Foot Locker 2010 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2010 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

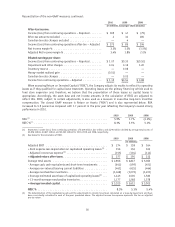

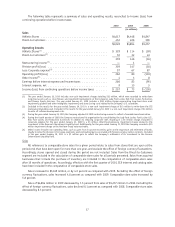

Critical Accounting Policies

Management’s responsibility for integrity and objectivity in the preparation and presentation of the

Company’s financial statements requires diligent application of appropriate accounting policies. Generally, the

Company’s accounting policies and methods are those specifically required by U.S. generally accepted accounting

principles. Included in the Summary of Significant Accounting Policies note in ‘‘Item 8. Consolidated Financial

Statements and Supplementary Data’’ is a summary of the Company’s most significant accounting policies. In

some cases, management is required to calculate amounts based on estimates for matters that are inherently

uncertain. The Company believes the following to be the most critical of those accounting policies that

necessitate subjective judgments.

Merchandise Inventories

Merchandise inventories for the Company’s Athletic Stores are valued at the lower of cost or market using

the retail inventory method (‘‘RIM’’). The RIM is commonly used by retail companies to value inventories at cost

and calculate gross margins due to its practicality. Under the retail method, cost is determined by applying a

cost-to-retail percentage across groupings of similar items, known as departments. The cost-to-retail percentage

is applied to ending inventory at its current owned retail valuation to determine the cost of ending inventory on

a department basis. The RIM is a system of averages that requires management’s estimates and assumptions

regarding markups, markdowns and shrink, among others, and as such, could result in distortions of inventory

amounts.

Significant judgment is required for these estimates and assumptions, as well as to differentiate between

promotional and other markdowns that may be required to correctly reflect merchandise inventories at the lower

of cost or market. The Company provides reserves based on current selling prices when the inventory has not been

marked down to market. The failure to take permanent markdowns on a timely basis may result in an

overstatement of cost under the retail inventory method. The decision to take permanent markdowns includes

many factors, including the current environment, inventory levels, and the age of the item. Management believes

this method and its related assumptions, which have been consistently applied, to be reasonable.

Vendor Reimbursements

In the normal course of business, the Company receives allowances from its vendors for markdowns taken.

Vendor allowances are recognized as a reduction in cost of sales in the period in which the markdowns are taken.

Vendor allowances contributed 20 basis points to the 2010 gross margin rate. The Company also has

volume-related agreements with certain vendors, under which it receives rebates based on fixed percentages of

cost purchases. These volume-related rebates are recorded in cost of sales when the product is sold and were not

significant to the 2010 gross margin rate.

The Company receives support from some of its vendors in the form of reimbursements for cooperative

advertising and catalog costs for the launch and promotion of certain products. The reimbursements are agreed

upon with vendors for specific advertising campaigns and catalogs. Cooperative income, to the extent that it

reimburses specific, incremental and identifiable costs incurred to date, is recorded in SG&A in the same period as

the associated expenses are incurred. Cooperative reimbursements amounted to approximately 24 percent and

11 percent of total advertising and catalog costs, respectively, in 2010. Reimbursements received that are in

excess of specific, incremental and identifiable costs incurred to date are recognized as a reduction to the cost of

merchandise and are reflected in cost of sales as the merchandise is sold and were not significant in 2010.

26