Entergy 2008 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2008 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

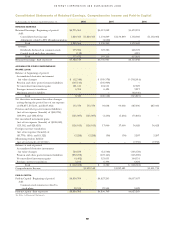

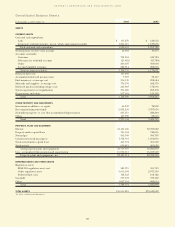

50

ENTERGY CORPORATION AND SUBSIDIARIES 2008

50

Management’s Financial Discussion and Analysis continued

Entergy’s Non-Utility Nuclear business’ purchase of the

FitzPatrick and Indian Point 3 plants from NYPA included value

sharing agreements with NYPA. In October 2007, NYPA and the

subsidiaries that own the FitzPatrick and Indian Point 3 plants

amended and restated the value sharing agreements to clarify

and amend certain provisions of the original terms. Under the

amended value sharing agreements, Entergy’s Non-Utility Nuclear

business agreed to make annual payments to NYPA based on the

generation output of the Indian Point 3 and FitzPatrick plants

from January 2007 through December 2014. Entergy’s Non-Utility

Nuclear business will pay NYPA $6.59 per MWh for power sold

from Indian Point 3, up to an annual cap of $48 million, and

$3.91 per MWh for power sold from FitzPatrick, up to an annual

cap of $24 million. The annual payment for each year is due by

January 15 of the following year. In August 2008, Non-Utility

Nuclear entered into a resolution of a dispute with NYPA over the

applicability of the value sharing agreements to its FitzPatrick and

Indian Point 3 nuclear power plants after the planned spin-off

of the Non-Utility Nuclear business. Under the resolution, Non-

Utility Nuclear agreed not to treat the separation as a “Cessation

Event” that would terminate its obligation to make the payments

under the value sharing agreements. As a result, after the spin-off

transaction, Non-Utility Nuclear will continue to be obligated to

make payments to NYPA under the amended and restated value

sharing agreements.

Non-Utility Nuclear will record its liability for payments to NYPA

as power is generated and sold by Indian Point 3 and FitzPatrick.

Non-Utility Nuclear recorded a $72 million liability for generation

in both 2008 and 2007. An amount equal to the liability will be

recorded to the plant asset account as contingent purchase price

consideration for the plants. This amount will be depreciated over

the expected remaining useful life of the plants.

Some of the agreements to sell the power produced by Entergy’s

Non-Utility Nuclear power plants contain provisions that require

an Entergy subsidiary to provide collateral to secure its obligations

under the agreements. The Entergy subsidiary is required to

provide collateral based upon the difference between the current

market and contracted power prices in the regions where Non-

Utility Nuclear sells power. The primary form of collateral to satisfy

these requirements is an Entergy Corporation guaranty. Cash and

letters of credit are also acceptable forms of collateral. At December

31, 2008, based on power prices at that time, Entergy had in place

as collateral $536 million of Entergy Corporation guarantees for

wholesale transactions, including $60 million of guarantees that

support letters of credit and $2 million of cash collateral. As of

December 31, 2008, the assurance requirement associated with

Non-Utility Nuclear is estimated to increase by an amount of up

to $216 million if gas prices increase $1 per MMBtu in both the

short- and long-term markets. In the event of a decrease in Entergy

Corporation’s credit rating to below investment grade, based on

power prices as of December 31, 2008, Entergy would have been

required under some of the agreements to replace approximately

$76 million of the Entergy Corporation guarantees with cash or

letters of credit.

For the planned energy output under contract through 2013 as

of December 31, 2008, 68% of the planned energy output is under

contract with counterparties with public investment grade credit

ratings; 31% is with counterparties with public non-investment

grade credit ratings, primarily a utility from which Non-Utility

Nuclear purchased one of its power plants and entered into a long-

term fixed-price purchased power agreement; and 1% is with load-

serving entities without public credit ratings.

In addition to selling the power produced by its plants, the

Non-Utility Nuclear business sells unforced capacity to load-

serving distribution companies in order for those companies

to meet requirements placed on them by the Independent

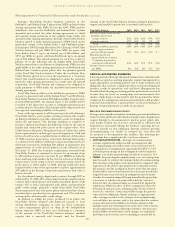

System Operator (ISO) in their area. Following is a summary

of the amount of the Non-Utility Nuclear business’ installed

capacity that is currently sold forward, and the blended

amount of the Non-Utility Nuclear business’ planned generation

output and installed capacity that is currently sold forward:

Non-Utility Nuclear 2009 2010 2011 2012 2013

Percent of capacity sold forward:

Bundled capacity and

energy contracts 26% 26% 26% 19% 16%

Capacity contracts 47% 34% 6% 9% 0%

Total 73% 0% 52% 28% 16%

Planned net MW in operation 4,998 4,998 4,998 4,998 4,998

Average capacity contract

price per kW per month $2.1 $3.4 $3.4 $3.2 $ –

Blended capacity and

energy (based on revenues)

% of planned generation

and capacity sold forward 86% 64% 43% 21% 14%

Average contract revenue

per MWh $63 $62 $59 $55 $50

CRITICAL ACCOUNTING ESTIMATES

The preparation of Entergy’s financial statements in conformity with

generally accepted accounting principles requires management to

apply appropriate accounting policies and to make estimates and

judgments that can have a significant effect on reported financial

position, results of operations, and cash flows. Management has

identified the following accounting policies and estimates as critical

because they are based on assumptions and measurements that

involve a high degree of uncertainty, and the potential for future

changes in the assumptions and measurements that could produce

estimates that would have a material effect on the presentation of

Entergy’s financial position or results of operations.

NU C L E A R DE C O M M I S S I O N I N G CO S T S

Entergy owns a significant number of nuclear generation facilities in

both its Utility and Non-Utility Nuclear business units. Regulations

require Entergy to decommission its nuclear power plants after

each facility is taken out of service, and money is collected and

deposited in trust funds during the facilities’ operating lives in

order to provide for this obligation. Entergy conducts periodic

decommissioning cost studies to estimate the costs that will

be incurred to decommission the facilities. The following key

assumptions have a significant effect on these estimates:

n COST ESCALATION FACTORS – Entergy’s decommissioning

revenue requirement studies include an assumption that

decommissioning costs will escalate over present cost levels

by annual factors ranging from approximately CPI-U to 5.5%.

A 50 basis point change in this assumption could change the

ultimate cost of decommissioning a facility by as much as 11%.

nTIMING – In projecting decommissioning costs, two assumptions

must be made to estimate the timing of plant decommissioning.

First, the date of the plant’s retirement must be estimated. The

expiration of the plant’s operating license is typically used for

this purpose, but the assumption may be made that the plant’s

license will be renewed and operate for some time beyond the

original license term. Second, an assumption must be made

whether decommissioning will begin immediately upon plant

retirement, or whether the plant will be held in “safestore”

status for later decommissioning, as permitted by applicable

regulations. While the effect of these assumptions cannot be

determined with precision, assuming either license renewal

or use of a “safestore” status can possibly change the present

value of these obligations. Future revisions to appropriately

reflect changes needed to the estimate of decommissioning

costs will affect net income, only to the extent that the estimate

of any reduction in the liability exceeds the amount of the

undepreciated asset retirement cost at the date of the revision,

for unregulated portions of Entergy’s business. Any increases

in the liability recorded due to such changes are capitalized

and depreciated over the asset’s remaining economic life in