Entergy 2008 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2008 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

6565

ENTERGY CORPORATION AND SUBSIDIARIES 2008

65

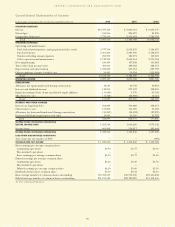

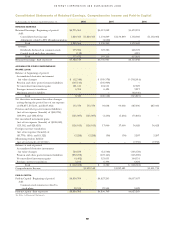

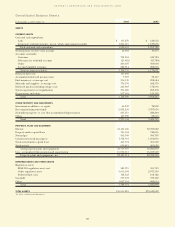

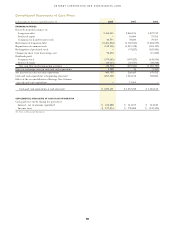

Notes to Consolidated Financial Statements continued

65

IN V E S T M E N T S

Entergy applies the provisions of SFAS 115, “Accounting for

Investments for Certain Debt and Equity Securities,” in accounting

for investments in decommissioning trust funds. As a result,

Entergy records the decommissioning trust funds on the balance

sheet at their fair value. Because of the ability of the Registrant

Subsidiaries to recover decommissioning costs in rates and in

accordance with the regulatory treatment for decommissioning

trust funds, the Registrant Subsidiaries have recorded an offsetting

amount of unrealized gains/(losses) on investment securities in

other regulatory liabilities/assets. For the nonregulated portion

of River Bend, Entergy Gulf States Louisiana has recorded an

offsetting amount of unrealized gains/(losses) in other deferred

credits. Decommissioning trust funds for Pilgrim, Indian Point 2,

Vermont Yankee, and Palisades do not receive regulatory treatment.

Accordingly, unrealized gains recorded on the assets in these trust

funds are recognized in the accumulated other comprehensive

income component of shareholders’ equity because these assets are

classified as available for sale. Unrealized losses (where cost exceeds

fair market value) on the assets in these trust funds are also recorded

in the accumulated other comprehensive income component

of shareholders’ equity unless the unrealized loss is other than

temporary and therefore recorded in earnings. The assessment

of whether an investment has suffered an other than temporary

impairment is based on a number of factors including, first, whether

Entergy has the ability and intent to hold the investment to recover

its value, the duration and severity of any losses, and, then, whether

it is expected that the investment will recover its value within a

reasonable period of time. See Note 17 to the financial statements

for details on the decommissioning trust funds and the other than

temporary impairments recorded in 2008.

EQ U I T Y ME T H O D IN VE S T E E S

Entergy owns investments that are accounted for under the equity

method of accounting because Entergy’s ownership level results

in significant influence, but not control, over the investee and its

operations. Entergy records its share of earnings or losses of the

investee based on the change during the period in the estimated

liquidation value of the investment, assuming that the investee’s

assets were to be liquidated at book value. In accordance with

this method, earnings are allocated to owners or members based

on what each partner would receive from its capital account if,

hypothetically, liquidation were to occur at the balance sheet

date and amounts distributed were based on recorded book

values. Entergy discontinues the recognition of losses on equity

investments when its share of losses equals or exceeds its carrying

amount for an investee plus any advances made or commitments to

provide additional financial support. See Note 14 to the financial

statements for additional information regarding Entergy’s equity

method investments.

DERIVATIVE FI N A N C I A L IN S T R U M E N T S A N D

CO M M O D I T Y DE RIVATIV ES

SFAS 133, “Accounting for Derivative Instruments and Hedging

Activities,” requires that all derivatives be recognized in the balance

sheet, either as assets or liabilities, at fair value, unless they meet the

normal purchase, normal sales criteria. The changes in the fair value

of recognized derivatives are recorded each period in current earnings

or other comprehensive income, depending on whether a derivative

is designated as part of a hedge transaction and the type of hedge

transaction.

Contracts for commodities that will be delivered in quantities expected

to be used or sold in the ordinary course of business, including certain

purchases and sales of power and fuel, are not classified as derivatives.

These contracts are exempted under the normal purchase, normal

sales criteria of SFAS 133. Revenues and expenses from these contracts

are reported on a gross basis in the appropriate revenue and expense

categories as the commodities are received or delivered.

For other contracts for commodities in which Entergy is hedging

the variability of cash flows related to a variable-rate asset, liability, or

forecasted transactions that qualify as cash flow hedges, the changes

in the fair value of such derivative instruments are reported in

other comprehensive income. To qualify for hedge accounting, the

relationship between the hedging instrument and the hedged item

must be documented to include the risk management objective and

strategy and, at inception and on an ongoing basis, the effectiveness of

the hedge in offsetting the changes in the cash flows of the item being

hedged. Gains or losses accumulated in other comprehensive income

are reclassified as earnings in the periods in which earnings are affected

by the variability of the cash flows of the hedged item. The ineffective

portions of all hedges are recognized in current-period earnings.

Entergy has determined that contracts to purchase uranium do not

meet the definition of a derivative under SFAS 133 because they do not

provide for net settlement and the uranium markets are not sufficiently

liquid to conclude that forward contracts are readily convertible to cash.

If the uranium markets do become sufficiently liquid in the future and

Entergy begins to account for uranium purchase contracts as derivative

instruments, the fair value of these contracts would be accounted for

consistent with Entergy’s other derivative instruments.

FA I R VA L U E S

The estimated fair values of Entergy’s financial instruments and

derivatives are determined using bid prices and market quotes.

Considerable judgment is required in developing the estimates of

fair value. Therefore, estimates are not necessarily indicative of the

amounts that Entergy could realize in a current market exchange.

Gains or losses realized on financial instruments held by regulated

businesses may be reflected in future rates and therefore do not accrue

to the benefit or detriment of stockholders. Entergy considers the

carrying amounts of most financial instruments classified as current

assets and liabilities to be a reasonable estimate of their fair value

because of the short maturity of these instruments. Effective January

1, 2008, Entergy and the Registrant Subsidiaries adopted Statement of

Financial Accounting Standards No. 157, “Fair Value Measurements”

(SFAS 157), which defines fair value, establishes a framework for

measuring fair value in GAAP, and expands disclosures about fair

value measurements. SFAS 157 generally does not require any new

fair value measurements. However, in some cases, the application

of SFAS 157 in the future may change Entergy’s and the Registrant

Subsidiaries’ practice for measuring and disclosing fair values under

other accounting pronouncements that require or permit fair value

measurements. See Note 16 to the financial statements for a discussion

of the implementation of SFAS 157.

IM P A I R M E N T O F LO N G -LI V E D AS S E T S

Entergy periodically reviews long-lived assets held in all of its

business segments whenever events or changes in circumstances

indicate that recoverability of these assets is uncertain. Generally,

the determination of recoverability is based on the undiscounted

net cash flows expected to result from such operations and assets.

Projected net cash flows depend on the future operating costs

associated with the assets, the efficiency and availability of the

assets and generating units, and the future market and price for

energy over the remaining life of the assets.

RI V E R BE N D AFUDC

The River Bend AFUDC gross-up is a regulatory asset that represents

the incremental difference imputed by the LPSC between the

AFUDC actually recorded by Entergy Gulf States Louisiana on a

net-of-tax basis during the construction of River Bend and what the

AFUDC would have been on a pre-tax basis. The imputed amount

was only calculated on that portion of River Bend that the LPSC

allowed in rate base and is being amortized through August 2025.