Entergy 2008 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2008 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

|

|

9191

ENTERGY CORPORATION AND SUBSIDIARIES 2008

91

Notes to Consolidated Financial Statements continued

91

Gulf States Louisiana and Entergy Louisiana recover other

postretirement benefits costs on a pay as you go basis and recorded

the unrecognized prior service cost, gains and losses, and transition

obligation for its other postretirement benefit obligation as other

comprehensive income. SFAS 158 also requires that changes in the

funded status be recorded as other comprehensive income and/or

a regulatory asset in the period in which the changes occur.

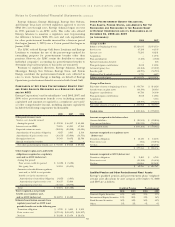

CO M P O N E N T S O F QU A L I F I E D NE T PE N S I O N CO S T A N D OT H E R

AM O U N T S RE C O G N I Z E D A S A RE G U L A T O R Y AS S E T A N D/O R

AC C U M U L A T E D OT H E R CO M P R E H E N S I V E IN C O M E (AOCI)

Entergy Corporation’s and its subsidiaries’ total 2008, 2007,

and 2006 qualified pension costs and amounts recognized as a

regulatory asset and/or other comprehensive income, including

amounts capitalized, included the following components:

(in thousands):

2008 2007 2006

Net periodic pension cost:

Service cost - benefits earned

during the period $ 90,392 $ 96,565 $ 92,706

Interest cost on projected

benefit obligation 206,586 185,170 167,257

Expected return on assets (230,558) (203,521) (177,930)

Amortization of prior

service cost 5,063 5,531 5,462

Recognized net loss 26,834 45,775 43,721

Curtailment loss – 2,336 –

Special termination benefit

loss – 4,018 –

Net periodic pension costs $ 98,317 $ 135,874 $ 131,216

Other changes in plan assets

and benefit obligations

recognized as a regulatory asset

and/or AOCI (before tax)

Arising this period:

Prior service cost $ – $ 11,339

Net (gain)/loss 965,069 (68,853)

Amounts reclassified from

regulatory asset and/or

accumulated AOCI

to net periodic pension cost in

the current year:

Amortization of prior

service credit (5,063) (5,531)

Amortization of net loss (26,834) (45,775)

Total $ 933,172 $(108,820)

Total recognized as net periodic

pension cost, regulatory asset,

and/or AOCI (before tax) $1,031,489 $ 27,054

Estimated amortization

amounts from regulatory

asset and/or AOCI to net

periodic cost in

the following year

Prior service cost $ 4,997 $ 5,064 $ 5,531

Net loss $ 22,401 $ 25,641 $ 44,316

QU A L I F I E D PE N S I O N OB L I G A T I O N S , PL A N AS S E T S , FU N D E D

ST A T U S , AM O U N T S NO T YE T RE C O G N I Z E D A N D RE C O G N I Z E D

IN T H E BA L A N C E SH E E T F O R EN T E R G Y CO R P O R A T I O N A N D I T S

SU B S I D I A R I E S A S O F DE C E M B E R 31, 2008 A N D 2007

(IN T H O U S A N D S):

2008 2007

Change in Projected Benefit Obligation (PBO)

Balance at beginning of year $ 3,247,724 $3,122,043

Service cost 90,392 96,565

Interest cost 206,586 185,170

Acquisitions and amendments – 52,142

Curtailments – 2,603

Special termination benefits – 4,018

Actuarial gain (89,124) (81,757)

Employee contributions 902 971

Benefits paid (151,165) (134,031)

Balance at end of year $ 3,305,315 $3,247,724

Change in Plan Assets

Fair value of assets at beginning of year $ 2,764,383 $2,508,354

Actual return on plan assets (823,636) 190,616

Employer contributions 287,768 176,742

Employee contributions 902 971

Acquisition – 21,731

Benefits paid (151,165) (134,031)

Fair value of assets at end of year $ 2,078,252 $2,764,383

Funded status $(1,227,063) $ (483,341)

Amount recognized in the balance sheet

Non-current liabilities $(1,227,063) $ (483,341)

Amount recognized as a regulatory asset

Prior service cost $ 20,548 $ 16,564

Net loss 1,150,298 436,789

$ 1,170,846 $ 453,353

Amount recognized as AOCI (before tax)

Prior service cost $ 4,941 $ 2,649

Net loss 276,635 69,581

$ 281,576 $ 72,230

OT H E R PO S T R E T I R E M E N T BE N E F I T S

Entergy also currently provides health care and life insurance

benefits for retired employees. Substantially all employees may

become eligible for these benefits if they reach retirement age

while still working for Entergy. Entergy uses a December 31

measurement date for its postretirement benefit plans.

Effective January 1, 1993, Entergy adopted SFAS 106, which

required a change from a cash method to an accrual method

of accounting for postretirement benefits other than pensions.

At January 1, 1993, the actuarially determined accumulated

postretirement benefit obligation (APBO) earned by retirees and

active employees was estimated to be approximately $241.4 million

for Entergy (other than the former Entergy Gulf States) and $128

million for the former Entergy Gulf States (now split into Entergy

Gulf States Louisiana and Entergy Texas.) Such obligations are

being amortized over a 20-year period that began in 1993. For the

most part, the Registrant Subsidiaries recover SFAS 106 costs from

customers and are required to contribute postretirement benefits

collected in rates to an external trust.