Foot Locker 2010 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2010 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

Capital Structure

Credit Agreement

On March 20, 2009, the Company entered into a new credit agreement (the ‘‘2009 Credit Agreement’’) with its

banks, providing for a $200 million asset-based revolving credit facility maturing on March 20, 2013. The 2009

Credit Agreement also provides for an incremental facility of up to $100 million under certain circumstances. The

2009 Credit Agreement provides for a security interest in certain of the Company’s domestic assets, including

certain inventory assets. The Company is not required to comply with any financial covenants as long as there are

no outstanding borrowings. If the Company is borrowing, then it may not make Restricted Payments, such as

dividends or share repurchases, unless there is at least $50 million of Excess Availability (as defined in the 2009

Credit Agreement), and the Company’s projected fixed charge coverage ratio, which is a Non-GAAP financial ratio

determined pursuant to the 2009 Credit Agreement designed as a measure of the Company’s ability to meet

current and future obligations (Consolidated EBITDA less capital expenditures less cash taxes divided by Debt

Service Charges and Restricted Payments), is at least 1.1 to 1.0. The Company’s management does not currently

expect to borrow under the facility in 2011.

Credit Rating

As of March 28, 2011, the Company’s corporate credit ratings from Standard & Poor’s and Moody’s Investors

Service are BB- and Ba3, respectively. Additionally, Moody’s Investors Service has rated the Company’s senior

unsecured notes B1.

Debt Capitalization and Equity

For purposes of calculating debt to total capitalization, the Company includes the present value of operating

lease commitments in total net debt. Total net debt including the present value of operating leases is considered

a non-GAAP financial measure. The present value of operating leases is discounted using various interest rates

ranging from 4 percent to 15 percent, which represent the Company’s incremental borrowing rate at inception of

the lease. Operating leases are the primary financing vehicle used to fund store expansion and, therefore, we

believe that the inclusion of the present value of operating leases in total debt is useful to our investors, credit

constituencies, and rating agencies.

The following table sets forth the components of the Company’s capitalization, both with and without the

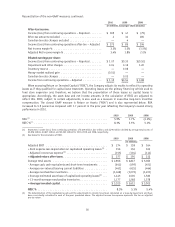

present value of operating leases:

2010 2009

(in millions)

Long-term debt ......................................... $ 137 $ 138

Present value of operating leases ............................. 1,852 1,923

Total debt including the present value of operating leases ........... 1,989 2,061

Less:

Cash and cash equivalents .................................. 696 582

Short-term investments ................................... — 7

Total net debt including the present value of operating leases ........ 1,293 1,472

Shareholders’ equity ..................................... 2,025 1,948

Total capitalization ...................................... $3,318 $3,420

Total net debt capitalization percent .......................... —% —%

Total net debt capitalization percent including the present value of

operating leases ...................................... 39.0% 43.0%

The Company increased cash, cash equivalents, and short-term investments by $107 million during 2010

reflecting strong cash flow generation from operating activities. Additionally, the present value of the operating

leases decreased by $71 million as compared with the prior year. This decrease represents the effect of the store

closures, offset, in part, by lease renewals and the effect of foreign currency translation. Including the present

value of operating leases, the Company’s net debt capitalization percent decreased 400 basis points in 2010.

24