Company has historically employed various interest rate swaps to minimize its exposure to interest rate

fluctuations. In 2009, the Company terminated the interest rate swaps for a gain of $19 million. The gain is being

amortized as part of interest expense over the remaining term of the debt, using the effective-yield method. This

gain amortization totaled $1 million in each of 2010 and 2009. Excluding the unamortized gain of the interest

rate swaps, the principal outstanding is $120 million.

Interest expense related to long-term debt, including the effect of the interest rate swaps and the

amortization of the associated debt issuance costs, was $9 million in each of 2010, 2009, and 2008.

47